Tutorial Categories

Last Updated: May 7, 2026 at 18:30

Permanent Income Hypothesis (PIH): How Expectations About Future Income Shape Consumer Behavior

Understanding why people spend based on long-term expectations rather than short-term income changes

Why does a one-time bonus often end up in savings, while a promotion that brings the same annual raise leads to a new car or a bigger apartment? The Permanent Income Hypothesis, developed by Milton Friedman, provides the answer. This tutorial explains how individuals base their spending decisions on their expected long-term income rather than their current earnings. You will learn the difference between permanent and transitory income, why people smooth their consumption over time, and how expectations about the future shape economic behavior. Using real-world examples, including a factory worker's response to overtime pay versus a permanent raise, this guide makes the logic of PIH clear and memorable.

Introduction: Beyond the Paycheck

When we think about how people decide how much to spend, the most natural starting point is to look at how much they currently earn. If someone gets a higher salary this month, it feels intuitive to assume they will spend more. If their income drops, it seems reasonable to expect them to cut back.

This way of thinking is simple and appears logical. But it does not fully capture how people actually behave.

Consider two workers. Both receive an extra £2,000 over the course of a year. One gets a one-time bonus in December. The other receives a permanent raise of £167 per month. Do they spend the money the same way? Almost certainly not. The worker with the bonus might save most of it or use it for a single large purchase. The worker with the raise will likely increase their everyday spending permanently.

Why the difference? Because people think about the future. They distinguish between income that is temporary and income that is lasting.

The Permanent Income Hypothesis, developed by the economist Milton Friedman in the 1950s, offers a deeper and more realistic explanation of consumer behavior. It suggests that individuals do not base their spending decisions only on what they earn today. Instead, they think ahead and consider their expected income over a long period of time. People are forward-looking. They try to maintain a stable standard of living by spreading their consumption evenly over time, even if their income fluctuates in the short run.

This idea has important implications for understanding economic stability, the effectiveness of government policies, and the way households respond to uncertainty.

The Core Idea: A Formal Definition

At the heart of the Permanent Income Hypothesis is a simple but powerful idea. People base their consumption on their expected long-term income, which Friedman called their permanent income.

But what does "permanent income" actually mean? Friedman defined it as the present value of all expected future income flows. In plain language, permanent income is the amount a household could consume each year while keeping its total wealth constant over time.

Think of it this way. If you add up everything you expect to earn over your entire career, plus any savings or inheritance you already have, and divide that total by the number of years you expect to live, you get your permanent income. It is your sustainable spending power.

This is different from current income, which may vary from month to month or year to year. A medical resident earns very little today but expects to earn a great deal in the future. Their permanent income is much higher than their current income. A factory worker on overtime earns more this month but knows the extra hours will not last. Their permanent income is much lower than their current monthly earnings.

Understanding this distinction is the key to understanding the entire theory.

There is also a deeper reason why individuals prefer to base consumption on permanent income rather than current income. In economics, it is generally assumed that people derive satisfaction from consumption, but each additional unit of consumption adds less satisfaction than the previous one. This means that a very uneven pattern of consumption—spending a great deal in one period and very little in another—reduces overall well-being. As a result, individuals have a natural incentive to spread consumption more evenly over time.

A Real-Life Story: Diane the Assembly Line Worker

To see how this works in practice, consider a woman named Diane. She works on an assembly line at a factory that manufactures washing machines. Her regular take-home pay is £2,200 per month. Her permanent income is also about £2,200 per month, because she expects this level of earnings to continue for the foreseeable future.

One month, the factory gets a large order from a retail chain. Diane is offered overtime. She works extra shifts and earns an additional £500 that month. This is transitory income. It is temporary. She knows the overtime will end when the order is finished.

How does Diane spend the extra £500? According to the Permanent Income Hypothesis, she will spend very little of it on ongoing consumption. She might save most of it. She might use it to pay down credit card debt. She might put it toward a holiday. But she will not increase her monthly spending on rent, groceries, or utilities. She knows the extra money is temporary, so she does not commit to ongoing expenses that would be hard to reverse.

Now imagine a different scenario. Diane is promoted to shift supervisor. Her regular monthly pay rises from £2,200 to £2,400. This is a permanent increase. Her permanent income has gone up.

Now how does she behave? She will increase her regular consumption. Perhaps she upgrades her car. Perhaps she moves to a slightly nicer apartment. Perhaps she eats out more often. She knows the extra money will continue month after month, so she feels comfortable committing to higher ongoing spending.

This is the central insight of the Permanent Income Hypothesis. Temporary income changes have small effects on consumption. Permanent income changes have large effects.

How People Estimate Permanent Income

Friedman recognized that people cannot see the future. No one knows exactly what they will earn over their entire lifetime. So how do they form expectations about permanent income?

