Tutorial Categories

Last Updated: February 26, 2026 at 10:30

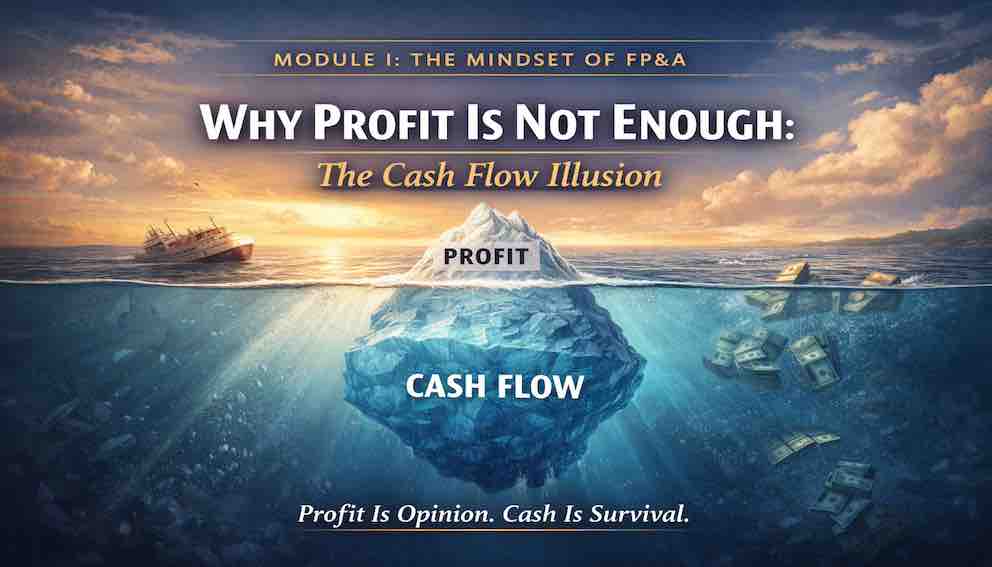

Why Profit Is Not Enough: Cash Flow, Liquidity Risk, and the Hidden Fragility Behind Accounting Profits

Many businesses proudly report rising profits and strong EBITDA, yet still find themselves struggling to pay suppliers, employees, or lenders. This tutorial explains in depth why profit does not equal cash, and why liquidity—not accounting income—determines survival. We walk carefully through the mechanics of accrual accounting, working capital timing, capital expenditure, the cash conversion cycle, and the structure of the cash flow statement itself. Through clear numerical examples and step-by-step reconciliation from profit to cash, you will see how companies can appear healthy while quietly approaching a liquidity crisis. The principle anchoring everything is simple but decisive: profit is opinion, but cash is survival.

Returning to the Boardroom: Where the Illusion Begins

Let us return to Sarah(the Financial Planning & Analysis Lead).

She sits in the quarterly review meeting, listening as the leadership team discusses performance. Revenue has grown by 30 percent year over year. Gross margins have improved. EBITDA has increased by 40 percent. The income statement presents a clean narrative of progress.

The CEO leans back in his chair and says, “This is what execution looks like.”

There is relief in the room. The numbers look strong. After months of operational strain, the company appears to be thriving.

Sarah does not interrupt the celebration. But she is not looking at the income statement. She is looking at the cash flow statement and the rolling liquidity forecast she updates weekly. She has noticed that the bank balance has declined steadily for six weeks. She has modeled payroll increases against delayed customer collections. She has reviewed the upcoming capital expenditure commitment that will require a significant payment next month.

The CEO sees profit.

Sarah sees pressure.

This divergence is not rare. It is not unusual. It is not even dramatic in its early stages. It is simply the natural result of confusing accounting performance with financial endurance.

And that confusion is one of the most common causes of corporate failure.

Profit Is an Accounting Construct. Cash Is a Physical Constraint.

Profit is calculated under accrual accounting. Accrual accounting was developed for a legitimate and important purpose: to measure economic performance during a period by recognizing revenue when it is earned and expenses when they are incurred, rather than when cash moves.

This matching principle gives us a clearer picture of operational performance. Without it, results would fluctuate wildly depending on payment timing.

But accrual accounting does not change one stubborn fact.

Cash moves when it moves.

To understand the gap, Sarah walks a new analyst through a simple scenario.

The company sells enterprise software licenses worth £1,000,000 in March. Customers receive 60-day payment terms. The costs of delivering those licenses—engineering time, hosting infrastructure, commissions—amount to £700,000 and are recorded in March.

The income statement shows £300,000 in profit.

Now comes the critical question.

How much cash has the company received from customers by the end of March?

None.

If customers pay exactly on time, cash arrives in May. Meanwhile, the company has already paid salaries for March and April. It has paid rent, utilities, software subscriptions, and marketing vendors. Cash has left the building.

