Tutorial Categories

Last Updated: February 26, 2026 at 10:30

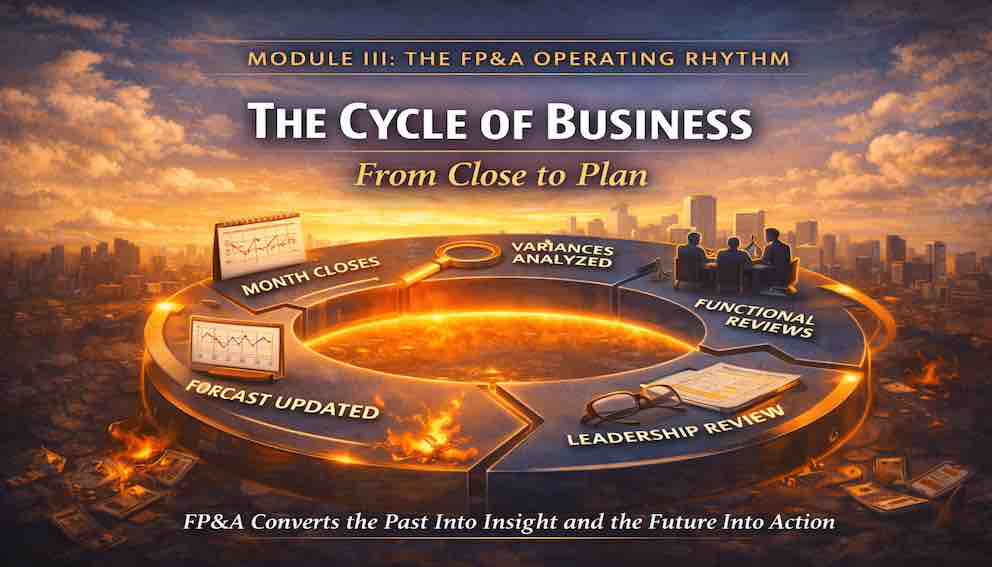

The Cycle of Business: From Close to Plan – Mastering FP&A Insights and Monthly Forecasting

The monthly financial close is far more than an administrative task—it is the heartbeat of financial planning and analysis. In this tutorial, we explore how each close generates valuable insight through flux and variance analysis, drives meaningful conversations with department leaders, and directly informs the company’s forecast and planning. By understanding the rhythm of the close, financial managers can transform routine reporting into a continuous engine of learning, decision-making, and operational improvement. Through practical examples and a real-world narrative, we show how mastering the cycle from close to plan equips finance professionals to guide their businesses with clarity, agility, and strategic foresight.

Understanding the Close as the Heartbeat of Financial Management

It is the second week of the month, and Sarah(the Financial Planning & Analysis Lead) is exhausted.

The last seven days have been consumed by the monthly close: late nights reconciling accounts, early mornings investigating variances, and countless emails with department heads about unexplained numbers. Her team is weary, and she is too.

Yet, as she sips her morning coffee and reviews the close package one final time before presenting to the leadership team, she smiles. She knows something that many outside finance never understand: the close is not just a chore—it is a diagnosis.

In most organizations, the monthly financial close is viewed as a necessary burden. Books must close, numbers must be accurate, and reports must be filed. While compliance is important, it represents the minimum. The true value of the close lies far beyond deadlines and filings.

Just as a physician monitors a patient’s pulse to understand overall health, Sarah observes the flow of transactions, reconciliations, and variances to understand the operational health of her company. Each month, the close reveals patterns: shifts in customer payments, changes in department costs, product line margin swings, and subtle stretches in working capital.

The close generates intelligence. Intelligence becomes insight, and insight—shared with the right people at the right time—becomes action. This is the cycle Sarah has mastered. Not just closing the books, but using the close to fuel strategic decisions across the business.

Two Approaches to Running the Close

Sarah recalls her early career. At her first company, the close was mechanical:

- Accuracy was ensured.

- Reports were submitted on time.

- Learning was minimal.

Variances were noted but rarely investigated. Department heads received reports, but no discussions occurred. Forecasts were updated only quarterly, disconnected from monthly realities. The close was a finish line, not a starting point.

That company struggled. Decisions were delayed. Problems were detected late. Opportunities were missed.

Now, Sarah runs the close differently. Accuracy and timeliness remain essential, but they are the foundation, not the purpose. The purpose is understanding. She tells new team members on day one:

“There are two ways to run a close. The first way produces numbers. The second way produces insight. We do the second way.”

The Mechanics of the Close: Step by Step

To turn a routine close into insight, it helps to understand the mechanics. Sarah walks her new analyst through each stage.

1. Recording Transactions and Reconciling Accounts

The first step is ensuring all transactions are recorded accurately. This includes:

- Sales and purchases

- Payroll and benefits

- Depreciation and amortization

- Accruals and prepayments

Every account in the general ledger must reconcile to reality. Accounts receivable should match customer invoices. Inventory should align with physical stock counts. Prepaid expenses must be properly amortized.

“This is where we verify that the raw data is reliable,” Sarah explains. “If the foundation is wrong, everything built on top is wrong.”

2. Generating Preliminary Reports

Once accounts are reconciled, preliminary reports are prepared: the income statement, balance sheet, and cash flow statement.

These reports provide the first opportunity to spot variances between actual and expected results. For instance, an unexpected rise in the cost of goods sold might hint at operational inefficiencies or supplier price increases. At this stage, the focus is observation, not explanation.

