Tutorial Categories

Last Updated: March 4, 2026 at 10:30

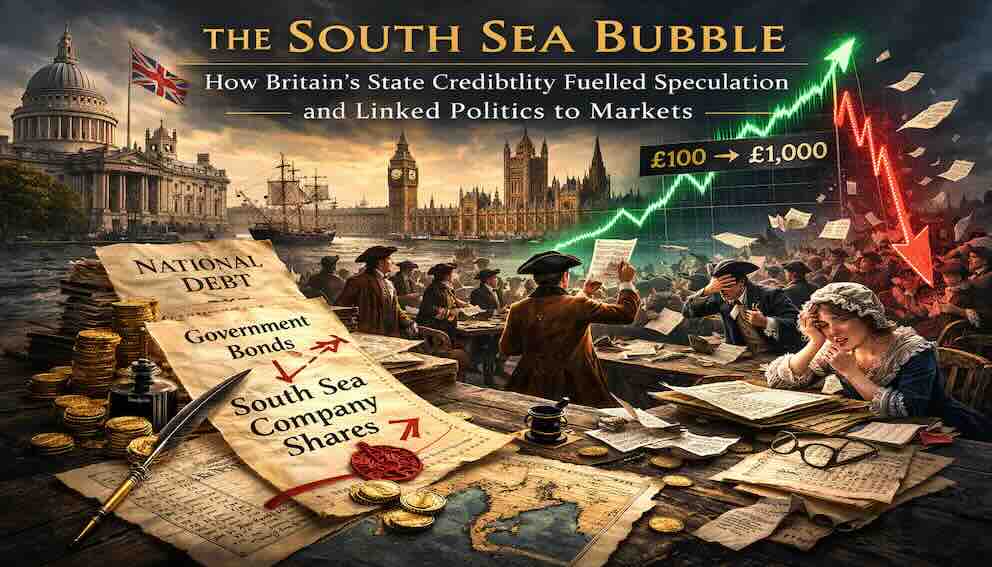

The South Sea Bubble of 1720: How Britain's National Debt, State Credibility, and Political Power Fueled a Historic Financial Crash

In early eighteenth-century Britain, the boundary between government and finance was thin, and that thin boundary helped create one of the most famous bubbles in history: the South Sea Bubble. The episode was not just a story about greed or naïve investors, but about how state credibility can amplify speculation when public debt, political promises, and private shares become tightly intertwined. By looking closely at how the South Sea Company was structured, how it converted government debt into equity, and how Parliament itself became entangled in the scheme, we can see how trust in the state can both stabilize and destabilize markets. The South Sea Bubble connects finance and politics in a way that still echoes today whenever governments backstop markets or fuse public guarantees with private risk.

A Coffeehouse, a Ledger, and a Promise

London in 1720. Exchange Alley, near the Royal Exchange, is thick with traders. At Jonathan's Coffeehouse, men in wigs lean over handwritten price sheets. Clerks run between establishments, shouting the latest quotes. A gentleman who bought South Sea Company shares at £100 sees them quoted at £300. Then £500. Then £1,000. He feels a mixture of pride and disbelief. He owns no ships, no cargoes, no warehouses. He owns a promise, and that promise seems blessed by the British state itself.

Across the alley, a widow who converted her safe government annuity into South Sea shares watches the same prices. She had been assured that Parliament stood behind the scheme. Now her paper wealth multiplies. She does not sell. Why sell when everyone says prices will rise further? The widow’s decision was not irrational in the way later commentators sometimes suggest. She was responding to signals that seemed solid.

What unfolded in 1720 was less a sudden outbreak of madness than an experiment in statecraft carried out through markets. Britain was discovering that political credibility could be converted into financial leverage. The same machinery that allowed the government to borrow cheaply could also amplify speculation.

