Tutorial Categories

Last Updated: May 19, 2026 at 10:30

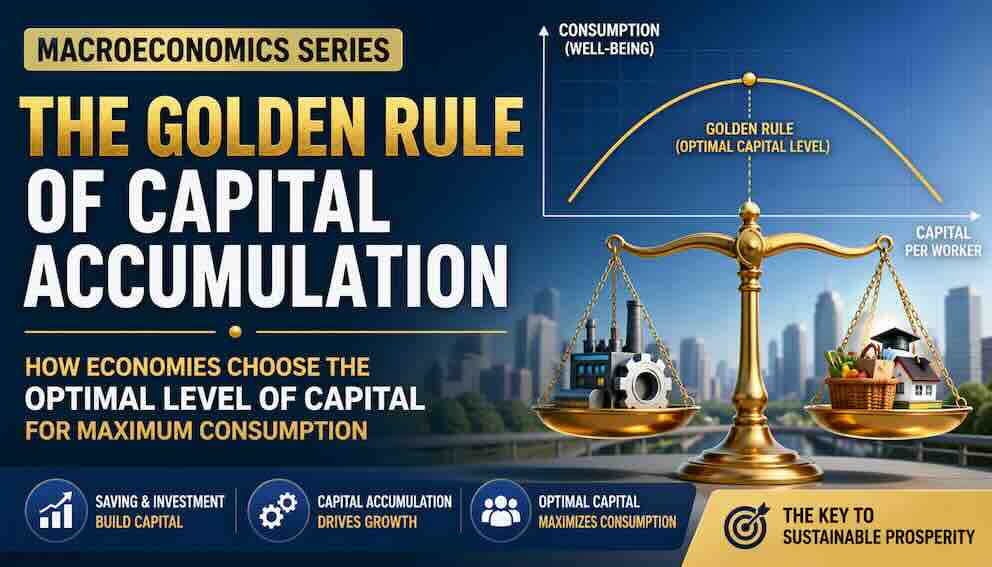

The Golden Rule of Capital Accumulation

How Much Should a Nation Save? Finding the Balance Between Today's Meals and Tomorrow's Harvest

This tutorial explores one of the most elegant and surprisingly counterintuitive ideas in macroeconomics: the Golden Rule of capital accumulation. It asks a human question: how much should an economy save so that people can enjoy the highest possible consumption over the long run? We will learn what it means for an economy to be dynamically inefficient — saving so much that every generation could be made better off by saving less. Using the real-world stories of post-war Germany, 1980s Japan, and China's recent property crisis, we will see why markets do not automatically find the right balance, and how policies like pension systems can help. By the end, you will understand a key insight: too little saving leaves people poor, but too much saving can also make a nation poorer than it needs to be.

Introduction: A Quiet Question About Flour and Bread

Imagine you are given a plot of land and a bag of wheat seeds. You can eat the seeds today as porridge, or you can plant them to grow more wheat for tomorrow. If you eat all the seeds, you feast today but starve later. If you plant every last seed, you will have a huge harvest next year — but you will be hungry today.

An economy faces the same kind of choice, only on a vast scale. Instead of wheat seeds, it has machines, roads, factories, and computers — what economists call capital. Instead of porridge, it has consumption: food, housing, healthcare, books, and holidays.

The Golden Rule of Capital Accumulation is the economist's attempt to answer: how much should we plant, and how much should we eat?

But here is a deeper twist. Even when people make their own saving decisions freely, there is no invisible hand that guarantees they will choose wisely for the long run. One generation might save too little, leaving the next generation poor. Or a generation might save too much, building a mountain of machines that cost more to maintain than they produce. The Golden Rule provides a benchmark — a north star — for judging whether a nation's saving is helping or hurting its people over time.

Capital Accumulation: The Quiet Engine of Living Standards

Let us begin with a simple truth. A worker with a bulldozer can dig more holes than a worker with a spoon. A doctor with an MRI machine can diagnose more accurately than one who only has a stethoscope. A farmer with a tractor can feed more people than one with a hand plough.

That is why countries accumulate capital. They set aside some of today's output — they save and invest — to build machines, schools, ports, and power grids. Over time, this capital makes workers more productive, and the economy grows.

