Tutorial Categories

Last Updated: January 31, 2026 at 19:30

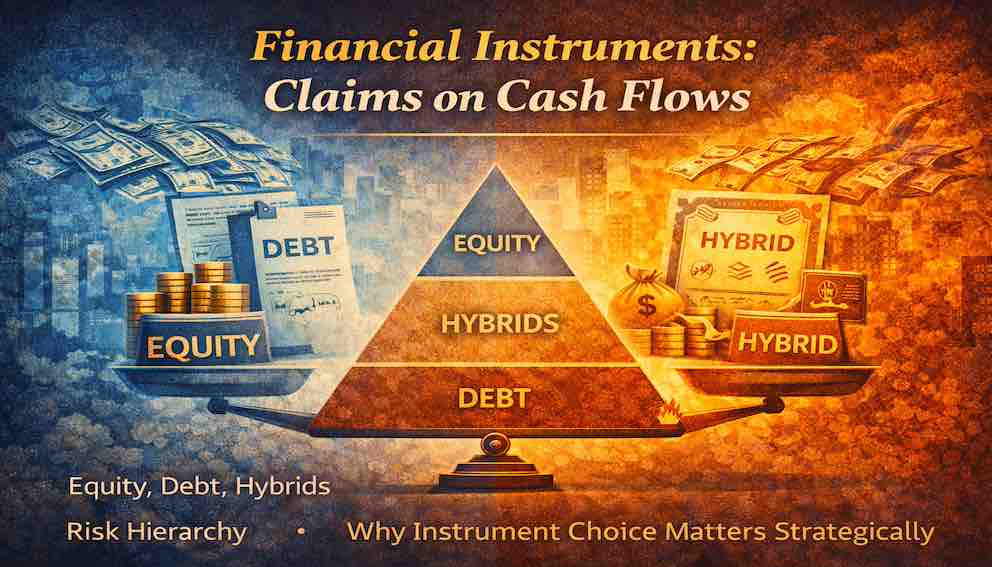

Financial Instruments: Claims on Cash Flows — How Equity, Debt, and Hybrids Shape Risk, Control, and Outcomes - Corporate Finance Series

Financial instruments are not just funding tools; they are the legal and economic architecture that dictates who wins and who loses in a business. This tutorial explains how equity, debt, and hybrids create a strict hierarchy of claims on cash flows, fundamentally shaping risk-taking, managerial control, and corporate survival. You'll learn to see a balance sheet not as a snapshot of value, but as a dynamic map of incentives and vulnerabilities. Through real-world examples, we demonstrate why the “cheapest” capital is often the most dangerous and how the wrong financial structure can turn a temporary setback into a terminal crisis.

Introduction: The Hidden Blueprint of Every Business

Throughout this series, we have explored what to do with capital: invest for growth, return it in maturity, and harvest it in decline. But beneath these strategic choices lies a more foundational one: in what form should capital enter the firm?

Capital is never neutral. It arrives as equity, debt, or a hybrid, and each instrument is a contract that makes a specific promise about risk, reward, and control. Choosing between them is not a technical financing decision; it is a core strategic act that pre-determines how the company will behave under pressure and who will decide its fate in a crisis.

To master corporate finance, you must learn to read the hidden blueprint of the balance sheet. This tutorial provides that lens.

The Cash Flow Waterfall: A Map of Economic Priority

At its core, a firm is a cash-flow generator. Financial instruments are simply the legal rules that determine the order of payment from that stream. Imagine a waterfall where cash flows in at the top.

The parties are paid in this strict, unchangeable sequence:

- Operating Claims: Employees, suppliers, taxes.

- Senior Secured Debt: Bank loans (backed by specific assets like factories or inventory).

- Senior Unsecured Debt: Corporate bonds.

- Subordinated Debt & Hybrids: Junior debt, convertible notes.

- Preferred Equity: Equity with a dividend priority.

- Common Equity: The residual owners.