His answer was that people look at their past income and make reasonable projections. They assume that what has happened in the recent past is a good guide to what will happen in the near future. Permanent income is essentially a weighted average of past income, with more weight given to recent years.

For example, if Diane has earned around £2,200 per month for several years, she will assume that her permanent income is roughly that amount. If she receives a promotion, she will update her estimate upward. If the factory announces layoffs, she will revise it downward.

This is not a perfect process. People make mistakes. They are sometimes too optimistic or too pessimistic. But the basic idea is that permanent income is not a fixed number. It changes as people receive new information about their prospects.

It is also important to note that permanent income includes more than just wages. Wealth matters too. A household with substantial savings or investments has a higher permanent income than a household with the same salary but no assets. The money in the bank generates interest. The investments can be sold. Wealth allows people to consume more without earning more from work.

The Role of Expectations: Looking Ahead

Expectations play a central role in the Permanent Income Hypothesis. People form beliefs about their future income based on available information, past experiences, and economic conditions.

These expectations influence how much they are willing to spend today. If individuals feel optimistic about their future earnings, they are more likely to increase their current consumption. On the other hand, if they are uncertain or pessimistic about the future, they may choose to save more and spend less.

It is important to recognize that it is not actual future income that determines consumption, but expected future income. These expectations can sometimes be inaccurate. People may be overly optimistic during economic booms or overly pessimistic during downturns. As a result, consumption decisions are shaped not only by economic reality but also by perception and confidence.

Consider the late 1970s in the United Kingdom. The economy was struggling with high inflation and rising unemployment. Even workers whose pay had not yet been cut felt uneasy about the future. They began saving more and spending less, not because their current income had fallen, but because they expected harder times ahead.

This forward-looking behavior explains why consumption can change even without immediate changes in income. It also highlights the importance of confidence and expectations in shaping economic activity. When people are confident, they spend. When they are worried, they save.

Consumption Smoothing: Keeping Life Stable

One of the most important implications of the Permanent Income Hypothesis is the idea of consumption smoothing. This refers to the tendency of individuals to keep their consumption relatively stable over time, even when their income varies.

People generally prefer a stable standard of living rather than one that fluctuates dramatically. Sudden increases or decreases in consumption can be uncomfortable and difficult to manage. As a result, individuals use savings and borrowing to smooth out their consumption.

This ability to smooth consumption depends on access to financial markets. When individuals save, they can earn interest and transfer purchasing power into the future. When they borrow, they bring future income forward into the present, although usually at a cost. These mechanisms allow people to adjust their spending in response to expected long-term income rather than being tied strictly to current earnings.

Think again about the medical resident. During their training, their income is very low. But they expect to earn a high income as a doctor in the future. They may take out loans to maintain a reasonable standard of living during their residency. They are essentially borrowing against their future income.

Later in life, when their income increases, they repay those loans and save more for retirement. In this way, consumption remains relatively stable even though income changes significantly over time.

The same logic applies to someone who experiences a temporary drop in income, such as during a short period of unemployment. Rather than immediately cutting spending drastically, they might rely on savings or short-term borrowing, expecting their income to recover soon.

This behavior shows how individuals actively manage their finances to avoid large swings in their standard of living. It also explains why consumption is much more stable than income in economic data.

When Smoothing Breaks Down: Liquidity Constraints

However, not all households are able to borrow freely. Some individuals face what economists call liquidity constraints, meaning they cannot easily access credit or are limited in how much they can borrow.

In such cases, consumption becomes more closely tied to current income. A worker who expects higher earnings next year but cannot borrow today may still be forced to reduce current consumption. This is one of the main reasons why real-world behavior sometimes deviates from the predictions of the Permanent Income Hypothesis.

For households living paycheck to paycheck, even a temporary drop in income can force immediate cuts in spending. They cannot smooth because they have no savings to draw on and no access to affordable credit. This is an important reality that the basic PIH model does not capture but that economists have since incorporated into more advanced versions of the theory.

Related Ideas: The Life-Cycle Hypothesis

Around the same time Friedman developed the Permanent Income Hypothesis, the economist Franco Modigliani was developing a closely related theory called the Life-Cycle Hypothesis.

Both theories emphasize that people are forward-looking and that consumption smoothing is a central goal. The main difference is that Modigliani explicitly models age. He argued that people typically borrow when they are young (spending more than they earn), save when they are middle-aged (earning more than they spend), and dissave when they are retired (spending their accumulated savings).

The Permanent Income Hypothesis is more general. It focuses on expectations rather than age. But the two theories are complementary, not contradictory. Together, they provide a powerful framework for understanding how households manage their finances over time.

Why This Matters for Policy

The Permanent Income Hypothesis has important implications for economic policy, particularly for understanding how people respond to government actions.

