Tutorial Categories

Last Updated: February 26, 2026 at 10:30

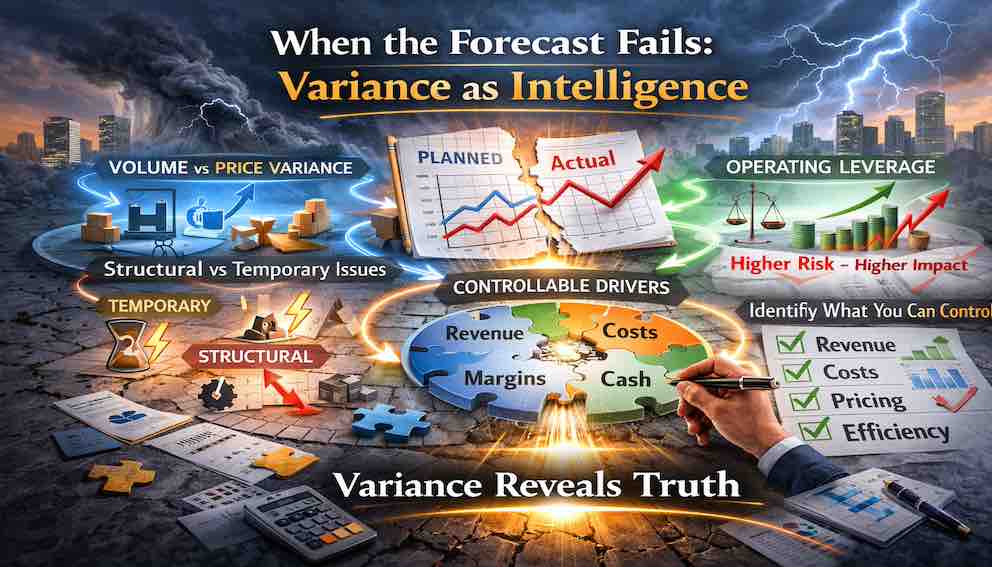

When the Forecast Fails: Variance as Intelligence in Financial Management

Forecasts rarely match reality, and the gap between expectation and outcome contains crucial lessons for financial managers. This tutorial teaches how to interpret variances intelligently rather than dismissing them as errors or failures. Learners will explore volume versus price variance, structural versus temporary deviations, operating leverage impacts, variance interactions, and how to identify controllable drivers. By understanding variance as a source of insight, managers can refine judgment, improve future forecasts, and strengthen strategic decision-making. Ultimately, this lesson bridges the gap between survival-focused liquidity management and the analytical maturity required for sustained financial leadership.

Introduction: From Forecasting to Learning

Sarah(the Financial Planning & Analysis Lead) sits at her desk on a quiet Friday afternoon, reviewing the monthly close package. The numbers are final, the reports complete. The forecast, updated just three weeks ago, sits beside the actual results.

They don’t match. They never do.

Revenue came in 4 percent below forecast. Operating expenses were 2 percent higher. The gap between what she expected and what actually happened is visible in every line.

A less experienced version of Sarah might have panicked. She might have worried about the CEO’s reaction or her own forecasting skills. She might have looked for someone to blame.

But Sarah knows forecasts are not promises—they are hypotheses. They represent her best guess, based on available information, about what the future might hold. When reality differs from the hypothesis, that difference is not failure. It is data. It is intelligence.

The 13-week cash flow model, studied in the previous tutorial, teaches the discipline of monitoring cash, protecting the organization from unexpected crises, and ensuring survival under uncertainty. However, even the most carefully constructed forecast rarely unfolds exactly as planned. Revenue may come in lower than expected, expenses higher, or payments delayed. Uncertainty is unavoidable. Forecasts will fail. The key question is not whether variances will occur, but how intelligently we respond to them.

Variance analysis is the tool that allows managers to transform deviations into insight, revealing how the business behaves under real-world conditions.

Variance as a Learning Mechanism

At its core, variance analysis is about learning from reality. Forecasts reflect expectations; variances reflect reality. This distinction is subtle but critical.

Consider a simple example: A company forecasts 10,000 units sold at $50 per unit, expecting revenue of $500,000. Actual sales are 9,000 units at $52 per unit, yielding $468,000.

The total revenue variance of $32,000 below forecast might initially appear as underperformance. But by separating the effects of volume and price, a richer story emerges: the company sold fewer units than planned, but each unit sold at a higher price. Demand underperformed, yet pricing strength suggests market value remains high.