But here is the subtle point: more capital is not always better for the people living in that economy. Why? Because capital is not free. To build and maintain capital, you must sacrifice consumption today. And after a certain point, adding one more machine adds so little extra output — due to diminishing returns — that it is not worth the sacrifice.

The Golden Rule identifies that precise point.

The Fishing Village

Imagine a fishing village. The villagers own fishing nets. Each net catches a certain number of fish per day. The villagers can either eat the fish (consumption) or set aside fish to trade for more nets (investment).

With one net, they catch 100 fish per day. They eat 80 and trade 20 for a second net. Now they have two nets and catch 180 fish. They eat 100 and trade 80 for more nets. With three nets they catch 240 fish, with four they catch 280, and with five they catch 300. Each additional net adds fewer fish than the last, because there are only so many fish in the nearby waters. This is diminishing returns.

Now the villagers face a choice about how many nets to own. Each net wears out over time — it needs to be mended and eventually replaced. This maintenance cost must be paid out of the fish they catch. So for every net they own, some fish must be set aside just to keep that net working. The question is no longer just "does this net catch any fish?" but "does this net catch enough fish to justify its upkeep, and are we eating as well as we possibly could?"

This is where the Golden Rule comes in. If the village owns too few nets, adding one more would bring in extra fish that far exceed its maintenance cost — meaning the villagers could eat more. If the village owns too many nets, the last net catches almost nothing, yet still demands maintenance fish that could have been eaten instead — meaning the villagers are actually eating less than they could be. The sweet spot — the point that maximises how many fish the villagers get to eat each day — is reached when the extra fish caught by the last net exactly equals the fish needed to maintain it. That is the Golden Rule: not simply the point where nets stop being profitable, but the precise capital stock that makes consumption as high as it can possibly be.

When the village reaches this sweet spot, the villagers are eating as many fish per day as they ever can, sustainably. Any additional net would not add to their meals — it would take away from them

Three Countries, Three Lessons

Instead of starting with a formula, let us walk through three real economic histories. Each one illuminates a different piece of the puzzle.

Germany After World War II: The Case of Too Little Capital

In 1945, Germany's factories were rubble. Capital per worker was extremely low. What does that mean in practical terms? It means that a single tractor could transform a field. A single welding machine could help rebuild a factory. The extra output from one more machine — what economists call the marginal product of capital — was enormous.

Germany faced a choice. It could consume what little it produced and live modestly. Or it could save and invest heavily, sacrificing present consumption for future abundance. It chose the latter. The famous Wirtschaftswunder (economic miracle) of the 1950s involved Germans consuming less than they could have, so that factories, roads, and housing could be rebuilt.

For about a decade, this was painful. But within fifteen years, Germany had accumulated enough capital that output per person had more than doubled. Consumption eventually soared far above what it would have been if they had saved less.

In this situation, the marginal product of capital was much higher than the cost of maintaining and replacing capital. Adding more capital raised long-run consumption. Economists say Germany was below the Golden Rule.

Japan in the Late 1980s: The Case of Too Much Capital (Dynamic Inefficiency)

Now consider Japan thirty years later. By the 1980s, Japan had rebuilt its capital stock to world-leading levels. Japanese companies were so productive that they could produce cars and electronics faster than almost anyone else. But here is the odd thing: Japanese households and firms kept saving at extremely high rates — around 30 to 35 percent of national income.

What happened? Japan built ports with very few ships. It built office towers that stood half-empty. It built factories that ran at 60 percent capacity. The marginal product of capital fell very low. Adding one more machine produced almost nothing extra because there were already enough machines.

Yet to maintain all this idle capital, Japan had to pour billions into repairs, maintenance, and interest payments. Consumption as a share of national income stayed lower than in other rich countries. Japanese workers had high output but relatively lower living standards in terms of leisure, housing space, and household spending.

This brings us to a powerful and counterintuitive concept: dynamic inefficiency. An economy is dynamically inefficient when it saves so much that it could make every generation — both present and future — better off by saving less. Think about how strange that is. Normally, if you save less today, you consume more today but leave less for tomorrow. That is a trade-off. But in a dynamically inefficient economy, there is no trade-off. Reducing saving increases consumption today and does not harm the future, because the future was already drowning in excess capital that cost more to maintain than it produced.