The income statement shows strength.

The bank account shows decline.

Accounting is not wrong. It is answering a different question. Profit answers whether value was created during a period. Cash answers whether the organization can continue operating long enough to realize that value.

Confusing those two questions creates strategic blindness.

How the Cash Flow Statement Reconciles Profit to Reality

At this point, Sarah slows down and introduces something foundational: the structure of the cash flow statement.

The cash flow statement exists precisely because profit alone does not explain changes in liquidity.

It is divided into three sections:

- Operating cash flow

- Investing cash flow

- Financing cash flow

Let us walk through how profit becomes—or fails to become—cash.

Imagine the company reports £1,000,000 in net income for the year.

We begin with that net income.

First, we adjust for non-cash expenses. Depreciation of £400,000 is added back because it reduced profit but did not consume cash this year.

So now we are at £1,400,000.

Next, we adjust for working capital movements.

If receivables increased by £600,000, that means revenue was recognized but cash has not yet been received. So £600,000 is subtracted.

If inventory increased by £500,000, that means cash was spent building stock not yet sold. So another £500,000 is subtracted.

If payables increased by £300,000, that means the company delayed paying suppliers. That preserves cash, so £300,000 is added.

Now operating cash flow becomes:

£1,000,000

- £400,000 depreciation

- – £600,000 receivables increase

- – £500,000 inventory increase

- £300,000 payables increase

Operating cash flow equals £600,000.

Notice what just happened.

The company reported £1,000,000 in profit. But only £600,000 in operating cash was generated.

Then we move to investing activities.

If the company spent £900,000 on capital expenditure during the year, that £900,000 leaves the bank.

Now we are at negative £300,000 in free cash flow.

Finally, financing activities.

If the company borrowed £500,000 from its credit facility, cash increases by £500,000.

The net change in cash becomes £200,000 positive.

The income statement alone would never reveal this chain of events. Only the cash flow statement shows how profit interacts with timing, investment, and financing.

This is the formal architecture that connects accounting performance to liquidity reality.

EBITDA and the Comfort of Partial Truth

In boardrooms, EBITDA often receives applause. It excludes interest, taxes, depreciation, and amortization. It presents a cleaner measure of operational profitability.

But EBITDA removes three categories that matter deeply to liquidity.

First, depreciation represents past capital expenditure and signals future replacement needs. Capital-intensive businesses require ongoing cash investment to sustain operations.

Second, interest payments are real cash obligations. A highly leveraged company may show impressive EBITDA while most of its operating cash is consumed servicing debt.

Third, taxes are not theoretical. They are cash payments triggered by taxable income.

EBITDA simplifies. Liquidity complicates.

EBITDA is useful for comparing operational efficiency across firms. But it cannot answer the survival question.

Working Capital and the Cash Conversion Cycle

Working capital is where timing differences become operational risk.

Working capital includes receivables, inventory, and payables. Together, they form what is known as the cash conversion cycle.

The cash conversion cycle measures how long cash is tied up in operations before returning to the company.

Consider a company where:

Customers take 60 days to pay.

Inventory sits 45 days before being sold.

Suppliers require payment in 30 days.

This means the company must finance 75 days of operations with its own cash.

Here is how that number emerges.

Inventory sits 45 days before sale.

After sale, customers take 60 days to pay.

So from the moment inventory is purchased to the moment cash is received, 105 days pass.

But suppliers allow 30 days before payment.

So the company must finance 105 minus 30, which equals 75 days of activity.

If daily operating expenses equal £100,000, the company must fund £7,500,000 in working capital just to operate normally.

Now imagine sales grow rapidly. Receivables increase. Inventory increases. If payment terms do not improve, the required financing grows proportionally.

Growth amplifies working capital requirements.

The income statement celebrates expansion. The cash conversion cycle quietly absorbs liquidity.

Capital Expenditure and Free Cash Flow

Capital expenditure is another dimension of the profit illusion.

When the company invests £3,000,000 in a warehouse, that full amount leaves the bank immediately. Yet the income statement may reflect only £150,000 in annual depreciation.

This difference highlights the importance of free cash flow.

Free cash flow is calculated as operating cash flow minus capital expenditure.

It represents the cash remaining after maintaining and expanding the asset base required to operate.

A company may show strong net income and positive operating cash flow, but if capital expenditure consistently exceeds operating cash flow, free cash flow is negative. Over time, that gap must be financed through debt or equity.

Free cash flow determines financial flexibility. It determines whether the company can reduce debt, return capital, or reinvest strategically.

Profit may suggest success. Free cash flow reveals sustainability.

Accounting Health Versus Financial Health

Sarah explains the difference clearly.

