Tutorial Categories

Last Updated: May 19, 2026 at 10:30

The Ramsey-Cass-Koopmans Model Explained: How Patient Households Choose Between Today's Consumption and Tomorrow's Growth

Moving Beyond Fixed Savings Rates — Understanding How Forward-Looking Families Decide the Fate of Entire Economies

The Solow model assumed that households save a fixed fraction of their income, but it never explained where that fraction comes from. The Golden Rule told us what the optimal savings rate should be, but it offered no mechanism for getting there. The Ramsey-Cass-Koopmans model closes this gap by placing optimising households at the centre of the story — households that look forward, weigh the pleasure of consumption today against the security of consumption tomorrow, and make deliberate choices about how much to save. This tutorial walks through the logic of intertemporal choice, the Euler equation that describes how consumption grows over time, the modified Golden Rule that incorporates household impatience, and the saddle path that guides the economy to its long-run destination. You will also learn why patient societies build more capital, why the model has important things to say about climate policy and government debt, and where its assumptions require honest qualification.

Introduction: The Unanswered Question from Solow and the Golden Rule

Let us go back to the Solow model for a moment. In that framework, the engine of capital accumulation was a fixed savings rate. Households were assumed to save a constant fraction of their income, and the model did not ask why they saved that particular fraction. It did not explore whether they might save more when interest rates rose or save less when the future felt uncertain. The savings rate simply fell from the sky, as if by decree.

The Golden Rule then asked a different and more interesting question: given the technology and the population growth of an economy, what savings rate would maximise long-run consumption? That was a genuine advance. It gave us a benchmark for judging whether a country was saving too much or too little. But the Golden Rule still did not explain how an economy actually arrives at its savings rate. It described a destination without explaining the journey, or whether any economy would naturally find its way there.

The Ramsey-Cass-Koopmans model, named after the economist Frank Ramsey who first conceived the core idea and later economists David Cass and Tjalling Koopmans who refined it into its modern form, solves this problem. Ramsey was originally motivated by a normative question: what is the optimal level of saving for a society that cares about both present and future generations? He derived the optimal savings rate from first principles rather than assuming it as a fixed parameter. Cass and Koopmans later transformed this into a positive model describing how actual optimising households behave. This tutorial focuses on that positive framework.

The central idea is straightforward. When you decide whether to spend your paycheck on a holiday or put it into a savings account, you are making what economists call an intertemporal choice. You are weighing the pleasure of spending today against the security of having more tomorrow. The Ramsey-Cass-Koopmans model takes that same logic, scales it up to the entire economy, and asks what happens when every household is thinking this way and when firms compete to borrow their savings for investment. The answer is a richer and more realistic picture of growth, where the patience and forward-looking behaviour of households shapes the long-run destiny of entire nations.

The Setup — Households That Think About the Future

To build this model, we need to imagine a particular kind of household. This household does not live for just one year or even one lifetime. In the model, it lives indefinitely, or equivalently it cares about the well-being of all future generations as if they were its own children and grandchildren. This is admittedly a strong assumption, and we will return to its limitations. But it is a useful starting point because it allows the household to think about the very long run without the complications that arise from retirement, inheritance, and uncertain lifespans.

The household derives satisfaction — economists call it utility — from consuming goods and services. A good meal produces utility. A comfortable home produces utility. A holiday produces utility. But the household does not value consumption in the distant future as much as it values consumption today. There is a simple reason for this that most people will recognise from their own experience: people are impatient. Most of us, if offered one hundred pounds today or one hundred pounds in a year, would take the money now. We prefer not to wait.

In the model, this impatience is captured by a single parameter called the discount rate, denoted by the Greek letter ρ (rho). The discount rate measures how much the household's valuation of future consumption is reduced simply because it lies in the future. A high discount rate means the household is strongly impatient — it values consumption today much more than consumption tomorrow. A low discount rate means the household is patient — it regards future consumption as nearly as valuable as present consumption.

To make this concrete, think of two families. The first family has a high discount rate. They live for the moment. They spend generously, save little, and are reluctant to defer enjoyment. The second family has a low discount rate. They are patient. They save consistently, invest carefully, and are comfortable sacrificing some comfort today for a more secure tomorrow. The Ramsey-Cass-Koopmans model tells us that these two families, if they represent entire economies, will end up in very different places. The patient economy will accumulate more capital over time and enjoy higher consumption in the long run.

