Tutorial Categories

Last Updated: February 24, 2026 at 13:30

Distress Valuation: The Art of the Waterfall in Debt Restructuring

Distress valuation is the analytical core of debt restructuring, showing how value is distributed among creditors, investors, and equity holders when a company faces financial stress. This tutorial explains the waterfall framework, demonstrates best case, base case, and distressed liquidation scenarios, and guides readers through expected recoveries under each. Using the example of Precio Components, we illustrate why equity holders may lose everything, subordinated creditors often face haircuts, and secured creditors typically recover most of their claims. By combining scenario analysis, probability weighting, and careful allocation, readers gain a practical toolkit to understand distressed capital structures and the strategic reasoning behind restructuring negotiations.

Introduction: Why Distress Valuation Matters

When a company is under financial stress, the core question guiding every negotiation is deceptively simple: What is the company worth?

Every decision—whether bondholders accept a debt-for-equity swap, senior lenders agree to extend maturities, or management implements operational changes—is shaped by this question. If stakeholders misjudge value, recoveries may be suboptimal, negotiations may fail, and the company may face unnecessary liquidation.

In healthy companies, value is often obvious. Publicly traded shares have market prices, comparable companies provide benchmarks, and historical performance guides expectations. In distressed situations, however, uncertainty reigns. Cash flows are volatile, assets may sell at discounted prices, and creditor claims compete against one another. Small differences in assumptions about future outcomes can dramatically change who gains and who loses.

Distress valuation provides a structured, analytical approach to this uncertainty. It allows stakeholders to quantify expected recoveries under different scenarios, turning speculation into informed negotiation. It is the bridge between the mechanics of restructuring—interest deferrals, principal haircuts, debt-for-equity swaps—and the financial logic that determines the allocation of value.

Two Kinds of Value: Going-Concern vs Liquidation

Before building the waterfall, it is essential to understand the distinction between going-concern and liquidation value, as this distinction drives restructuring decisions.

Going-concern value assumes the business continues operating. Customers keep buying, employees remain productive, suppliers continue shipping, and the company’s organizational capital—its relationships, processes, and know-how—retains value.

Liquidation value assumes the business stops. Assets are sold piecemeal, inventory may be cleared at discounts, equipment is auctioned off, and customer relationships dissolve. Liquidation values are almost always lower than going-concern values because the business’s integrated system no longer generates value.

For Precio Components, a mid-sized manufacturing company undergoing restructuring, the distinction is clear. If the company continues as a going concern, with operational improvements taking effect, its value might reach €120 million. If forced to liquidate, selling assets quickly at discounted prices, recoverable value might only be €70 million. The €50 million difference represents the surplus that restructuring aims to preserve.

This is why restructurings exist: when going-concern value exceeds liquidation value, there is an incentive to negotiate and maintain the business. If liquidation value is higher, preserving operations is unnecessary; the rational course is to sell the parts.

The Waterfall Concept: Visualizing the Flow of Value

At the heart of distress valuation lies the waterfall framework. It represents how cash flows and asset values move through a company’s capital structure during restructuring or liquidation.

