Tutorial Categories

Last Updated: February 13, 2026 at 19:30

Corporate Governance: Who Really Controls the Firm? Understanding Boards, Management, and Shareholder Power

Corporate governance explains who really guides a company, how important decisions are taken, and how leaders are held responsible for their actions. In this tutorial, we look closely at the relationship between boards of directors, managers, and shareholders, and we explain how differences in power, strong founder influence, and company culture shape what actually happens inside firms. Through real examples such as Enron, Volkswagen, WeWork, and Meta, we show that simply having independent board members does not always ensure proper supervision or accountability. You will learn clear principles that support effective governance and practical ways to align authority, incentives, and behavior so that they work in the firm’s long-term interest. Corporate governance is not only a legal structure written in documents; it is the underlying system that ultimately determines whether a company performs well or moves toward failure.

Introduction: From Incentives to Organizational Control

In previous tutorials, we examined how incentives shape behavior. We studied the mortgage loan officer whose commission encouraged risky approvals, the trader whose bonus structure rewarded excessive risk, and executives whose stock options favored short-term stock price spikes over long-term growth.

These stories illuminate individual behavior, but they also point to a deeper question: who designs and oversees the systems that create these incentives?

The loan officer does not set her commission. The trader does not design his bonus formula. The executive does not draft her own employment contract. These systems are created, approved, and monitored by boards, compensation committees, and shareholders.

If incentives are the software guiding behavior, governance is the operating system controlling what software gets installed, who can change it, and how errors are detected. Even the most elegantly designed incentives fail when governance is weak. Governance answers the question: who watches the watchers?

What Corporate Governance Really Is

Corporate governance is the system of rules, practices, and relationships through which a corporation is directed and controlled. It encompasses:

- Legal structures: Charters, bylaws, and shareholder agreements that define formal authority.

- Relational dynamics: Informal influence, deference to founders, and collective action challenges among shareholders.

- Culture: Expectations for honesty, transparency, and active engagement.

- Market constraints: Takeovers, activist investors, and debt covenants that discipline decision-making.

Governance is not a document. It is a lived system of power, behavior, and accountability.

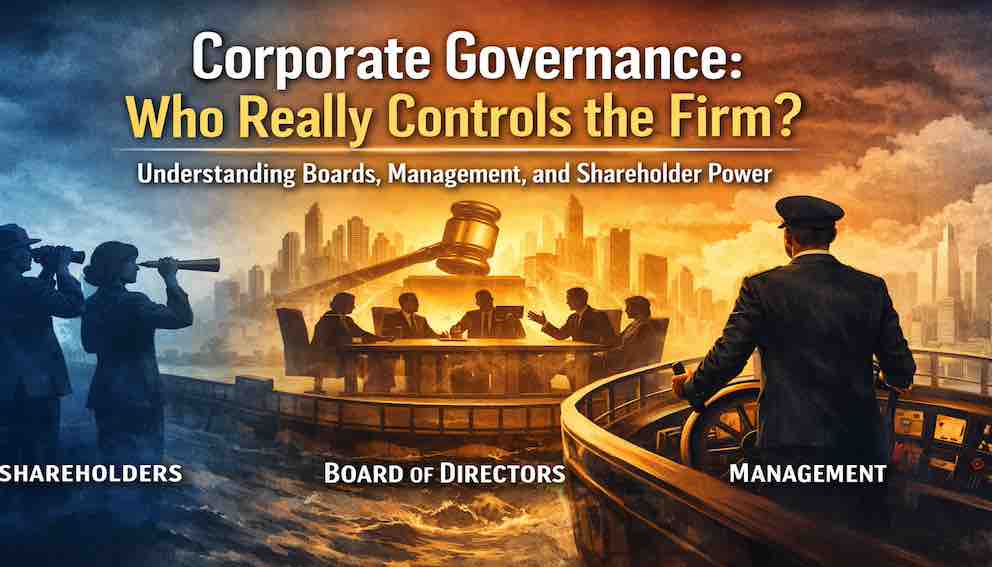

The Ship Analogy: Understanding Power Asymmetry

Imagine a ship on a long voyage.