The household's preferences are also described by a utility function, which captures how satisfaction changes as consumption rises. The feature of the utility function that matters most for our purposes is called the elasticity of intertemporal substitution, denoted by θ (theta). This parameter measures how willing the household is to shift consumption from one period to another in response to changes in the return on saving. A low θ means the household is very willing to defer consumption when returns are high — a small increase in the interest rate produces a large increase in saving. A high θ means the household strongly prefers to keep its consumption stable over time, even when the return to saving is attractive.

The parameter θ also plays a deeper mathematical role. In the standard utility function used in this model, θ governs the curvature of utility — how quickly the satisfaction from an additional unit of consumption diminishes as consumption rises. This curvature is what makes the household willing to trade off present against future consumption in a well-behaved way, and it is why θ appears in the Euler equation that we are about to examine.

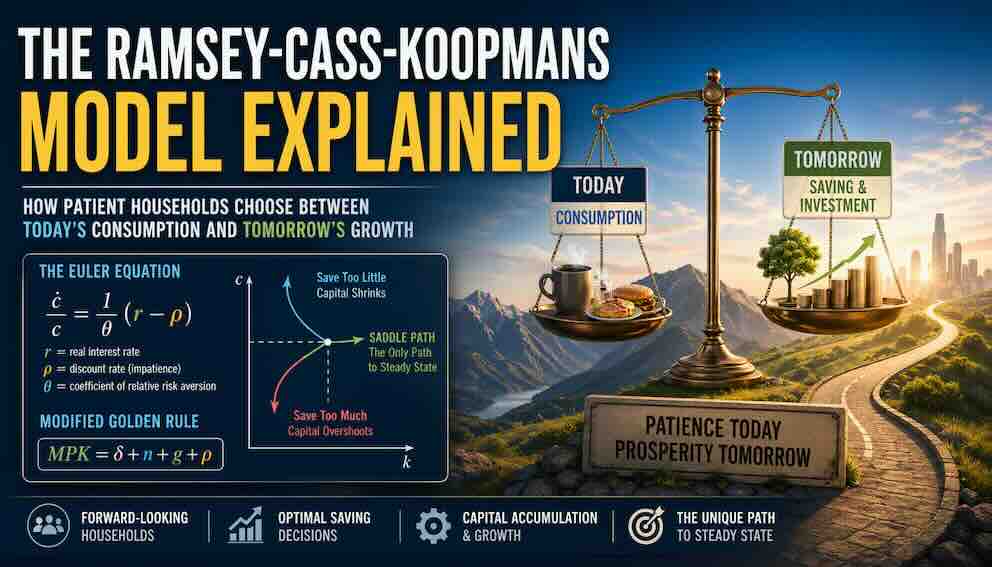

The Euler Equation — The Heart of the Model

The Euler equation is the central result of the Ramsey-Cass-Koopmans model. It describes how consumption grows over time along the optimal path. Understanding it is the key to understanding everything else the model tells us.

In its simplest form, for an economy without population growth or technological progress, the Euler equation says:

Growth rate of consumption = (r − ρ) / θ

Here r is the real interest rate that households earn on their savings, ρ is the discount rate measuring impatience and θ is the elasticity of intertemporal substitution.

Let us unpack each part of this carefully.

The interest rate r is the reward for waiting. If you save one hundred pounds today at an interest rate of five percent, you will have one hundred and five pounds next year. The higher the interest rate, the greater the reward for deferring consumption.

The discount rate ρ is the cost of waiting. Even if the interest rate offers a good return, an impatient household still finds waiting unpleasant. The discount rate quantifies that reluctance. If ρ is two percent, the household values consumption next year about two percent less than consumption today, simply because of impatience.

When the interest rate exceeds the discount rate, the reward for waiting is greater than its cost. The household finds it worthwhile to save more now and consume more in the future. Consumption will therefore grow over time. When the discount rate exceeds the interest rate, waiting is not worth it. The household prefers to consume now rather than save for a modest return. Consumption will fall over time as capital is drawn down. When the two are equal, consumption is constant — the household has no reason to shift its spending pattern in either direction.

The elasticity θ in the denominator determines how sensitive the growth rate of consumption is to the gap between r and ρ. If θ is small, households respond strongly to any imbalance between the interest rate and the discount rate, producing large swings in consumption growth. If θ is large, households are resistant to changing their consumption pattern even when the gap between r and ρ is substantial, and consumption growth responds only weakly.

This equation — sometimes called the consumption Euler equation or the Ramsey rule — is one of the most important results in dynamic macroeconomics. It tells us that the entire path of consumption over time is governed by a simple comparison between what the market offers and what the household prefers. This is a profound simplification of what might seem like an impossibly complex problem. Every household, in every period, is effectively solving the same equation.