Your position in this waterfall defines everything: your risk, your potential reward, and your power. Those at the top sleep well; those at the bottom own the future—or the ruins.

Equity: The Residual Claim (The Foundation of Risk)

What It Is: Equity is the residual claim. It is not a claim to cash flows, but to what remains after every superior claim in the waterfall has been paid in full.

Its Economic Role: The Ultimate Shock Absorber.

Equity's position at the bottom makes it the financial system's primary risk-bearing layer. When revenues fall, equity value cushions the blow for all claimants above it. This is why it demands high expected returns—it is paid for bearing the full, undiluted uncertainty of the business.

Its Strategic Character: Control and Optionality.

Because equity bears the residual risk, it typically holds residual control. Equity holders vote, appoint directors, and approve major decisions. This alignment of risk and control is deliberate. In a startup, this is crucial: equity provides maximum strategic optionality because it carries no mandatory payments that could force a bad decision during tough times.

Real-World Lens: Tesla in 2018.

In 2018, Tesla was burning billions and missing production targets. As a pure-equity-funded company, it had no mandatory interest payments to miss. This gave it the optionality of time—a critical few quarters to solve production hell. A heavily indebted company would have been forced into restructuring by creditors. Equity, while dilutive, bought survival.

Debt: The Fixed Claim (The Engine of Discipline and Fragility)

What It Is: Debt is a fixed, senior claim. It promises specific payments at specific times, with priority over equity. Its payoff is asymmetric: limited upside (the interest rate), severe downside (default).

Its Economic Role: Imposing Discipline.

Debt is not patient capital. Its fixed payments force relentless focus on cash flow generation and cost control. This can be immensely valuable for mature, stable businesses (like a utility or a branded consumer goods firm), preventing managerial waste and empire-building. The threat of covenant breaches keeps management aligned with creditor interests—which are primarily about capital preservation.

Why Debt Works for Some, Not Others: The Role of Assets.

The safety of debt depends on what backs it. Lenders tolerate more leverage in a utility or a railroad because loans are secured by tangible, durable assets (power plants, rail lines) that retain value in distress. Conversely, lending to an asset-light software or media company is riskier; the collateral is intangible (code, brand) and can evaporate. This is why lenders allow high debt for utilities but demand low debt for retailers—it’s not just about cash flow predictability, but about what can be seized and sold.

Its Strategic Character: The Sword of Damocles.

The discipline of debt is also its danger. It amplifies business risk into financial risk. A modest downturn can trigger a cash shortfall, a covenant breach, and a loss of control to lenders. Debt removes optionality just when you need it most.

Real-World Lens: Toys "R" Us vs. Amazon.

In the 2000s, both companies faced the existential threat of e-commerce.

- Toys "R" Us: Burdened by billions in leveraged buyout debt, it had no strategic flexibility. Every dollar of cash flow was committed to interest payments, leaving nothing to invest in a competitive e-commerce platform. Debt strangled its ability to adapt.

- Amazon: Funded almost entirely by equity, it had the optionality to invest relentlessly in logistics, AWS, and Prime—initiatives that lost money for years but built an unassailable moat. Debt would have killed this strategy.

The "cheap" debt of the LBO wasn't cheap; it was a claim on the company's future that prevented it from having one. This is why textbook cost-of-capital optimization often fails in real companies—it ignores the strategic cost of lost flexibility.

The Hierarchy in Crisis: When Structure Becomes Destiny

In good times, the capital structure is silent. In distress, it screams. Control doesn't vanish; it travels up the waterfall to whoever is now bearing the imminent loss.

Mechanism of Transfer:

- Equity is wiped out (absorbs losses).

- Debt becomes the new "residual claimant" and demands control.

- This happens through covenant enforcement, debt-for-equity swaps, or bankruptcy proceedings.