- Shareholders are the owners: They pooled resources to build and equip the vessel. They want it to reach port safely but do not steer the ship.

- The board of directors is the representative assembly: They hire the captain, approve destinations, and monitor the voyage. They review logs, question the crew, and ensure resources are used wisely.

- Management is the captain and crew: They navigate, adjust the sails, and manage daily operations. They possess specialized knowledge about the ship and the sea.

Tensions are inevitable:

- The captain knows more than the board.

- The board knows more than the dispersed shareholders.

- Shareholders have the most at stake but the least information.

This is the fundamental challenge of governance: ensuring those with the least information—but the most at risk—can effectively monitor those with the most information—but the least personal exposure to loss.

The Players and Their Powers

Shareholders: Owners Who Often Cannot Govern

Shareholders are the residual claimants. They benefit when the firm prospers and lose when it fails. In theory, this should incentivize monitoring.

- Individual shareholders often hold negligible stakes. Rationally, they sell rather than engage.

- Institutional investors have resources but face agency and collective action problems. The effort of monitoring may benefit many but is costly to the individual institution.

- Activist investors concentrate stakes, bear monitoring costs, and demand changes. They are effective but sometimes controversial, balancing short-term gains against long-term value.

Mini Takeaway: Dispersed ownership creates a natural vacuum of power that management can exploit.

Boards of Directors: The Watchdogs Who Often Sleep

Boards are designed to solve the collective action problem, acting as shareholders’ representatives. They hire and fire the CEO, approve strategy, and monitor performance.

Challenges:

- Selection: CEOs often influence board composition. Dissident candidates rarely succeed.

- Information asymmetry: Boards rely on management-prepared reports, limiting independent insight.

- Social dynamics: Directors develop relationships with CEOs, making confrontation difficult.

- Incentives: Compensation is rarely tied meaningfully to performance, and challenging management can risk renomination.

Even highly formalized boards can fail if they lack intellectual independence, vigilance, and courage.

Mini Takeaway: Independence on paper is not independence in action. Culture and human behavior shape outcomes.

Management: Agents Who Become Principals

CEOs are single, full-time actors with deep knowledge of the firm, while boards are part-time, dispersed, and information-limited. This creates a natural asymmetry of power.

- The CEO controls agenda-setting, information flow, and board nominations.

- Board authority exists but is rarely exercised until crises occur.

- Most CEOs retire honored, not fired, illustrating that governance often works imperfectly.

Mini Takeaway: Power is concentrated in management due to attention, expertise, and social dynamics, not necessarily malfeasance.

The Founder Problem: Ownership vs Control

Founders often retain control far exceeding their economic stake:

- Mark Zuckerberg controls Meta via super-voting shares, enabling long-term vision but insulating from accountability.

- Adam Neumann at WeWork retained control and extracted personal benefits, harming shareholders.

The same governance mechanism can yield radically different outcomes depending on the founder’s integrity, incentives, and skill.

Mini Takeaway: Governance effectiveness depends on context and individuals, not just structure.

The Independence Mirage

Board independence is widely regarded as a solution. But formal independence is insufficient. Directors may:

- Lack industry knowledge or confidence

- Be overcommitted to multiple boards

- Avoid confrontation to preserve reputation

Intellectual independence—the willingness to ask hard questions, challenge assumptions, and say no—is critical.

Lessons from Governance Failures

Enron: Cultural Capture

Enron appeared to have strong governance on paper. The board was formally independent, committees were led by financially knowledgeable directors, and the structure matched what many governance frameworks recommend. However, despite these formal safeguards, directors did not effectively challenge the company’s complex financial engineering or the dominance of senior executives.

The failure was not caused by missing rules but by belief, trust, and culture. Directors trusted management’s confidence and embraced the company’s success narrative. Over time, this created cultural capture, where skepticism weakened and questioning leadership felt unnecessary or even disloyal. The board became aligned with management rather than actively overseeing it.