A closely related idea in economics is Milton Friedman's permanent income hypothesis, which argued that households base their consumption not on their income this year but on their expected average income over their entire lives. The Euler equation formalises and extends this intuition. Households smooth their consumption over time, adjusting their saving whenever the return to waiting rises or falls.

The real interest rate r in the Euler equation deserves one further clarification. In the full model with capital depreciation, r is the net return to capital — the marginal product of capital minus the depreciation rate. When the capital stock is low, the marginal product of capital is high (a single new machine in a factory with very few machines adds a great deal to output), so the interest rate is high and households are induced to save and let consumption grow. As capital accumulates and diminishing returns set in, the marginal product falls, the interest rate falls, and consumption growth slows. This is the mechanism that connects the household's saving decision to the productive capacity of the economy.

Firms, Capital Markets, and How the Two Sides Connect

We have described how households respond to the interest rate. But the interest rate is not handed down from above — it is determined within the model by the interaction between households who supply savings and firms that demand capital for investment.

Firms in the Ramsey-Cass-Koopmans economy are straightforward. They rent capital from households and hire labour, combining them to produce output using a production function of the kind we encountered in the Solow model. In competitive capital markets, the interest rate that households earn equals the marginal product of capital minus the depreciation rate. This is the net return that households receive after accounting for the wear and tear on capital each year.

The crucial step that closes the model is capital market clearing: in equilibrium, household saving equals firm investment. Every pound that households choose not to consume is channelled through financial markets to firms that use it to build new capital. The interest rate adjusts until the amount households want to save exactly matches the amount firms want to invest. This market-clearing condition ties the household's consumption decision to the economy's capital accumulation in a single, coherent system.

When the capital stock is low and the marginal product of capital is high, the interest rate is high. The Euler equation then tells us that consumption growth is high, which means households are saving a large fraction of their income. That saving flows to firms, which invest it in new capital. As capital accumulates, the marginal product falls, the interest rate falls, and household saving gradually declines. The economy approaches its steady state from the demand side and the supply side simultaneously.

The Steady State and the Modified Golden Rule

The steady state in the Ramsey-Cass-Koopmans model is the point where the economy settles in the long run. At the steady state, consumption per person and capital per person are both constant. To find the steady state, we set the growth rate of consumption to zero in the Euler equation. This means r = ρ, which means the net interest rate equals the discount rate. Since the net interest rate equals the marginal product of capital minus the depreciation rate, we can write:

MPK = δ + ρ

When we extend the model to include population growth at rate n and technological progress at rate g, the steady state condition becomes:

MPK = δ + n + g + ρ

This is called the modified Golden Rule, and it is worth comparing carefully to the pure Golden Rule from an earlier tutorial. The pure Golden Rule set ρ equal to zero. It asked what savings rate would maximise steady-state consumption if the future were valued just as highly as the present. The modified Golden Rule acknowledges that real households discount the future — they are impatient by nature — and incorporates that impatience into the steady state condition.

The discount rate ρ appears on the right-hand side of the equation. To satisfy the condition with a higher ρ, the marginal product of capital must be higher. The marginal product of capital is higher only when the capital stock is lower, because of diminishing returns. So a more impatient society converges to a lower steady state capital stock and lower steady state consumption per person. A more patient society, with a lower ρ, converges to a higher capital stock and higher consumption.

This has a direct connection to the pure Golden Rule. The pure Golden Rule capital stock is the level that maximises long-run consumption when impatience is ignored. The Ramsey-Cass-Koopmans steady state capital stock is always below the pure Golden Rule level whenever ρ is positive — that is, whenever households discount the future at all. Patient societies come closer to the Golden Rule ideal. Impatient ones fall further below it.

There is also an important implication for dynamic inefficiency, a concept introduced in the Golden Rule tutorial. Dynamic inefficiency occurs when an economy saves so much that every generation could be made better off by saving less. Within the Ramsey-Cass-Koopmans framework, this cannot happen under the model's core assumptions, provided that the equilibrium interest rate exceeds the economy's growth rate — that is, provided r > n + g. When this condition holds, optimising households would never choose to accumulate capital beyond the Golden Rule level, because they would prefer to consume more today rather than leave capital that exceeds the optimal amount. However, this result depends specifically on the infinite-horizon assumption. In the overlapping generations model, where households have finite lives and different generations cannot bargain with each other, dynamic inefficiency can persist even with fully optimising households. That model offers a genuinely different perspective on intertemporal choice and deserves attention in its own right.

The Saddle Path — How the Economy Finds Its Way

We now know where the economy is headed: the steady state where the marginal product of capital equals δ + n + g + ρ. The remaining question is how it gets there. The answer involves one of the most distinctive features of the Ramsey-Cass-Koopmans model: the saddle path.