This insight guides management focus: investigate why volume declined—perhaps marketing or distribution issues—while recognizing pricing discipline as a positive signal. Variance analysis transforms deviation from a “problem” into actionable intelligence.

Volume and Price Variance

Breaking down total variance into its components is essential:

- Volume variance measures the impact of selling more or fewer units than forecasted.

- Price variance measures the impact of selling at a higher or lower price than expected.

Returning to our example:

- Forecast: 10,000 units × $50 = $500,000

- Actual: 9,000 units × $52 = $468,000

- Volume variance: (9,000 – 10,000) × $50 = –$50,000

- Price variance: ($52 – $50) × 9,000 = +$18,000

- Net variance: –$32,000

By decomposing variance, managers can focus corrective action where it is most needed. Volume shortfalls may point to operational, marketing, or competitive challenges. Favorable price variance may indicate pricing power or disciplined sales behavior, highlighting strengths that can be leveraged elsewhere.

Temporary vs. Structural Variances

Not all variances are created equal. Some are temporary, caused by timing differences or one-off disruptions, while others are structural, indicating permanent shifts. Understanding this distinction determines the appropriate response.

- Temporary variances are transient. A delayed customer order, machinery downtime, or storm-related store closures may temporarily affect numbers but not the overall trend.

- Structural variances are lasting. A declining market segment, competitor entry, regulatory change, or lasting shift in customer behavior signals a permanent change requiring strategic intervention.

Sarah recalls a manufacturing client: a one-time machinery breakdown reduced output for a month—a temporary variance easily corrected. Later, a consistent decline in demand for a legacy product revealed a structural variance caused by new competitor technology, prompting product redesign and market repositioning.

Identifying the type of variance prevents misallocation of attention. Acting on temporary deviations as if they were permanent can waste resources, while ignoring structural issues risks crisis escalation.

Operating Leverage and Variance Amplification

Operating leverage explains how a company’s cost structure can amplify small changes in revenue into disproportionately large changes in profit. The mechanism behind this amplification is the presence of fixed costs.

Fixed costs do not change when revenue changes. They remain constant whether the company sells one unit or ten thousand. Because of this rigidity, once fixed costs are covered, additional revenue contributes directly to profit. But if revenue declines, fixed costs do not decline with it. The burden remains.

To understand this clearly, consider a simplified example.

Assume the following:

- Selling price per unit: $50

- Variable cost per unit: $20

- Contribution margin per unit: $30

- Fixed monthly costs: $300,000

Now let us determine the breakeven point.

Breakeven occurs when total contribution equals fixed costs. Each unit contributes $30 toward covering fixed costs. To cover $300,000 in fixed costs, the company must sell:

$300,000 ÷ $30 = 10,000 units

So at 10,000 units, the company breaks even.

Let us examine what happens around that breakeven level.

At 10,000 units:

- Revenue = 10,000 × $50 = $500,000

- Variable costs = 10,000 × $20 = $200,000

- Contribution margin = $300,000

- Fixed costs = $300,000

- Profit = $0

Now suppose sales fall by 10 percent, from 10,000 units to 9,000 units.

At 9,000 units:

- Revenue = 9,000 × $50 = $450,000

- Variable costs = 9,000 × $20 = $180,000

- Contribution margin = $270,000

- Fixed costs = $300,000

- Loss = $30,000

A 10 percent decline in revenue produces a shift from breakeven to a $30,000 loss.

Now consider the opposite direction. Suppose sales increase by 10 percent, from 10,000 units to 11,000 units.

At 11,000 units:

- Revenue = 11,000 × $50 = $550,000

- Variable costs = 11,000 × $20 = $220,000

- Contribution margin = $330,000

- Fixed costs = $300,000

- Profit = $30,000

A 10 percent increase in revenue produces a $30,000 profit.

This is operating leverage in action. Around the breakeven point, small percentage changes in revenue create proportionally larger swings in profit. The reason is structural. Fixed costs create a threshold effect. Once that threshold is crossed, profit accelerates upward. When revenue falls below it, losses accumulate quickly.

The effect becomes even more dramatic in businesses with very high fixed costs relative to contribution margin. Airlines, software platforms, manufacturing plants, logistics networks, and subscription-based businesses often operate with significant operating leverage. In such environments, modest revenue variance is never “just” a small deviation. It may signal meaningful profit risk.

