Tutorial Categories

Last Updated: May 7, 2026 at 18:30

Life-Cycle Hypothesis (LCH) Explained: Consumption, Saving, and Retirement Planning in Macroeconomics

A step-by-step guide to how income, age, and expectations shape spending, saving, and retirement decisions

Why does a 25-year-old with a modest income sometimes save while a 55-year-old with a high income spends carefully? The answer lies in where they are on their life journey. The Life-Cycle Hypothesis explains how individuals make decisions about consumption and savings across different stages of life. Instead of reacting only to current income, people think ahead, planning how to maintain a stable standard of living from youth to retirement. This tutorial explores how income tends to rise and fall over time while consumption remains relatively smooth, and why borrowing, saving, and dissaving occur at predictable life stages. By the end, you will understand how individuals balance income, expectations, and time to maintain a stable standard of living.

Introduction: Looking Beyond Today's Income

When we think about how people spend money, it is tempting to assume that individuals simply consume based on what they earn right now. If income rises, spending rises; if income falls, spending falls. This view is simple and appears logical.

But it misses something important. People think about the future.

Consider two neighbours. One is 25 years old, just starting a career as a nurse. The other is 55 years old, a senior manager at a manufacturing firm. The 55-year-old earns nearly three times as much as the 25-year-old. Who do you think saves more each month?

The answer is not obvious. The 55-year-old has higher income but also has children in university, aging parents who need help, and retirement only a decade away. The 25-year-old has lower income but few responsibilities and many years ahead to save. Their saving behavior cannot be explained by looking only at their current paychecks.

The Life-Cycle Hypothesis, developed by the economist Franco Modigliani in the 1950s, provides a framework for understanding exactly these kinds of differences. It suggests that individuals plan their consumption and savings over their entire lifetime, not just based on their current income. A person's spending today is influenced by what they expect to earn in the future, how long they expect to work, and how long they expect to live.

At the most basic level, there is a simple constraint that everyone faces. Over a lifetime, what a person spends cannot exceed what they earn plus any wealth they started with. This is the lifetime budget constraint. It forces people to think ahead. It also means that borrowing in early life is not free. Any amount borrowed must eventually be repaid out of future income. In the same way, saving in middle age is not simply a preference but a necessity, because it finances consumption when income falls later in life.

A Real-Life Story: Margaret the Nurse

To see how this works in practice, consider a woman named Margaret. She is 25 years old and has just qualified as a nurse. Her starting salary is £28,000 per year. She has a small amount of student debt but no significant savings.

Margaret expects her income to rise steadily over her career. She anticipates becoming a senior nurse in her 40s, earning around £45,000 per year. She plans to retire at 68. She expects to live into her mid-80s.

What does Margaret do with her money? She does not spend her entire salary, even though her income is relatively low right now. She saves a small amount each month into a pension plan. Why? Because she is thinking about retirement, which is more than 40 years away.

Now consider Margaret at age 50. She has been promoted several times. She now earns £50,000 per year. Her children have left home. Her mortgage is nearly paid off. She saves aggressively, putting aside a large portion of her income for retirement.

Finally, consider Margaret at age 70. She has retired. Her income has dropped to her state pension and her private pension withdrawals, perhaps £22,000 per year. But her spending has not fallen as much as her income. She still travels, eats out, and enjoys her hobbies. The difference is covered by the savings she accumulated during her working years.

This is the Life-Cycle Hypothesis in action. Margaret borrowed early in life (through student loans), saved heavily in middle age, and now dissaves in retirement.

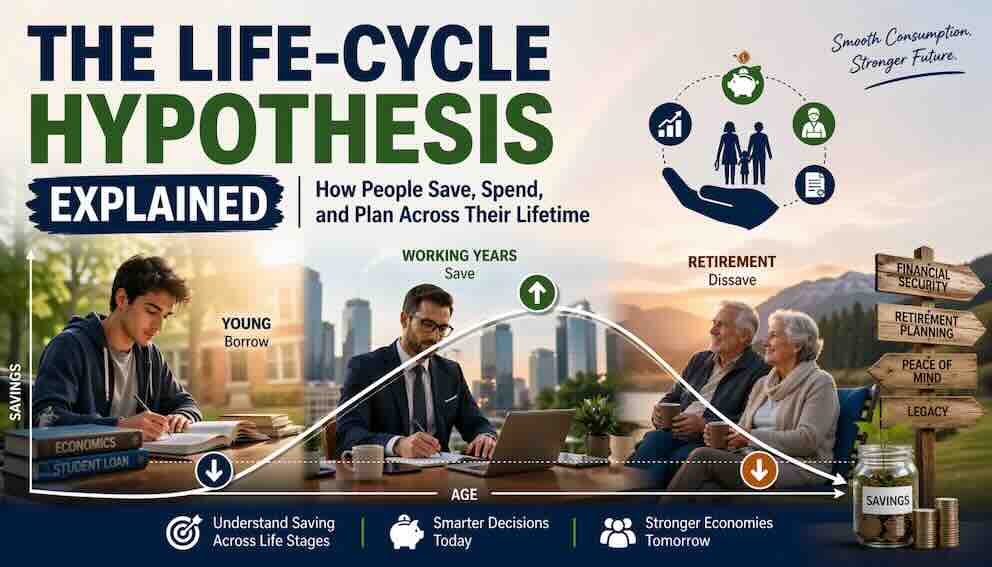

The Three Stages of Financial Life

The Life-Cycle Hypothesis divides a person's life into three broad stages. Each stage has a different relationship between income and consumption.