To understand the saddle path, it helps to notice an important asymmetry between two variables in the model. Capital is what economists call a state variable. It is built up gradually through investment over time and cannot jump suddenly from one level to another. The capital stock today was determined by decisions made in the past, and it can only change slowly as investment accumulates. Consumption, by contrast, is a choice variable. Households can choose their consumption level at any moment. If circumstances change, consumption can adjust immediately.

This asymmetry creates the following problem. Given the current capital stock — which is fixed by history — households must choose how much to consume today. If they consume too much, saving will be too low, investment will be insufficient, and the capital stock will not grow toward the steady state. If households consistently consume too much, the capital stock will eventually be exhausted and the economy will collapse. If households consume too little, the capital stock will grow beyond the steady state level, accumulating more capital than is optimal and leaving households with less consumption than they could have enjoyed.

There is exactly one initial level of consumption that places the economy on a path arriving precisely at the steady state — not collapsing and not overshooting indefinitely. That path is the saddle path. Once the economy is on the saddle path, it follows it smoothly toward the steady state without any further correction.

The saddle path is mathematically unstable in the sense that paths slightly above or below it diverge away from the steady state rather than converging toward it. This might seem to make finding the right path nearly impossible. The reason optimising households do find it is that they solve a forward-looking problem. They can see the consequences of choosing a consumption level that is too high or too low. Knowing that excessive consumption leads to eventual collapse, and knowing that insufficient consumption leads to wasteful over-accumulation, they choose the unique level that puts them on the saddle path. This forward-looking calculation is the formal content of the transversality condition.

The transversality condition is the mathematical statement that completes the household's optimisation problem alongside the Euler equation. In plain language, it says that the household should not accumulate capital indefinitely without ever consuming it. At the limit, as time extends toward infinity, the present value of the capital stock must approach zero — meaning the household must eventually consume all its wealth rather than leaving it idle forever. This rules out paths that overshoot the steady state and accumulate ever-growing capital stocks that are never drawn down. Combined with the Euler equation, the transversality condition uniquely selects the saddle path.

A practical analogy may help. Imagine landing an aircraft on a runway. The approach must begin from exactly the right altitude and at exactly the right rate of descent. Too steep and the aircraft hits the ground too early. Too shallow and it overshoots the runway. There is one correct approach path, and the pilot must commit to it from a considerable distance away. The saddle path is that approach for an economy. Forward-looking households, like an experienced pilot, compute it in advance and commit to the right starting point.

Real-World Grounding

The Ramsey-Cass-Koopmans model is abstract, but it connects to real economic behaviour in several concrete and important ways.

Consider consumption smoothing during recessions. The model predicts that forward-looking households should maintain their consumption as stable as possible, drawing on savings when income falls temporarily rather than cutting back sharply. This pattern is visible in the data. During the 2008 financial crisis, United States GDP fell by roughly four percent, but personal consumption expenditures fell by only about one and a half percent. Households used their savings and access to credit to keep their living standards more stable than their incomes. During the Covid-19 pandemic in 2020, the pattern went even further in the opposite direction: the United States personal saving rate spiked above thirty percent as households, unable to spend normally and uncertain about the future, accumulated savings at a historically unusual rate. This precautionary response — saving more when the future feels uncertain — is not fully captured by the basic Ramsey-Cass-Koopmans model, which assumes households face a certain future. But it is a natural extension of the same framework, where uncertainty about future income gives households an additional reason to save beyond what the Euler equation alone would predict.

Consider the cross-country differences in saving rates. Japan, South Korea, and China have historically saved at considerably higher rates than the United States or the United Kingdom. The Ramsey-Cass-Koopmans model offers a precise way to think about this: different discount rates lead to different steady states. Societies that value the future more highly, whether because of cultural norms, demographic structures, or institutional incentives for long-term saving, will accumulate more capital and converge to higher steady-state living standards. This is not a complete explanation, but it gives a coherent framework for discussing why patient economies end up richer.

Consider the response of household saving to interest rates. The Euler equation predicts that higher interest rates should induce households to save more, because the reward for waiting is greater. The empirical evidence on this is genuinely mixed. Some studies find meaningful responses, particularly in economies with well-developed financial markets where households can adjust their saving easily. Others find the effect is small, especially for middle-income households who already have stable consumption patterns and face borrowing constraints. This mixed evidence is one of the main reasons why economists continue to debate the appropriate value of the elasticity of intertemporal substitution θ, and why the basic model must be extended to account for credit constraints and household heterogeneity before it can match the data closely.