The government needed to manage enormous war debts. Investors needed safe, credible assets. The South Sea Company appeared to solve both problems at once. That alignment of interests, backed by Parliament, created a powerful wave of confidence. Confidence, in turn, became fuel for speculation.

The difficulty lay in what people were being asked to value. A farm can be walked. A bale of wool can be inspected. A ship can be seen in the harbor But a claim on future tax revenues depends on political discipline that must be maintained year after year. Profits from trade with distant colonies depend on treaties, ships, and markets that most shareholders would never see. Investors could not examine these foundations directly. They had to rely on parliamentary approval, the reputation of directors, and, increasingly, the behavior of other buyers.

In such an environment, trust becomes a collective act. Each person looks sideways as much as forward. If others appear confident, confidence feels justified. If others hesitate, doubt spreads quickly. The South Sea Bubble grew inside this fragile coordination.

The South Sea Bubble shows how trust can be magnified by state backing, and how that magnified trust can detach from reality.

Britain's Financial Revolution: Debt, War, and Credibility

In the late seventeenth and early eighteenth centuries, Britain was transforming. After the Glorious Revolution of 1688, Parliament gained stronger control over taxation and borrowing. The creation of the Bank of England in 1694 allowed the government to borrow more systematically. Investors could lend to the state and receive interest funded by taxes approved by Parliament.

This arrangement was revolutionary. In many European countries, kings could repudiate debts or alter terms at will. In Britain, the growing authority of Parliament made default less likely. The state's promise began to carry weight. Government debt became a tradable, semi-liquid asset.

By 1719, Britain's national debt stood at roughly £50 million—an enormous sum for an economy that was still largely agricultural. Interest payments consumed a significant portion of state revenues. The burden of war financing from the War of the Spanish Succession pressed heavily on the Treasury. Parliament was desperate for solutions.

A London merchant with spare capital could lend to the government and receive regular interest. He believed Parliament would honor the debt because its own members, and their allies, were investors too. The people who approved taxes were often the same people collecting interest. Default would have meant harming themselves.

This illustrates a principle that extends far beyond eighteenth-century Britain: state credibility is a form of capital. When people believe a government will honor its obligations, the government can mobilize private savings at scale. That mobilization can be stabilizing. It can also create platforms for complex financial engineering.

The modern echo is clear. When investors buy U.S. Treasury bonds or German Bunds, they rely on state credibility. That credibility lowers borrowing costs. Yet when that same credibility supports complex financial products—mortgage-backed securities with implicit government backing—the line between safe public debt and speculative private assets can blur. The South Sea Bubble shows an early version of that blur.

The South Sea Company: Converting Public Debt into Private Shares

The South Sea Company was founded in 1711. Its formal purpose was to trade with Spanish South America, the "South Seas." The trade rights were limited and uncertain, since Britain and Spain were rivals. The more important function of the company lay elsewhere.

Britain had accumulated massive war debts. The government needed a way to manage and refinance this burden. The South Sea Company offered a solution. It would assume a large portion of the national debt. In exchange, it would receive interest payments from the government. Creditors who held government debt could swap their bonds for shares in the company.

Make this concrete. Suppose you hold £1,000 of government debt paying 6 percent interest. The South Sea Company offers to exchange your bond for £1,000 worth of its shares. The government will pay interest to the company, and the company will use that income to support dividends to shareholders. You now own equity in a trading company that also receives steady payments from the state.

This structure combined two elements. First, it tied the company's revenue to government payments, which were seen as reliable. Second, it dangled the prospect of vast profits from trade in the Americas. The safe income from public debt blended with the exciting story of overseas riches.

The principle here is subtle but powerful: when a company's revenue is anchored in state payments, investors may treat its shares as semi-sovereign instruments. The presence of government cash flows lowers perceived risk. That lower perceived risk allows prices to rise more easily, because buyers feel protected.