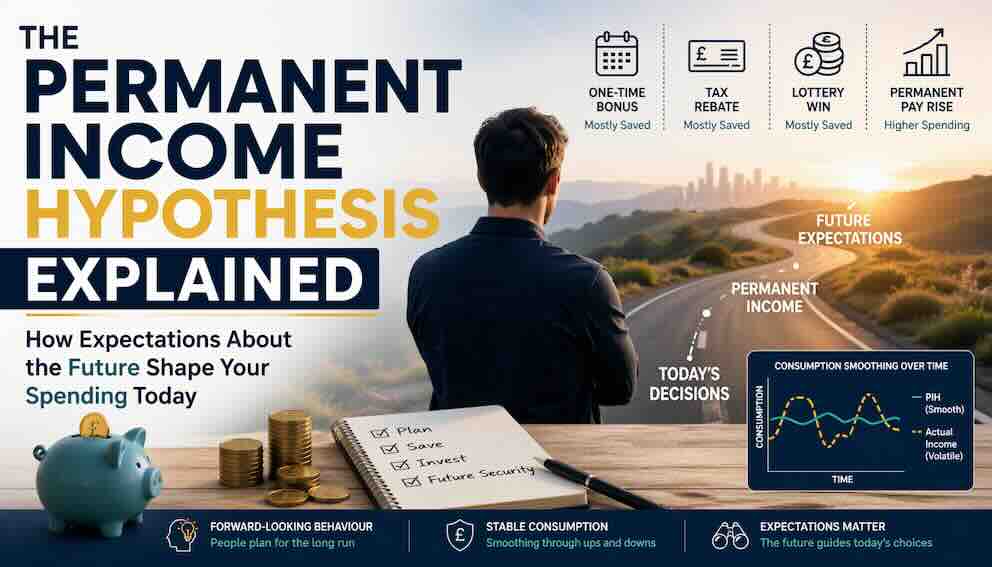

One key insight is that temporary changes in income, such as short-term tax cuts or one-time stimulus payments, may not lead to large increases in consumption. Since individuals recognize that these changes are temporary, they are more likely to save the additional income rather than spend it.

For example, if a government provides a one-time tax rebate, households may treat it as transitory income. Instead of increasing their regular spending, they might use the money to pay off debt or add to their savings.

A clear example can be seen during the COVID-19 pandemic, when governments across the world issued one-time financial support payments to households. While some of this money was spent, a significant portion was saved or used to pay down debt. This pattern is consistent with the Permanent Income Hypothesis, which predicts that temporary income increases will have a limited effect on consumption.

This does not mean that such policies have no effect, but it suggests that their impact on consumption may be limited compared to policies that affect permanent income.

On the other hand, policies that influence long-term income prospects, such as education reforms, infrastructure investment, or stable employment opportunities, can have a stronger effect on consumption. By increasing permanent income, these policies encourage individuals to adjust their spending more significantly.

Another implication is that consumption tends to be more stable than income. Even when income fluctuates due to economic cycles, consumption does not change as dramatically. This stability can help reduce the severity of economic fluctuations.

What Economists Discovered After Friedman

The Permanent Income Hypothesis was a major advance in economic thinking. But as researchers tested it against real-world data, they discovered two puzzles.

The first is called excess sensitivity. Consumption seems to respond more to predictable changes in income than the theory predicts. For example, people often spend more when they know a tax refund is coming, even though they should have already anticipated it.

The second is called excess smoothness. Consumption seems to respond less to unexpected changes in income than the theory predicts. When people receive a surprise bonus, they do not increase spending as much as the theory suggests.

These puzzles led economists to refine the theory. They introduced the idea of liquidity constraints (some people cannot borrow against future income, so they are forced to live paycheck to paycheck). They also introduced precautionary saving (people save extra when they are uncertain about the future, just to be safe).

These refinements do not reject the Permanent Income Hypothesis. They build on it. The core insight—that people look to the future when making spending decisions—remains intact.

Conclusion: A Forward-Looking View of Consumption

The Permanent Income Hypothesis provides a powerful framework for understanding how individuals make consumption decisions in a complex and uncertain world. By focusing on long-term expectations rather than short-term fluctuations, it captures the forward-looking nature of human behavior.

People do not simply react to their current income. They think carefully about their future prospects and adjust their spending accordingly. They distinguish between permanent and transitory income. They smooth their consumption over time. They respond to changes in expectations about the future. And when they cannot borrow or face uncertainty, they adapt in ways that refine but do not overturn the basic theory.

This perspective helps explain why consumption remains relatively stable even when income varies, and why certain economic policies may have limited effects. It also highlights the importance of confidence, stability, and long-term planning in shaping economic outcomes.

In a broader sense, the Permanent Income Hypothesis reminds us that economic decisions are deeply connected to expectations about the future. Understanding these expectations is essential for interpreting real-world behavior and designing effective policies. And it all begins with a simple distinction: between the money you have today and the money you expect to have tomorrow.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.