The model also has important implications for government policy through a result known as Ricardian equivalence. In an economy populated by infinite-horizon households of the Ramsey-Cass-Koopmans type, government borrowing does not affect real economic outcomes. Here is why. When the government cuts taxes today and borrows to cover its spending, households receive higher after-tax income now. But they also know that future taxes must rise to repay the debt. Because they care about all future generations as if they were their own, they save the entire tax cut today to pay the higher taxes tomorrow. Government debt therefore has no effect on consumption, investment, or the real interest rate. This is a strong and controversial prediction. In practice, many households do not behave this way — they are credit-constrained, they have finite lives, or they do not fully anticipate future tax increases. But Ricardian equivalence serves as an important benchmark, and debates about whether fiscal stimulus works or whether government deficits crowd out private investment are, at their core, debates about how far real households deviate from the Ramsey-Cass-Koopmans ideal.

The discount rate also sits at the centre of one of the most consequential policy debates of our time: how to value the well-being of future generations in climate change policy. The economist Nicholas Stern, in his influential 2006 review of the economics of climate change, argued for a discount rate close to zero on ethical grounds — future generations matter as much as the present, so their welfare should be discounted very little if at all. The economist William Nordhaus, whose work on climate economics earned him a Nobel Prize, argued for a higher discount rate based on what households actually reveal about their preferences through market behaviour. The disagreement is not only about ρ but also about θ: a higher θ implies that future generations, who will likely be richer than us, should receive less weight in current decisions because the marginal value of an additional pound of consumption is lower for a richer person. The Ramsey-Cass-Koopmans framework provides the formal structure for this entire debate, even though the question of what discount rate society should use is ultimately normative rather than purely economic.

Honest Limitations

The Ramsey-Cass-Koopmans model is powerful, but its assumptions deserve scrutiny.

The representative household assumption is one of the strongest. Every real economy contains rich households and poor ones, young households and old ones, patient savers and impatient spenders. Their behaviour differs substantially. The rich save a higher fraction of their income than the poor. The young save for retirement. The retired draw down their savings. Aggregating all of this into a single representative household smooths over differences that matter greatly for distributional questions and for understanding how fiscal policy affects different groups.

The assumption of infinite horizons is similarly idealised. Real households have finite lives. They retire, age, and eventually die. Their children may not behave as if they were simply an extension of their parents' preferences. The overlapping generations model, in which each generation lives for a finite period and interacts with other generations in markets, generates different predictions about dynamic efficiency and the effects of government debt precisely because it relaxes this assumption.

The assumption of perfect foresight — that households can compute the saddle path and commit to it — is demanding. In reality, households face genuine uncertainty about future interest rates, future incomes, and future policy. The model can be extended to incorporate uncertainty, and the precautionary saving motive emerges naturally from such extensions. But the basic model abstracts from all of this.

Despite these limitations, the Ramsey-Cass-Koopmans model remains the foundation of modern dynamic macroeconomics. It is used to analyse fiscal policy, monetary policy, climate change economics, and the long-run consequences of structural reforms. Its power comes from its clarity: it starts from a simple and honest premise about household behaviour and derives the economy's entire trajectory from that starting point.

Conclusion: The Patience of Nations

The Ramsey-Cass-Koopmans model answers the question that the Solow model left open and the Golden Rule could not resolve. The savings rate emerges from the choices of forward-looking households who weigh the pleasure of consumption today against the security of consumption tomorrow. Those choices are shaped by the real interest rate, which reflects the productivity of capital, and by the discount rate, which reflects how patiently or impatiently the society regards its future.

The Euler equation captures this in a single relationship: consumption grows when the return to saving exceeds the household's impatience, and is stable when the two are equal. The modified Golden Rule tells us where the economy ultimately settles, incorporating the discount rate alongside depreciation, population growth, and technological progress. The saddle path, selected by the transversality condition, describes the unique route the economy follows to reach that destination. And the model's extensions — to precautionary saving, to Ricardian equivalence, to the climate discount rate debate — show how far the same framework can reach when applied carefully to real policy questions.

Yet the model leaves one great question unanswered. Technological progress, the ultimate source of sustained growth in living standards, remains exogenous. It still falls from the sky, just as it did in Solow. The Ramsey-Cass-Koopmans model tells us how patient households allocate consumption over time given the technology available to them. It does not explain where better technology comes from or why some societies generate it faster than others. That question belongs to the next tutorial in this series, on endogenous growth theory, where we will explore the economics of innovation, research and development, and the deliberate creation of knowledge. The patient households of the Ramsey-Cass-Koopmans model are waiting for an answer.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.