Stage One: Youth – Low Income, Borrowing

In the early stage of life, individuals typically have low income. They may be in education, just starting their careers, or working in entry-level positions.

Despite this low income, they still need to consume. They need housing, food, transportation, and often education or training. Since their income is insufficient to cover these expenses, they borrow. This borrowing can take many forms: student loans, credit card debt, overdrafts, or help from family.

A medical student is an example. They may have very little income for several years while incurring significant tuition and living costs. They borrow against their expected future earnings as a doctor. This is rational forward-looking behavior.

Stage Two: Middle Age – High Income, Saving

As individuals progress in their careers, their income generally rises. Promotions, experience, and skill development lead to higher earnings. This is typically the period of peak income, often between the ages of 40 and 60.

At this stage, people save a portion of their income. These savings are not simply leftover money. They are part of a deliberate plan to prepare for retirement, when income will fall.

A factory supervisor in their 50s earning a good wage might contribute to a workplace pension, invest in a savings account, and pay down their mortgage. They could increase their current consumption instead. They choose to save because they understand that their income will not remain high forever.

Stage Three: Retirement – Low Income, Dissaving

In retirement, income from work stops. Individuals may receive a state pension, a private pension, or returns from investments. But for most people, this income is lower than what they earned during their peak working years.

At this stage, people begin to use the savings accumulated earlier. They spend more than their current income. This is called dissaving.

A retired teacher might withdraw from their pension fund each month to cover everyday expenses, travel, and leisure activities. Their spending remains relatively stable compared to their working years, even though their income has dropped significantly.

Consumption Smoothing: The Central Goal

Why do people go through this complicated process of borrowing, saving, and dissaving? Why not simply spend whatever they earn each year?

The answer is consumption smoothing. People prefer a stable standard of living over time. They do not want to live richly in their 40s and poorly in their 70s. They want a predictable, comfortable life throughout.

To understand this, imagine two scenarios.

In the first scenario, a person spends exactly what they earn each year. In their 20s, they live frugally because their income is low. In their 40s, they live lavishly because their income is high. In their 70s, they struggle because their income has fallen. Their standard of living rises and falls dramatically.

In the second scenario, the person plans ahead. They borrow in their 20s to maintain a reasonable lifestyle. They save in their 40s rather than spending everything. They use those savings in their 70s. Their standard of living remains relatively stable across their entire life.

The Life-Cycle Hypothesis suggests that most people prefer the second scenario. The first scenario is too unpredictable and uncomfortable. The second scenario requires discipline, but it provides peace of mind.

How Interest Rates Affect Each Life Stage

The decision to save or borrow is not just about timing. It is also about price. The price of moving consumption from the present to the future is the interest rate.

The impact of interest rates depends on where a person is in their life.

For Margaret in her 40s, when she is saving aggressively for retirement, higher interest rates are good news. Her savings grow faster. Each pound set aside today becomes a larger amount in the future. This encourages her to save even more, because the reward for waiting is greater.

For Margaret in her 20s, when she is borrowing for education and training, lower interest rates are helpful. The cost of bringing future income into the present is smaller. This makes it easier for her to invest in her career without being overwhelmed by debt repayments later.

In this way, interest rates do not affect everyone the same way. A policy that raises interest rates might encourage saving among middle-aged households while making life harder for young borrowers. The Life-Cycle Hypothesis helps us see these different effects clearly.

Visualizing the Life Cycle: The Balance Condition

Imagine a simple graph. On the bottom line, from left to right, we measure age, from 20 to 80. On the vertical line, we measure income and consumption in pounds per year.

Income follows a hump-shaped line. It starts low at age 20, rises steadily through the 30s and 40s, peaks in the 50s, and then falls in retirement.

Consumption is a relatively smooth line across the entire lifespan. It does not rise and fall as dramatically as income.

Now look at the gap between the two lines at different ages.

In the 20s, consumption is above income. The gap represents borrowing.

In the 40s and 50s, income is above consumption. The gap represents saving.

In the 70s, consumption is above income again. The gap represents dissaving.

There is a deeper logic here. Over the entire lifetime, the total amount saved during middle age must be sufficient to cover the total borrowing in youth and the total dissaving in retirement. This is the balance condition. It is not optional. If a person does not save enough in middle age, they will face a sharp drop in consumption during retirement. If they save too much, they die with unused wealth, which may be inefficient from their own perspective.

