Tutorial Categories

Last Updated: April 18, 2026 at 10:30

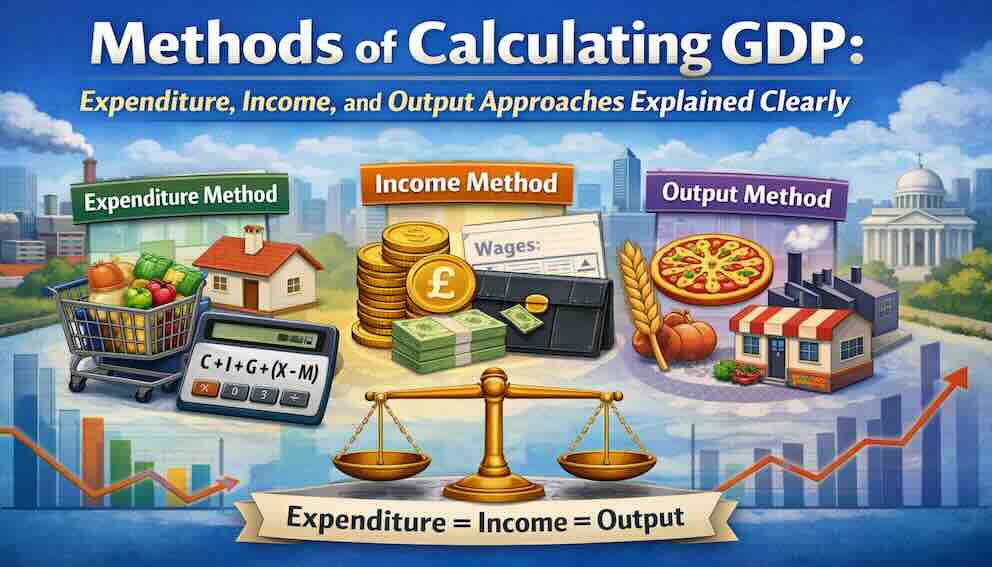

Methods of Calculating GDP: Expenditure, Income, and Output Approaches Explained Clearly

A Step-by-Step Guide to Understanding How Economists Measure National Output Using Three Complementary Perspectives

Gross Domestic Product (GDP) is one of the most important indicators used to understand the performance of an economy, yet the way it is calculated is often misunderstood. This tutorial explains the three main methods used to calculate GDP – the expenditure method (adding up all spending), the income method (adding up all earnings), and the output method (adding up value added at each stage of production) – in a clear and gradual way using a single running example of a pizza economy. You will learn why all three methods should theoretically produce the same number, what the statistical discrepancy tells us about data quality, and the crucial distinction between nominal GDP and real GDP. You will also discover the difference between gross GDP and net domestic product (NDP), why GDP per capita matters for understanding living standards, and what GDP leaves out. By the end, you will understand not just how GDP is calculated, but what it includes, what it leaves out, and why that matters for interpreting economic news.

Introduction: Why Are There Multiple Ways to Calculate GDP?

When economists talk about GDP, they are referring to the total value of all final goods and services produced within a country over a specific period, usually a year or a quarter. At first glance, it might seem that this total value could be calculated in only one straightforward way. But economic activity is complex and interconnected. Every transaction involves both a buyer and a seller, and it also generates income for someone involved in production.

Because of this interconnected nature, economists developed three different approaches to measure GDP, each focusing on a different aspect of the same economic activity. The expenditure method looks at spending. The income method looks at earnings. The output method looks at production. Although they approach measurement differently, all three methods should theoretically produce the same GDP figure if all data is recorded accurately. They are not competing approaches but complementary perspectives, like looking at the same object from different angles.

To see how this works numerically, let us use a single running example throughout this tutorial: a simple pizza economy. This economy produces only one thing – pizzas – but it has all the essential features of a real economy: households, firms, and a government. By tracking the same pizzas through all three methods, you will see exactly how the numbers match up.