“We see the numbers first. Then we ask why.”

3. Performing Variance Analysis

Variance analysis compares actual results to budgets, forecasts, and prior periods.

Yet this is not a purely numerical exercise. Understanding the business is essential. A spike in marketing expenses might reflect a planned campaign executed earlier than anticipated—a timing issue rather than a structural change. Conversely, if the spike results from permanently higher media rates, the forecast must be updated.

“Variance analysis tells us what changed,” Sarah says. “But it doesn’t tell us why. For that, we need flux analysis.”

Flux Analysis: Understanding the Why Behind the Numbers

Flux analysis takes variance analysis deeper, examining the reasons behind every movement.

For example, suppose total revenue increased 10% over the previous month. A simple variance report stops there. Flux analysis asks: why?

- 6% came from higher sales volume in one region

- 3% from a price increase in another

- 1% from a change in product mix with higher-margin products selling better

This level of detail allows management to understand not just that revenue improved, but why.

Flux analysis also uncovers hidden risks. Revenue might increase, but if margins shrink due to higher discounting, leadership could be misled by headline numbers.

“Sometimes the most important insight is what the headline numbers don’t show,” Sarah emphasizes.

Turning Insight into Action: Conversations with Department Heads

The true power of the close emerges in discussions with department heads. Data alone is insufficient. Insight emerges when numbers are interpreted in collaboration with those who have operational knowledge.

Sarah meets with operations to review cost variances: Was overtime higher due to inefficiency or a one-off rush order? Supplier price increases: temporary or permanent?

She meets with sales: Which deals slipped? Which exceeded expectations? Patterns in discounting or deal velocity?

With marketing: Are customer acquisition costs rising? Which channels perform best? Are there timing mismatches between spend and results?

“These conversations are where numbers become knowledge,” Sarah tells her team. “The data tells us what happened. The department heads tell us why. Together, we figure out what to do about it.”

From Close to Forecast: Using Insights to Guide the Business

Insights from the close feed directly into forecasting. Unlike many companies that update forecasts quarterly, Sarah’s team refreshes them monthly.

- If sales in a key market fall short due to rising competition, projections and cash flow models are updated.

- If cost savings are identified, resources can be reallocated to strategic initiatives.

- If working capital stretches, adjustments in cash management and financing are made.

The close is a feedback loop. It informs the forecast, which informs decisions, which informs the next close.

“The close feeds the forecast,” Sarah explains. “And the forecast feeds decisions. It’s a continuous loop, not a once-a-quarter event.”

A Real-World Example: Margin Recovery Through Close Insights

Six months ago, Sarah noticed a three-point decline in gross margin on one product line. Flux analysis revealed a raw material price increase had quietly compressed margins.

She met with the product manager, discussed pricing, and tested a modest price increase on a segment of customers. Within three months, margins recovered, preserving six figures in profit.

“If we hadn’t caught that during the close,” Sarah says, “we would have lost substantial profit before anyone noticed. Early detection makes all the difference.”

Best Practices for Maximizing the Value of the Close

Sarah’s team has developed a set of best practices:

- Plan for the Close: Maintain a clear checklist and timeline. Reduces stress and frees time for analysis.

- Document Assumptions: Track accounting assumptions, accruals, and one-time adjustments. Ensures continuity.

- Focus on Material Variances: Prioritize variances with significant impact. Minor fluctuations are noted but not overanalyzed.

- Collaborate Across Teams: Schedule discussions with department heads rather than just sending reports.

- Integrate Insights into Forecasts: Treat the close as a feedback mechanism. Keep the forecast alive and evolving.

- Reflect and Improve: Maintain a decision journal. Record lessons, surprises, and actions to refine the process over time.

The Consequences of Skipping the Close-to-Plan Cycle

Companies that treat the close as purely mechanical often face:

- Decisions based on outdated information

- Delayed problem detection

- Missed opportunities

- Forecasts disconnected from reality

- Silos between departments

- Cash flow surprises and eroding margins

“The close is your early warning system,” Sarah reminds her team. “Without it, you’re flying blind.”

Connecting the Close to Broader Financial Concepts

The close links directly to lessons from previous tutorials in this series:

- Strategy to Cash Translation: The close tests whether strategic initiatives produce expected cash outcomes.

- Cash vs. Profit: The close reveals gaps between income statement results and cash flow realities.

- Economic Engines: The close tracks the performance of operational drivers like traffic, conversion, or utilization.

- Growth and Cash Consumption: The close shows how expansion affects working capital, inventory, and capital expenditure timing.

By integrating these lessons, the close becomes a concrete tool for understanding the business, not just an accounting exercise.

Conclusion: Transforming the Close into a Continuous Engine of Learning

Sarah stands before the leadership team. Reports are projected. On the surface, it’s a clean month: revenue slightly above forecast, stable margins, expenses in line.

But deeper insights emerge: receivables stretched, early margin pressure in one product line, supplier cost increases, marketing performance above expectation.

Decisions are made: pricing adjustments, marketing reallocation, focused receivables review. Actions are assigned. The close is complete—but the cycle continues.

In this tutorial, we have shown that the monthly financial close is far more than a reporting exercise. It is the heartbeat of the business, producing insight through variance and flux analysis, guiding leadership decisions, and feeding forecasts. By mastering this cycle, finance professionals elevate their role from compliance to strategic partnership, ensuring that every close contributes to sustainable growth and operational success.

Two weeks later, the cycle begins again—and Sarah will be ready.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.