This simple picture captures the entire theory. The gaps in the early and late years are funded by the gap in the middle years.

Where the Model Fits Real Life

The Life-Cycle Hypothesis is a powerful framework, but real life is messier than the model suggests. Several important factors complicate the simple picture.

Uncertainty About Lifespan

The basic model assumes people know exactly how long they will live. In reality, no one knows. Many people fear outliving their savings. This leads them to save more than the basic model predicts. Economists call this precautionary saving against longevity risk.

The Bequest Motive

Not everyone spends all their savings in retirement. Many people want to leave money to their children, grandchildren, or to charity. This is called the bequest motive. It means that some individuals die with significant wealth, contrary to the basic model's assumption that wealth falls to zero at death.

Liquidity Constraints

The basic model assumes people can borrow freely against their future income. In reality, not everyone has access to credit. A young worker who expects higher future earnings may still be unable to borrow for education or a house deposit because banks require current income or collateral. This forces consumption to be more closely tied to current income.

Government Pensions

The basic model assumes individuals must save entirely on their own for retirement. In most advanced economies, the government provides a state pension. This reduces the amount individuals need to save themselves. Countries with generous state pensions tend to have lower private saving rates. Countries with minimal state pensions tend to have higher private saving rates.

Does the Model Actually Hold?

In practice, the Life-Cycle Hypothesis does not perfectly describe all behavior. Many households save less than the model predicts, often because of limited financial literacy, short-term thinking, or unexpected expenses. Others remain heavily dependent on current income because they cannot borrow easily. At the same time, some retirees continue to hold significant wealth rather than spending it down, partly due to uncertainty or the desire to leave a bequest. These patterns suggest that while the Life-Cycle Hypothesis provides a useful benchmark, real-world behavior is shaped by additional psychological and institutional factors.

Connection to the Permanent Income Hypothesis

The Life-Cycle Hypothesis is closely related to Milton Friedman's Permanent Income Hypothesis, which you may have encountered in a previous tutorial.

Both theories emphasize that people are forward-looking and that they aim to smooth consumption over time. Both reject the idea that consumption depends only on current income.

The main difference is that the Life-Cycle Hypothesis explicitly builds in age and retirement. It focuses on the predictable hump-shaped pattern of income over a working life. The Permanent Income Hypothesis is more general. It focuses on expectations about future income without explicitly modeling age.

In practical terms, this means that when economists observe stable consumption despite changing income, they cannot immediately tell whether the explanation lies in lifetime planning (LCH) or expectations about future income (PIH). Both theories predict similar behavior, but for slightly different reasons. Understanding the distinction helps economists design better tests and more accurate models.

The two theories are complementary, not contradictory. Together, they provide a rich understanding of how households make financial decisions.

Why This Matters for Policy

The Life-Cycle Hypothesis has important real-world applications, particularly for pension systems and retirement policy.

Pension systems are designed to help individuals smooth consumption over time. A state pension provides a guaranteed income in retirement, reducing the amount people need to save on their own. Private pension schemes, such as workplace pensions, encourage saving by offering tax advantages and sometimes employer contributions.

Understanding the Life-Cycle Hypothesis helps policymakers design systems that align with how people naturally plan. For example, if people tend to save too little for retirement because they underestimate their lifespan or are overly optimistic about future earnings, governments may introduce automatic enrolment in pension schemes. This is a direct application of the insights from the Life-Cycle Hypothesis.

For individuals, the theory provides a framework for making long-term financial decisions. It highlights the importance of saving during high-income years and planning for future needs. A person in their 30s might focus on paying down student debt and building an emergency fund. A person in their 50s might focus on maximising pension contributions. A person in their 70s might focus on drawing down savings in a sustainable way.

Conclusion: A Lifetime of Planning

The Life-Cycle Hypothesis invites us to see consumption and saving not as isolated decisions but as parts of a broader life strategy. It shows that individuals are forward-looking and that their financial behavior reflects an effort to balance present needs with future security.

By smoothing consumption over time, people aim to maintain stability in their standard of living despite the natural rise and fall of income. They borrow when young, save during their peak earning years, and dissave in retirement. This pattern is not random. It is a rational response to the predictable shape of a working life. And it is governed by a simple balance condition: what is saved in middle age must fund what is borrowed in youth and what is spent in retirement.

The theory also acknowledges that real life is more complex than the basic model. Lifespan uncertainty, the desire to leave wealth to heirs, limited access to credit, and government pensions all modify the simple picture. Many households do not save as much as the model predicts. Others hold onto wealth well into retirement. These deviations are not failures of the theory but opportunities to refine it.

Understanding the Life-Cycle Hypothesis deepens our understanding of individual behavior and provides valuable insights for designing economic policies and financial systems that support long-term well-being. It reminds us that a 25-year-old saving a small amount each month and a 55-year-old saving aggressively are both doing the same thing: preparing for a future they can already see taking shape. And it reminds us that financial well-being depends not only on how much you earn today, but on how you allocate your income across the decades of your life.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.