Accounting health reflects reported earnings, margins, and return metrics. It depends on revenue recognition policies, expense matching, depreciation schedules, and accounting estimates such as bad debt provisions.

These estimates involve judgment. Revenue recognition can accelerate or defer profit. Capitalizing costs rather than expensing them increases reported earnings. Adjusting depreciation assumptions changes net income.

In this sense, profit contains elements of opinion.

Financial health, by contrast, reflects liquidity strength. It depends on:

Cash balances available today.

Unused credit capacity.

Debt maturity schedules.

Covenant requirements.

Cash conversion efficiency.

Banks do not rely solely on net income when evaluating risk. They examine liquidity ratios, interest coverage, and covenant compliance.

A company can report profit while approaching a covenant breach if EBITDA declines slightly or debt increases. Covenant violations can trigger immediate repayment obligations, accelerating liquidity crises.

Financial health answers the question: can we meet obligations when they come due?

Accounting health answers the question: did we create value during this period under reporting standards?

Both matter. But only one determines survival.

Why Profitable Companies Collapse

Sarah recounts the construction firm she studied earlier in her career.

The company reported profit for three consecutive years. Contracts were profitable on paper. Revenue increased steadily.

But customers paid slowly. Receivables ballooned. Subcontractors demanded payment weekly. Suppliers shortened payment terms after hearing rumors of strain.

The company borrowed against receivables to bridge the gap. Interest expense rose. Cash tightened further.

Eventually, the bank refused additional credit. Without cash to meet payroll, operations stopped.

The income statement said profit.

The bank account said insolvency.

The collapse was not caused by lack of margin. It was caused by timing.

Cash failure precedes accounting failure.

The Vulnerability of Fast-Growing Companies

Fast-growing companies face amplified liquidity strain.

Growth requires hiring before revenue materializes fully. It requires inventory purchases before sales occur. It requires infrastructure investment before efficiency gains appear. It often requires extending credit to attract customers.

Each of these actions consumes cash before generating it.

Suppose revenue doubles from £5,000,000 to £10,000,000. Profit doubles from £1,000,000 to £2,000,000.

But receivables double. Inventory doubles. Marketing expenses are paid upfront. Payroll increases immediately.

The company may need several million pounds of additional liquidity to support expansion.

If access to credit tightens or investors hesitate, the company can stall or collapse despite strong margins.

Growth without liquidity planning is acceleration without fuel assurance.

Liquidity Metrics and Runway

Sarah frequently asks a question that cuts through accounting abstraction.

“If all revenue stopped tomorrow, how long could we continue?”

This question introduces the concept of runway.

Runway equals available liquidity divided by monthly cash burn.

Liquidity includes cash on hand plus unused committed credit facilities.

Burn rate includes payroll, fixed costs, debt service, and essential supplier payments.

If liquidity equals £6,000,000 and monthly burn equals £1,000,000, runway is six months.

Profit does not answer this question.

Cash does.

Liquidity ratios such as the current ratio and quick ratio provide signals, but they must be interpreted alongside timing realities. Receivables may inflate the current ratio, but if collections are slow, liquidity remains fragile.

True financial resilience requires disciplined liquidity monitoring, not comfort derived from profit alone.

Translating Strategy into Liquidity Discipline

The purpose of FP&A, as we established in the previous tutorial, is to translate strategy into cash consequences.

When leadership proposes expansion, Sarah models the working capital absorption before revenue contribution.

When new equipment is approved, she models the cash payback period and financing impact.

When acquisitions are discussed, she analyzes not just EBITDA accretion but debt capacity, covenant headroom, and free cash flow implications.

Liquidity is not a by-product of profit. It is a parallel discipline.

Strategy without liquidity modeling is ambition without oxygen.

Conclusion: Profit Is Opinion. Cash Is Survival.

In this tutorial, we examined the structural divergence between accounting profit and liquidity reality.

We walked through how accrual accounting recognizes revenue and expenses independently of cash timing. We reconciled net income to operating cash flow step by step and saw how working capital movements alter liquidity outcomes. We explored how capital expenditure creates immediate cash outflows while appearing gradually through depreciation. We introduced the cash conversion cycle and understood how growth lengthens liquidity demands. We examined free cash flow as the measure of sustainable financial flexibility. We distinguished accounting health from financial health and recognized how covenant pressure can intensify risk even when profits appear solid.

Profit measures performance under reporting standards shaped by judgment and estimation. It contains interpretation.

Cash reflects the physical capacity to pay obligations. It contains no interpretation.

Financial Planning & Analysis exists to ensure those two narratives remain aligned. It exists to prevent strategic ambition from outrunning financial endurance.

As Sarah reminds her team:

The income statement tells you how well you performed.

The cash flow statement tells you how long you can continue.

When those stories diverge, survival belongs to cash.

Profit is opinion.

Cash is survival.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.