In 1720, the South Sea Company proposed an even more ambitious scheme. It would assume almost all remaining government debt in exchange for new shares. But it faced competition. The Bank of England also submitted a bid to take over the debt. The South Sea Company outbid it, offering more favorable terms to the government and to debt holders. This was not merely speculation; it was a competitive battle for control of the state's financial machinery. Political factions backed different institutions, and the outcome would shape Britain's financial architecture for years.

Parliament approved the South Sea scheme. The company would profit from managing the debt, and investors would benefit from rising share prices.

This was financial alchemy. Government debt was being transformed into equity. Equity was being marketed not only as a claim on trade profits, but as a stake in a state-backed financial machine.

The modern echo appears whenever private financial institutions are tightly interwoven with government guarantees. Consider government-sponsored enterprises like Fannie Mae and Freddie Mac before the 2008 crisis. Investors believed the U.S. government would not allow them to fail. That belief reduced perceived risk and supported high valuations. The South Sea Company operated in the same zone: private shares infused with public credibility.

Parliament, Privilege, and the Social Spread of Speculation

Picture a Member of Parliament in early 1720. He hears that the South Sea Company's directors are offering favorable terms for debt conversions. He knows that colleagues are subscribing to shares. He may even receive shares at preferential prices—a quiet reward for political support. Some ministers are implicated in these distributions.

As the share price rises from £100 to £300 and then toward £1,000, the atmosphere becomes feverish. Aristocrats, merchants, widows, and craftsmen all want in. Pamphlets circulate promising wealth. Other speculative ventures spring up, some absurd, including famously vague proposals for companies "for carrying on an undertaking of great advantage, but nobody to know what it is."

The rise in price creates its own justification. A man who hesitated at £200 sees the price at £400 and concludes he was foolish to wait. He buys at £500. His purchase pushes the price higher. The cycle feeds itself.

The crucial factor is political endorsement. Parliament approved the debt conversion. Leading politicians are associated with the company. The scheme carries an aura of official blessing, and that blessing was partly purchased through share allocations.

This introduces the concept of moral hazard. Moral hazard arises when someone takes more risk because they believe they are protected from consequences. In the South Sea case, investors believed that because the company was intertwined with the state, catastrophic failure was unlikely. That belief made them more willing to speculate.

The coordination problem deepens here. Each individual investor reasons that as long as others continue to buy, the price will rise. The rational strategy seems to be to join the crowd, even if private doubts exist. Economists later called this "greater fool" dynamics—each buyer expects to sell to someone else at a higher price.

The modern echo is visible in episodes where political endorsement amplifies speculative waves. When governments signal strong support for certain sectors—housing in the early 2000s, green energy more recently—investors may interpret that support as a safety net. That perception can drive capital flows beyond fundamental value. The South Sea Bubble reminds us that political proximity can intensify herd behavior.

The Liquidity Illusion

One element of the South Sea scheme is easy to overlook today, but it mattered enormously to investors. Government debt before conversion was relatively illiquid. It paid steady interest but could not be easily sold. South Sea shares, by contrast, traded actively in Exchange Alley. They could be converted into cash at a moment's notice.

This liquidity was seductive. An asset that can be sold quickly feels safer, even if its price fluctuates wildly. Investors traded predictable interest income for liquid, rising equity. They gained the ability to exit, but they also exposed themselves to price swings driven by sentiment.

The liquidity illusion is this: liquid assets feel safe because you believe you can always sell. But when everyone tries to sell at once, liquidity vanishes. The very feature that attracted investors—easy trading—becomes the channel through which panic spreads. In 1720, that illusion shattered when sellers found no buyers at any price near the recent highs.

Modern investors experience this constantly. Exchange-traded funds, popular stocks, and even real estate investment trusts offer daily liquidity. That liquidity feels like protection. But in a crash, liquidity can evaporate as quickly as confidence. The South Sea Bubble reminds us that tradability is not the same as safety.