The key takeaway is that structural compliance cannot replace behavioral vigilance. Independent committees and formal procedures only work if directors are willing to ask difficult questions, verify information, and remain skeptical even during periods of apparent success. Governance depends not just on systems, but on the courage and judgment of the people operating within them.

Volkswagen: Hidden Information and Culture

- Governance appeared robust by German standards.

- Systematic emissions cheating arose from culture and suppressed information flows, not board neglect.

- Mid-level managers prioritized company priorities over ethics, hiding risks from oversight.

Takeaway: Boards can monitor only what they are allowed to see; culture shapes what reaches the top.

Activist Investors: Corrective Force

Activist investors step in when they believe a company is underperforming or poorly governed. Because most individual shareholders own small stakes and lack incentives to organize (the collective action problem), activists solve this by buying a significant ownership stake and pushing publicly for strategic, financial, or leadership changes. Their concentrated position gives them both influence and motivation to demand accountability.

The results of activism are mixed. Some activists push for operational improvements, better capital allocation, or stronger governance that increases long-term value. Others may focus on short-term measures—such as share buybacks or asset sales—that quickly boost stock prices but may not strengthen the company’s long-term position.

Importantly, activist investors tend to emerge where ordinary governance mechanisms—like board oversight or dispersed shareholder monitoring—have not been effective. In that sense, they often act as a market-based corrective force when internal controls and accountability systems fall short.

Principles for Effective Governance

Governance is about behavior, not just structure.

A company can have all the correct committees, policies, and reporting lines on paper, yet still fail if the people within the system do not exercise independent thinking and responsible judgment. Effective governance depends on how individuals behave in real situations, especially when facing pressure, uncertainty, or conflicting incentives. Structure creates the framework, but behavior determines whether that framework actually works.

Independent committees are ineffective without active judgment.

Simply labeling a committee as “independent” does not guarantee that it will challenge management or ask difficult questions. True independence requires members who are willing to analyze information critically, voice disagreement when necessary, and resist social or professional pressure to conform. Without active engagement and thoughtful skepticism, independence becomes a formality rather than a safeguard.

Actively manage information asymmetry.

Managers typically possess far more detailed knowledge about daily operations than board members, which creates an imbalance known as information asymmetry. If this imbalance is not carefully managed, boards may rely too heavily on summaries or selectively presented data. Effective governance requires systems that ensure directors receive timely, complete, and unfiltered information so that their oversight is grounded in reality rather than narrative.

Boards should meet mid-level managers, conduct site visits, and demand alternative analyses.

Direct interaction with employees below the executive level allows board members to hear perspectives that might not surface in formal presentations. Site visits help directors observe operational realities firsthand rather than relying only on reports. Requesting alternative analyses or “what-if” scenarios also ensures that decisions are tested against different assumptions, reducing the risk of blind spots.

Balance power, don’t eliminate it.

Strong leadership can be valuable, especially in times of rapid change or crisis, but concentrated power without oversight can create significant risks. Governance should aim to create balance, where authority is paired with accountability rather than weakened entirely. The goal is not to remove power from leaders, but to ensure that it operates within clear boundaries and is subject to review.

CEO power is necessary but must be counterbalanced by board authority, lead directors, and long-term incentives.

Chief executives often need sufficient authority to make strategic decisions quickly and to guide the organization with clarity. However, this authority should be balanced by an empowered board, strong lead independent directors, and compensation structures that reward sustainable performance rather than short-term gains. Such counterweights reduce the likelihood that personal ambition or overconfidence will harm the firm.

Culture is a governance responsibility.

Corporate culture shapes how employees behave when rules are unclear or supervision is limited, making it a central governance concern rather than a peripheral issue. Boards must recognize that toxic or overly aggressive cultures can undermine formal controls. Monitoring culture is therefore part of protecting long-term firm value.

Boards monitor employee surveys, turnover, whistleblower reports, and internal communications.

These indicators provide early signals about underlying problems that may not yet appear in financial statements. High turnover, declining morale, or frequent whistleblower complaints can reveal ethical, operational, or leadership issues. By reviewing these signals regularly, boards can detect risks before they escalate into crises.