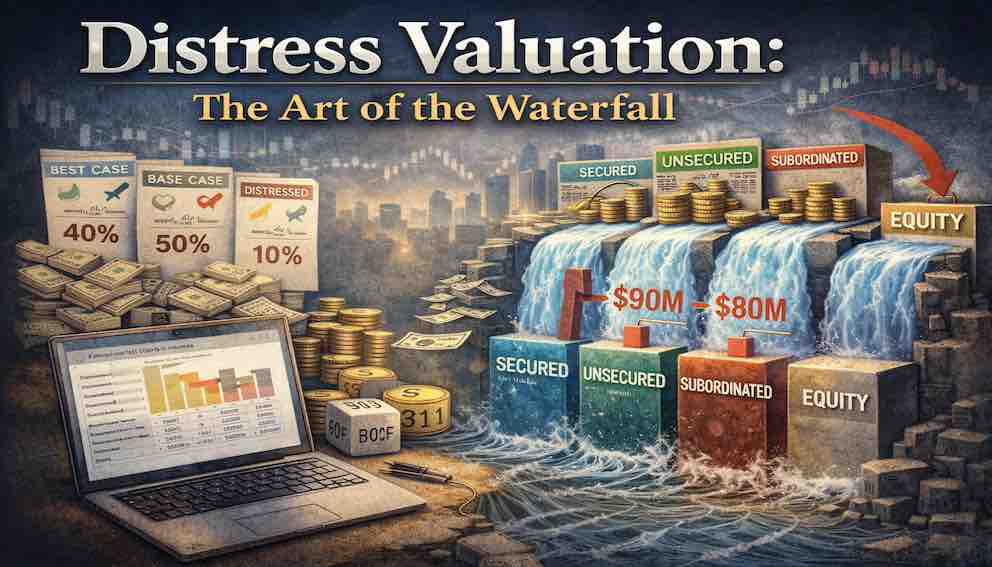

Imagine a literal waterfall. The total value of the company is like water cascading down. The first layer to receive the water is the highest-priority claim: secured debt. Once secured creditors are paid, any remaining value flows to senior unsecured creditors, then subordinated creditors, trade creditors, and finally equity holders.

The waterfall is not just a visualization; it reflects both legal and financial reality. In bankruptcy or negotiated restructurings, priority rules dictate recoveries. Those at the top almost always recover in full; those at the bottom face the greatest risk of loss. Understanding this flow clarifies why stakeholders behave the way they do in negotiations.

Precio Components’ Capital Structure

To make the waterfall tangible, consider Precio Components’ claims entering restructuring. The company has a mix of debt and equity, prioritized as follows:

- Senior secured debt: €70 million

- Unsecured bond debt: €30 million

- Subordinated debt: €10 million

- Trade payables: €5 million

- Equity (book value): €20 million

The estimated going-concern value under the operational plan ranges from €90 million to €120 million, depending on scenario assumptions. Liquidation value is roughly €70 million. This capital structure provides the framework for understanding who benefits under different outcomes.

Scenario Analysis: Best Case, Base Case, and Distressed Liquidation

Because future outcomes are uncertain, valuation under distress is scenario-driven. Analysts typically model at least three scenarios: best case, base case, and distressed liquidation, assigning probabilities to each.

- Best Case: Maria’s operational plan exceeds expectations. Cost reductions are realized, divisions stabilize, and the company generates strong cash flows. Going-concern value: €120 million. Probability: 20%.

- Base Case: Operational improvements succeed but market conditions remain competitive. Cash flows are adequate but not exceptional. Going-concern value: €95 million. Probability: 60%.

- Distressed Liquidation: Operational improvements fail, key customers leave, and assets must be sold quickly. Liquidation value: €70 million. Probability: 20%.

Assigning probabilities is itself a negotiation. Creditors may dispute which scenario is most likely, influencing the allocation of equity and the design of debt restructuring plans.

Walking the Waterfall

Best Case (€120 million)

Senior secured debt: €70 million is paid in full. Remaining value: €50 million.

Unsecured bond debt: €30 million is paid in full. Remaining value: €20 million.

Subordinated debt: €10 million is paid in full. Remaining value: €10 million.

Trade payables: €5 million is paid in full. Remaining value: €5 million.

Equity: €5 million flows to equity holders. Book value was €20 million, so equity recovers 25% of its claim.

In this best case, all stakeholders receive some recovery, and equity holders, typically wiped out in distress, gain partial value.

Base Case (€95 million)

Senior secured debt: €70 million is fully paid. Remaining value: €25 million.

Unsecured bond debt: €25 million is paid, leaving a €5 million haircut. Remaining value: €0.

Subordinated debt: Nothing remains. Losses are total.

Trade payables: Nothing remains.

Equity: Nothing remains. Wiped out entirely.

Here, senior lenders are fully protected, bondholders take a modest haircut, and lower-priority claimants, including equity, receive nothing.

Distressed Liquidation (€70 million)

Senior secured debt: €70 million is fully recovered. Remaining value: €0.