Collapse: When Confidence Turns

By late summer 1720, cracks appeared. Insiders quietly sold shares. Confidence wavered. The price, which had reached near £1,000, began to fall. As it fell, leveraged investors faced losses. Many had borrowed to buy shares, expecting continued appreciation.

Imagine a merchant who bought shares at £800 using borrowed funds. When the price falls to £600, his collateral is insufficient. He must sell to cover debts. His sale pushes the price lower still. Others, seeing the decline, rush to exit.

Imagine also a widow who had converted her safe government annuity into shares at £900. She had been told the scheme was backed by Parliament. Now her savings are evaporating. She cannot sell because the price is collapsing faster than she can find a buyer. The pride she felt months ago has turned to despair.

Confidence, once abundant, evaporates quickly. The same state association that had reassured investors now becomes a source of anger. Accusations of corruption spread. Parliamentary inquiries follow. Some directors are disgraced. Their estates are confiscated to compensate victims.

Public anger focuses on the politicians who took shares. The entanglement of power and profit, once hidden, is now exposed. Trust in the system fractures.

The deeper principle is that trust has a tipping point. While rising prices create a feedback loop of optimism, falling prices create a feedback loop of fear. When an asset is valued partly on confidence in political arrangements, any hint of political scandal or mismanagement accelerates decline.

We can think of this as a "trust thermocline." In the ocean, temperature changes gradually until, at a certain depth, it shifts sharply. In markets, confidence may seem stable until it reaches a threshold, and then sentiment changes abruptly. In 1720, that shift was dramatic.

Modern markets experience similar moments. During the 2008 financial crisis, institutions once considered secure faced rapid loss of confidence. Even firms with strong political connections saw their stock prices collapse when trust eroded. The South Sea Bubble shows that when finance and politics are fused, crises become both financial and political events.

The Fusion of Finance and Politics: A Structural Lesson

The South Sea Bubble is often taught as a morality tale about greed. That interpretation misses the structural insight. Britain was building a powerful fiscal-military state. It needed sophisticated financial tools. The South Sea Company was an experiment in aligning public debt management with private capital markets.

In theory, this alignment made sense. By converting illiquid government bonds into tradable shares, the state could simplify its obligations. By linking those shares to a company with trade privileges, investors could hope for upside beyond fixed interest.

The problem was that political incentives and market incentives became entangled. Directors sought higher share prices to facilitate further debt conversions. Politicians wanted the scheme to succeed to stabilize public finances. Investors interpreted official support as validation of value.

When finance and politics intertwine, price signals can become distorted. A rising share price may reflect political momentum rather than underlying cash flows. Investors may struggle to disentangle genuine economic prospects from policy-driven enthusiasm.

This dynamic remains relevant. When central banks purchase large quantities of assets, or when governments provide guarantees to certain industries, asset prices incorporate political commitments. That incorporation can stabilize markets, as seen when central banks act as lenders of last resort. It can also encourage risk-taking if investors believe losses will be socialized.

The South Sea Bubble was one of the earliest large-scale demonstrations of this duality. State credibility fueled speculation. The same credibility, once questioned, intensified the fallout.

Here the "abstraction trap" appears clearly. Investors traded claims on future government revenues and imagined trade profits. As long as everyone believed, those paper claims moved like concrete wealth. When belief wavered, people remembered that the claims were just promises. Their value evaporated faster than any underlying asset could decline.

A Comparative Lens: The Mississippi Bubble

While Britain experienced the South Sea Bubble, France underwent a parallel episode under the economist John Law. Law's Mississippi Company also consolidated government debt and issued shares. French investors similarly experienced euphoria and collapse.

But the aftermath differed dramatically. In Britain, political institutions remained intact. Parliament investigated, punished some wrongdoers, and restructured the company's finances. British state credibility survived. The national debt was still honored.

In France, the collapse discredited the monarchy's financial management more deeply. Trust in state credit was severely damaged. France's fiscal problems would fester, contributing to the revolutionary pressures later in the century.