Shareholders must be engaged.

Shareholders are not merely providers of capital; they are owners with legitimate interests in the firm’s direction and integrity. Active dialogue between boards and shareholders encourages transparency and strengthens accountability. When shareholders are informed and involved, governance becomes a shared responsibility rather than a procedural obligation.

Beyond compliance, boards should treat shareholders as partners in accountability.

Regulatory compliance sets a minimum standard, but effective governance requires going beyond basic legal requirements. By treating shareholders as long-term partners, boards foster trust and open communication about strategy, risk, and performance. This partnership perspective reinforces the idea that governance is ultimately about preserving and growing value responsibly over time.

Global Perspectives

US:

The United States commonly follows a one-share-one-vote model, meaning voting power generally corresponds to economic ownership. However, many companies—especially founder-led technology firms—use dual-class share structures that give certain shareholders (often founders) superior voting rights. This allows founders to retain control even with a smaller economic stake, creating a deliberate imbalance between ownership and control.

UK & EU:

In the United Kingdom and much of the European Union, governance frameworks emphasize strong independent directors and formal board oversight. Stewardship codes encourage institutional investors to actively monitor and engage with companies rather than remain passive owners. There is also greater recognition of stakeholder interests, such as employees and broader societal impact, within governance discussions.

Germany & Japan:

Germany and Japan commonly use two-tier board structures that separate supervisory and management functions. In Germany, for example, supervisory boards include both shareholder and employee representatives, formally integrating labor into corporate oversight. This structure is designed to balance long-term stability with accountability to investors.

Mini Takeaway:

While governance systems differ in structure across countries, the core challenges remain the same. Information asymmetry between management and boards, the influence of corporate culture, and the limited time and attention of directors are universal issues. No matter the formal design, governance ultimately depends on how people behave within the system.

Linking Governance to Firm Performance

Strong governance consistently correlates with:

- Higher long-term profitability and shareholder returns

- Lower risk of crises or fraud

- Better strategic decision-making

- Improved capital allocation and market confidence

Good governance channels individual behavior and incentives toward long-term value creation, while poor governance amplifies risk and misalignment.

Forward-Looking Trends

Digital oversight:

Boards are increasingly using digital dashboards, data analytics, and AI-driven reporting tools to monitor performance and risk in real time. These tools help reduce information gaps between management and directors by providing more direct, timely access to operational and financial data. While technology improves transparency and speed, it still requires directors to interpret the data critically and ask the right questions.

ESG governance:

Environmental, social, and governance (ESG) considerations are becoming central to board oversight rather than peripheral concerns. Boards now track metrics such as carbon emissions, workforce diversity, supply chain ethics, and regulatory compliance alongside financial performance. The goal is to manage long-term risks and reputational exposure while aligning corporate strategy with evolving societal expectations.

Stakeholder-focused governance:

Many firms are broadening their focus beyond shareholders to include employees, customers, suppliers, and communities. This approach recognizes that sustainable value creation often depends on maintaining trust and strong relationships across multiple stakeholder groups. Balancing these interests can be complex, especially when short-term shareholder returns conflict with longer-term social or strategic goals.

Overall takeaway:

Governance structures are adapting to technological change, global scrutiny, and shifting societal expectations. However, despite new tools and broader objectives, the core lessons remain unchanged: effective governance still depends on incentives, accountability, and the judgment and behavior of the people in positions of oversight.

Conclusion: Governance as an Unfinished Work

Corporate governance is the architecture within which a firm operates. Formal structures—boards, committees, shareholder rights—are necessary but insufficient. Behavior, culture, attention, and information flow determine whether governance works in practice.

Failures are predictable outcomes of structural incentives and human psychology, not anomalies. Effective governance requires ongoing effort: recruiting intellectually independent directors, investing in information systems, cultivating a healthy culture, and engaging shareholders continuously.

There is no final destination for governance. Firms that thrive recognize it as an eternal, unfinished work, and commit daily to the tension between delegation and accountability.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.