Clash of Incentives: The "Gambling for Resurrection" Problem

In distress, incentives fatally diverge:

- Equity Holders (Nearly Wiped Out): Prefer high-risk, high-reward "Hail Mary" plays. They have little left to lose.

- Debt Holders (Now at Risk): Prefer safe, asset-preserving strategies to salvage some repayment.

This clash is exacerbated by management’s personal incentives. Executives with equity-heavy compensation may roll the dice to save their wealth, while those focused on job preservation may make short-term decisions to please creditors, even if they destroy long-term value.

This isn't about morality; it's about the mechanical payoff of their instruments. The company often makes disastrous bets simply because its capital structure forces it to.

Real-World Lens: Chesapeake Energy (2020 Bankruptcy).

The fracking giant, laden with debt from the shale boom, faced collapsing oil prices in 2020. To avoid breaching covenants, management was incentivized to keep drilling to generate immediate cash flow, even as it burned long-term value and flooded a glutted market. Equity wanted the gamble; debt demanded the cash. The structure forced a value-destroying strategy, culminating in a bankruptcy where debt holders took control and equity was wiped out.

Hybrids: Negotiated Truces in the War of Incentives

Hybrids exist because the clean dichotomy of debt and equity often doesn't match messy reality. They are bespoke contracts that split the difference.

- Convertible Debt: "Acts like debt, thinks like equity." It provides downside protection (seniority, interest) but gives the option to participate in upside via conversion. It's perfect for high-growth, hard-to-value companies (e.g., a Series B tech startup), as it delays the valuation argument until more information is available.

- Preferred Equity: "Equity with a priority lane." It sits above common equity in the waterfall, often with a fixed dividend, making it palatable to investors who want some protection (like VC firms) without the rigidities of debt.

Hybrids are not "free lunches." They are complex compromises that can create their own conflicts, especially around triggering conversion or redemption features.

Instruments Across the Lifecycle: Matching Structure to Reality

The optimal capital structure is not static; it evolves with the firm's risk profile.

| Lifecycle Stage | Dominant Risk | Optimal Instrument | Why It Fits |

| Startup | Survival / Product-Market Fit | Pure Equity (Founder, Angel, VC) | Preserves optionality; no fixed payments to cause death during uncertainty. |

| Growth | Execution / Scaling Economics | Equity + Selective Convertibles | Funds growth while delaying valuation; begins to introduce light discipline. |

| Maturity | Complacency / Capital Efficiency | Strategic Debt + Equity Returns | Debt enforces cash discipline; surplus equity is returned via buybacks/dividends. |

| Decline | Harvest / Liquidation | Simplified Capital Structure | Complex debt layers cause destructive conflict. Simplify to harvest or wind down cleanly. |

Applying the Lens: Netflix's Structural Evolution.

- Startup/Growth: Funded by equity (VC) and convertible debt. Structure preserved optionality to experiment with streaming.

- Hyper-Growth: Issued billions in high-yield bonds. Why? Its subscription model generated predictable, recurring cash flows—the only kind that can safely service high debt. The debt funded a content war without diluting founders.

- Maturity (Today): As growth slows, the sustainability of its debt load is the central financial question. The instrument chosen in the growth stage now dictates its strategic constraints.

Conclusion: Finance as the Allocation of Losses

The essence of finance is not the pursuit of upside, but the prudent allocation of downside. Financial instruments are the tools for this allocation. They decide, in advance, who will bear losses and who will gain control when plans fail.

Therefore, capital structure is a pre-written script for a crisis. A strong balance sheet (equity-heavy) gives you the option to fight another day. A fragile one (debt-heavy) writes a script where lenders take the pen.

The master allocator knows:

- Equity is not expensive; it is insurance against uncertainty.

- Debt is not cheap; it is a claim on your future flexibility.

- The goal is not to minimize a theoretical cost of capital, but to maximize strategic optionality across the entire range of possible futures.

Choose your instruments not for how they make your P&L look today, but for the company they will force you to become tomorrow.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.