This comparison sharpens the structural argument: political structure determines post-crisis recovery. Where institutions are resilient and accountable, trust can be rebuilt. Where they are fragile and arbitrary, the damage lingers.

The Aftermath: Institutional Reform and Survival

Despite the scale of the bubble, Britain's financial system did not collapse permanently. The state's borrowing credibility survived. How?

First, Parliament moved quickly. Directors were investigated. Some had their estates confiscated, and the proceeds were used to compensate investors. The political system demonstrated that it could respond to failure.

Second, the South Sea Company was restructured rather than liquidated. Its shares continued to trade, though at much lower values. The company's operations were separated from its speculative excesses.

Third, the Bank of England remained stable throughout. The competition between the South Sea Company and the Bank had been fierce, but the Bank's more conservative structure insulated it from the worst of the frenzy.

Fourth, the government did not repudiate its debt. The underlying obligation to pay interest remained. Creditors understood that the state would still honor its promises, even if the speculative superstructure had collapsed.

The paradox is important: a severe speculative bubble can occur without destroying the underlying creditworthiness of the state. Trust in the government's long-term commitment to pay its debts proved more resilient than trust in the shares of a company entangled with that government.

This resilience matters for modern investors. It suggests that institutional credibility, built over decades, can survive even dramatic failures in specific markets. The key is whether the institutions themselves remain intact and accountable.

Conclusion: Trust as Power, Trust as Risk

The South Sea Bubble unfolded in a Britain learning how to harness credit and political legitimacy to build national power. The episode shows how state credibility can lower borrowing costs, mobilize capital, and create new financial instruments. It also shows how that credibility can magnify speculation when public guarantees and private profit become closely linked.

From this episode, we draw several lessons:

State credibility is capital. When a government's promise is trusted, it can mobilize private savings at scale. That capacity is a national asset. But that same credibility can distort private markets when it becomes implicit backing for speculative ventures.

Political endorsement amplifies herding. When investors believe the state supports an asset, they may suspend normal caution. The coordination problem intensifies: each buyer assumes others will keep buying, because political backing seems to guarantee it.

Moral hazard follows explicit or implicit guarantees. If investors believe they are protected from downside, they take more risk. That risk-taking pushes prices higher and embeds more leverage, making the system more fragile when confidence eventually shifts.

Liquidity creates an illusion of safety. Assets that can be traded daily feel safer than illiquid ones. But that liquidity can vanish when everyone tries to sell at once. The very feature that attracts investors becomes the channel for panic.

Trust has a tipping point. The trust thermocline is real. Confidence can seem stable until it isn't. When it breaks, the shift is abrupt, not gradual.

Financial abstraction creates distance from reality. The abstraction trap—trading claims detached from underlying assets—makes prices vulnerable to rapid revision when belief falters.

Political structure shapes recovery. Britain's institutions survived the bubble because they were accountable and resilient. France's more fragile monarchy suffered lasting damage. The quality of institutions matters as much as the scale of the crisis.

At its heart, the bubble was about coordination and trust. Individuals acted on reasonable assumptions about state backing and collective behavior. As long as confidence held, prices soared. When confidence broke, the fusion of finance and politics turned a market crash into a political scandal.

The names and instruments change. The underlying human behavior does not.

In the next installment of this series, we will move forward in time to examine another moment when financial innovation, political structures, and human behavior combined to produce both progress and instability—and we will continue exploring how trust remains the invisible architecture beneath every market.

Further Reading

- The South Sea Bubble by John Carswell – a detailed narrative history

- Famous First Bubbles by Peter Garber – comparative analysis of early bubbles

- Manias, Panics, and Crashes by Charles Kindleberger – the classic work on financial crises

- This Time Is Different by Carmen Reinhart and Kenneth Rogoff – broader context on debt and crises

- A Financial History of Western Europe by Charles Kindleberger – institutional context for Britain and France

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.