Most economists believe that Japan in the late 1980s and early 1990s was dynamically inefficient. It was above the Golden Rule. Reducing the saving rate would have increased long-run consumption.

China Today: The Difficulty of Knowing Where You Stand

China saves and invests about 45 percent of its national income — one of the highest rates in the world. For decades, this was wise. China was poor. Capital was scarce. The marginal product of capital was high. Building subways, high-speed rail, ports, and solar panel factories lifted hundreds of millions out of poverty.

But China is no longer poor. Its capital per worker now approaches that of developed countries. And there are growing signs of diminishing returns. Since 2021, China has experienced a severe property crisis, with major developers defaulting on massive debts. Across the country, there are empty apartment towers, ghost cities, and expressways with very few cars. Industrial overcapacity in steel, cement, and solar panels means factories are producing far more than can be sold profitably.

The difficult question is whether China is already above the Golden Rule — dynamically inefficient — or whether it still benefits from high investment. The answer depends on measurements that are never perfectly precise: the marginal product of capital, the rate at which capital wears out, population growth, and technological progress. This uncertainty is real. Even expert economists disagree about China.

What is clear is that if China continues to save at 45 percent when the marginal product of capital has fallen below the cost of maintaining and expanding the capital stock, then it is above the Golden Rule. That would mean Chinese citizens could actually consume more today and in the future simply by saving less. That is a very live policy debate inside China today.

The Formal Condition Emerges

Notice a pattern across these three stories.

In Germany, the marginal product of capital was very high — much higher than the rate at which machines wore out (depreciation) plus the rate at which the population was growing plus the rate of technological progress. So Germany was below the Golden Rule. It made sense to invest more.

In Japan, the marginal product of capital fell very low — below depreciation plus population growth plus technological progress. So Japan was above the Golden Rule. It had accumulated too much capital.

The Golden Rule condition can therefore be written as a simple equality:

Marginal Product of Capital = Depreciation rate + Population growth rate + Technological progress rate

Let us unpack each term slowly.

- Marginal Product of Capital (MPK): The extra output produced by adding one more unit of capital, holding everything else constant. A new machine, one more factory, an additional mile of road.

- Depreciation rate (δ): The rate at which capital wears out, breaks, or becomes obsolete. Machines rust. Buildings age. Computers become outdated. In rich countries, depreciation is typically about 5 to 10 percent per year.

- Population growth rate (n): If the population is growing, you need more capital just to keep capital per person constant. A growing population dilutes the capital stock unless you invest enough to keep up.

- Technological progress rate (g): Better technology makes old capital obsolete faster. A factory built for horse-drawn carriages is useless once cars are invented. Technological progress raises the effective cost of maintaining capital. g will be explored more fully in the next tutorial.

When MPK is greater than δ + n + g, the economy is below the Golden Rule. Adding capital raises long-run consumption. When MPK is less than δ + n + g, the economy is above the Golden Rule (dynamically inefficient). Reducing capital (by saving less) raises long-run consumption.

When MPK equals δ + n + g, the economy is at the Golden Rule. Consumption is as high as it can sustainably be.

Why Markets Do Not Automatically Find the Golden Rule

You might wonder: if the Golden Rule is such a good idea, why don't markets just get there on their own? This is where the overlapping generations model becomes important.

In the real world, people live for about 60 to 80 years. They work, save during their working lives, and then consume those savings in retirement. Each generation makes its own saving decisions. But those decisions affect future generations — and future generations have no say in them.

There is no market transaction between the unborn and the living. A young person saving for retirement does not consider whether their saving might accidentally push the economy above the Golden Rule, leaving their own children with too much capital. There is no price signal that says "stop saving, you are making future generations worse off."

This is why the Golden Rule is a policy benchmark rather than a market outcome. In a decentralized market economy, there is no automatic mechanism that steers the capital stock toward the Golden Rule. It can systematically overshoot (like Japan) or undershoot (like many poor countries). Governments may need to use policies — such as tax incentives, pension system design, or public investment — to guide the economy closer to the optimal level.

A Real-World Policy Application: Social Security and Pensions

This is not an abstract theoretical curiosity. The design of pension systems directly affects whether an economy is near the Golden Rule.