This is why variance analysis cannot stop at revenue. A 5 percent shortfall in sales may appear manageable in isolation. But if the organization operates close to breakeven and carries high fixed costs, that 5 percent variance may translate into a disproportionately large decline in operating income.

Understanding operating leverage changes how managers interpret variance. It sharpens sensitivity to early warning signs. It encourages proactive monitoring when revenue drifts below forecast. And it reinforces the importance of understanding cost structure, not just top-line performance.

Operating leverage teaches a powerful lesson: not all revenue variances are equal. Their impact depends on where the organization sits relative to its cost structure.

And that insight is exactly what variance analysis is designed to uncover.

Controllable vs. Uncontrollable Drivers

Effective variance analysis distinguishes between what management can influence and what it cannot.

- Controllable drivers include production efficiency, pricing strategy, staffing, marketing spend, and quality control.

- Uncontrollable drivers include macroeconomic shifts, regulatory changes, competitor actions, and natural disasters.

For instance, if unexpected weather reduces retail foot traffic, the weather is uncontrollable. But management can shift marketing to digital channels, adjust inventory, and redeploy staff—controllable actions that mitigate the impact.

Focusing on controllable drivers ensures that attention and resources are directed where they can make a difference.

Variance Interactions: When Multiple Factors Combine

Variances often interact. High fixed costs amplify revenue deviations. Unfavorable volume and price variances together can compound losses, while a favorable price variance may offset a temporary volume decline.

For example, a retailer facing stock-outs (controllable volume variance) and a new competitor undercutting prices (structural price variance) must simultaneously address logistics and strategic market response. Recognizing these interactions prevents simplistic or incorrect reactions and highlights where integrated solutions are needed.

Turning Variance Into Insight: A Systematic Approach

Sarah teaches her team a disciplined five-step method:

- Identify variances – Compare actual outcomes to forecasts across revenue, costs, EBITDA, and cash flow. Even small deviations can signal important trends.

- Decompose variances – Separate into volume, price, cost, and operational effects.

- Classify variances – Determine temporary vs. structural, controllable vs. uncontrollable.

- Analyze causes – Investigate operational, market, and behavioral drivers.

- Apply insights – Adjust forecasts, operational plans, and strategy. Close the loop to improve future performance.

Example: A retail chain forecasts $1,000,000 revenue from 50,000 units at $20 each. Actual: $950,000 from 48,000 units at $19.80.

- Volume variance: –$40,000 (controllable: supplier delays)

- Price variance: –$9,600 (structural: competitor entry)

Action: Improve supplier coordination and design strategic response for competitive pressures.

The Emotional Dimension

Variance analysis is as much about mindset as mechanics. Confronting deviations can trigger defensiveness or ego concerns. Sarah emphasizes that forecasts are hypotheses, not judgments of professional competence.

Approaching variances with curiosity rather than blame transforms analysis into learning. The best financial leaders are those who are excited by variances—they know insight lives there.

Practical Next Steps for Managers

- Maintain a variance journal to track trends and patterns over time.

- Integrate variance review into weekly or monthly leadership meetings.

- Monitor interactions between volume, price, and cost variances to anticipate amplified effects.

- Adjust forecasts and operational plans using insights from prior variance analysis.

- Train teams to adopt a curiosity-first mindset, separating personal ego from financial outcomes.

Conclusion: From Survival to Strategic Judgment

Variance analysis bridges the gap between survival-focused cash flow discipline and strategic, insight-driven financial management. By separating volume and price effects, distinguishing temporary from structural deviations, recognizing operating leverage, and focusing on controllable drivers, managers transform deviations into actionable intelligence.

Connecting variance analysis to prior lessons—strategy translation, economic engines, scenario planning, the 13-week model, and liquidity discipline—reinforces a holistic view of the organization.

Ultimately:

- Visibility protects survival.

- Analysis strengthens judgment.

- Judgment improves future decisions.

By embracing variance as intelligence, managers move from reactive oversight to proactive strategic leadership, learning continuously from every outcome, refining forecasts, and improving decisions.

Sarah stands, stretches, and prepares to present her insights to the leadership team. The variances are not problems—they are signals, guides, and opportunities. And the learning cycle continues.

Because in financial management, variance is where the learning lives.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.