Unsecured bond debt: Nothing remains.

Subordinated debt: Nothing remains.

Trade payables: Nothing remains.

Equity: Nothing remains.

In this worst-case scenario, only secured creditors recover, highlighting the risk for subordinated creditors and equity holders.

Expected Recovery and Negotiation Implications

Expected recovery is calculated by weighting scenario outcomes by probabilities. For example:

- Senior secured debt: Paid in full across all scenarios, expected recovery 100%.

- Unsecured bonds: Weighted recovery is 70% of the claim.

- Subordinated debt: Weighted recovery 20%.

- Trade payables: Weighted recovery 20%.

- Equity: Weighted recovery 5%.

These calculations explain negotiation dynamics. Senior lenders’ security gives them power; bondholders face risk and may accept equity to gain upside; subordinated lenders and equity holders are incentivized to accept minimal recoveries or risk complete loss. The waterfall frames these incentives clearly.

Valuation as a Negotiation Battlefield

Every assumption—probabilities, scenario valuations, and liquidation estimates—is contested. Stakeholders hire experts to support their positions:

- Bondholders may argue for higher probabilities of best-case scenarios to justify larger equity stakes.

- Senior lenders may emphasize downside risk to retain control and limit concessions.

- Equity holders may highlight residual value in any scenario to maintain negotiating leverage.

In other words, the numbers are not just calculations—they are tools for argument, influence, and strategy.

Beyond Simple Waterfalls: Strategic Value and Option-Like Features

Strategic Premiums

Some divisions or assets may have unique appeal to strategic buyers. For example, a defense contractor might pay €150 million for Precio Components’ aerospace division, far above standalone going-concern value. Such premiums alter expected recoveries, potentially increasing payouts for bondholders and even equity.

Equity as a Call Option

Equity receives value only if enterprise value exceeds total senior claims, functioning like a deep out-of-the-money call option. The time value lies in the potential upside from operational success, explaining why equity holders may resist restructuring even with low expected recovery.

Subordinated Debt as Hybrid

Subordinated debt blends fixed-income and equity-like risk. It may be partially impaired but can also convert into equity, formalizing exposure that already resembles equity economics. This explains why subordinated lenders sometimes accept debt-for-equity swaps.

Practical Toolkit: Steps for Distress Valuation

- Map the capital structure: Include secured debt, unsecured debt, subordinated debt, trade payables, and equity. Note guarantees, collateral, or intercreditor agreements.

- Estimate going-concern value: Use DCF or market multiples with explicit assumptions on revenue, margins, and capital expenditures.

- Estimate liquidation value: Value assets as if sold quickly, accounting for discounts and transaction costs.

- Develop scenarios: At least three (upside, base, downside) with probability assignments.

- Run the waterfall: Allocate value by priority for each scenario.

- Calculate expected recoveries: Weight scenario outcomes by probabilities.

- Analyze negotiation dynamics: Identify who gains, who risks loss, and areas of conflict.

- Test assumptions: Adjust key variables to see sensitivity and reveal which assumptions drive disputes.

Conclusion: Seeing the Financial DNA of Distress

Distress valuation turns abstract restructuring mechanics into a concrete, quantifiable framework. Through Precio Components, we followed cash flows through the waterfall under multiple scenarios, understanding why senior lenders recover in almost all cases, unsecured creditors may face haircuts, subordinated debt and trade creditors are often wiped out, and equity typically receives little or nothing.

Scenario analysis and probability weighting transform uncertainty into expected values, showing how valuation drives negotiation and strategy. Strategic premiums, option-like features, and control considerations further complicate the picture but do not change the fundamental principle: value first, allocate according to priority.

Most importantly, the waterfall is a lens for understanding the financial DNA of distress—how incentives, risks, and potential rewards shape behavior. With this framework, analysts, managers, and investors can see why some restructurings succeed, others fail, and how numbers, strategy, and negotiation are deeply intertwined.

In the final tutorial of this series, we will explore the human side of distress: how leaders navigate crisis, communicate with stakeholders, and make decisions when the stakes are highest and the path is uncertain.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.