Consider a pay-as-you-go pension system. The working generation pays taxes that are immediately transferred to retirees. This system reduces national saving because workers do not need to save as much for their own retirement. In a dynamically inefficient economy — one that is above the Golden Rule — reducing saving is actually beneficial. A pay-as-you-go system can push the economy back toward the Golden Rule, increasing consumption for both the old (who receive benefits) and the young (who no longer need to save excessively).

Conversely, a fully funded pension system (like a national 401(k)) forces people to save more. If the economy is already above the Golden Rule, this makes the dynamic inefficiency worse. If the economy is below the Golden Rule, it helps.

This is why debates about pension reform are not just about fairness or fiscal sustainability. They are also about whether a country is saving too much or too little relative to the Golden Rule. Japan, with its aging population and history of high saving, might benefit from more pay-as-you-go financing. A poor country with low saving might benefit from more funded pensions.

The Asymmetry of Transition

One of the most important practical facts about the Golden Rule is that moving toward it is not symmetric.

If an economy starts below the Golden Rule (like Germany in 1950), increasing the saving rate requires a period of lower consumption today. People must sacrifice now so that investment can rise and capital can grow. This is politically difficult. Voters dislike being asked to consume less. That is why many poor democracies under-invest relative to the Golden Rule.

If an economy starts above the Golden Rule (like Japan in 1990), lowering the saving rate can actually increase consumption immediately — because you simply stop building so much new capital and let people spend more of what they produce. There is no sacrifice period. In theory, the transition is painless or even beneficial from day one.

So why don't countries above the Golden Rule just reduce saving overnight? Because in practice, reducing saving means reducing investment. That can cause a sharp drop in aggregate demand, leading to recession and unemployment. Japan tried to reduce its excessive saving in the 1990s but found that doing so triggered a banking crisis and a lost decade of growth. The transition to the Golden Rule, even from above, is not always smooth in the real world. This is another reason why the Golden Rule remains a benchmark rather than a simple policy lever.

What the Golden Rule Does Not Say

It is worth being clear about the limits of this framework.

The Golden Rule does not say an economy should never be above or below it. Sometimes temporary deviations make sense — for instance, after a war when capital is destroyed, investing heavily even beyond the Golden Rule might be justified for a time.

The Golden Rule says nothing about distribution. An economy could be at the Golden Rule level of capital, but if all the consumption goes to a tiny elite, ordinary people will not feel prosperous. The Golden Rule is about total consumption, not its fairness.

The Golden Rule also says nothing about environmental sustainability in its standard form. An economy could maximize consumption by burning forests, depleting fisheries, and exhausting mineral resources. But those actions are not sustainable — they reduce the capital available to future generations. Many ecological economists argue that the Golden Rule should incorporate natural capital (forests, fisheries, clean air, stable climate) alongside physical capital. In that expanded framework, the condition becomes: invest in renewable natural capital at least as fast as you deplete it. Otherwise, you are not truly maximizing sustainable consumption. This is a more advanced extension, but it shows how the Golden Rule logic can be adapted to environmental concerns.

Conclusion: A Rule for Human Flourishing, Not Just Growth

The Golden Rule of Capital Accumulation is a quiet corrective to the idea that more growth is always better. It asks a deeper question: growth for what? The answer, in economics, is consumption — the actual goods and services that people use to live, learn, play, and rest.

Too little capital leaves a society poor and vulnerable. Too much capital — dynamic inefficiency — leaves a society rich in machines but poor in comfort, leisure, and home life. Somewhere in between lies a balance: enough investment to keep the economy productive, but not so much that people sacrifice their living standards for the sake of idle steel.

The fact that markets do not automatically find this balance is not a failure of markets per se. It is a feature of an economy where each generation makes decisions that affect generations who cannot bargain with them. That is why the Golden Rule exists as a benchmark for wise policy — whether through pension system design, tax policy, or public investment decisions.

When you hear a politician say "we must save more for the future," you can now ask: are we below the Golden Rule? And when you hear "we cannot afford more consumption," you can ask: are we perhaps above it, in a state of dynamic inefficiency? These are not technical questions only for economists. They are human questions about how we choose to live between today and tomorrow.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.