The Expenditure Method: Measuring What People Spend

The expenditure method calculates GDP by adding up all the spending on final goods and services in an economy. This approach is based on a simple idea: everything that is produced is ultimately purchased by someone – whether a household, a business, the government, or a foreign buyer.

The formula for the expenditure method is:

GDP = C + I + G + (X − M)

Let us walk through each component using our pizza economy.

Consumption (C): This is spending by households on goods and services. In our pizza economy, when a family buys a pizza for dinner, that purchase counts as consumption. In a real economy, consumption includes groceries, rent, haircuts, petrol, cinema tickets, and medical services. It is typically the largest component of GDP, often making up 60 to 70 per cent of the total.

Investment (I): This does not refer to buying stocks or bonds. In GDP accounting, investment means spending on capital goods that will be used for future production – machinery, factory buildings, new housing, and software. In our pizza economy, when the pizza shop buys a new oven, that is investment. When a household buys a newly constructed home, that is also investment. Investment is the most volatile component of GDP, falling sharply in recessions and rising rapidly in booms.

A crucial part of investment that is often overlooked is inventory changes. If a pizzeria produces pizzas that are not sold immediately and are stored for later sale, this increase in inventory is counted as investment. This ensures that all production is included in GDP, even if it is not sold in the same period. Conversely, if a pizzeria sells more pizzas than it produced by drawing down its inventory, that reduction in inventory is subtracted from investment. Inventory changes are often small relative to total GDP, but they can be large during recessions when firms unexpectedly find themselves with unsold goods.

Government Spending (G): This includes spending by all levels of government on public services – education, healthcare, defence, roads, and police. In our pizza economy, if the government buys pizzas for a public event or pays teachers' salaries, that counts as government spending. However, transfer payments such as unemployment benefits or pensions are not included because they are not payment for newly produced goods or services. They are redistributions of income, not purchases of output.

Net Exports (X − M): This is exports (goods sold to foreign buyers) minus imports (goods bought from foreign producers). In our pizza economy, if a pizzeria in Naples sells pizzas to tourists from Germany, that is an export. If the pizza shop imports special Italian flour, that is an import, subtracted to avoid counting foreign production. A country with positive net exports sells more to the world than it buys; a country with negative net exports (a trade deficit) buys more than it sells.

Bringing It All Together – Our Pizza Economy Example: Suppose in one year, households spend £500,000 on pizzas (C). Pizzerias buy £50,000 in new ovens and add £10,000 to their inventory of unsold pizzas (I total = £60,000). The government spends £30,000 on pizzas for school lunches (G). The country exports £20,000 worth of pizzas and imports £10,000 worth of flour (X − M = £10,000). Total GDP by the expenditure method is £500,000 + £60,000 + £30,000 + £10,000 = £600,000.

What this means in practice: The expenditure method is widely used because spending data is relatively easy to collect from retail surveys, trade records, and government budgets. It provides a clear picture of demand in the economy – who is buying what.

The Income Method: Measuring What People Earn

While the expenditure method focuses on spending, the income method approaches GDP from the perspective of income earned by factors of production. The logic is simple: every time a good or service is produced and sold, income is generated for someone involved in the production process. That income must equal the value of what was produced.

The income method adds up all the incomes earned in an economy, then makes a few adjustments.

Wages and Salaries: These are payments to workers in exchange for labour – basic pay, bonuses, overtime, and benefits like employer pension contributions. In our pizza economy, the wages paid to pizza chefs and delivery drivers are part of GDP under the income method.

Profits: These are earned by business owners after covering costs. In our pizza economy, the profit the pizzeria owner makes on each pizza sold is counted here. This includes profits of corporations (paid to shareholders as dividends) and profits of sole proprietors.

Rent: This is income earned from leasing land or property. In our pizza economy, if the pizzeria rents its shop space from a landlord, the rent payment is income that contributes to GDP. Even for owner-occupied homes, statistical agencies estimate an "imputed rent" – the rent the owner would pay themselves – to ensure consistency across methods.

Interest: This is income earned by lending money. In our pizza economy, if the pizzeria took out a loan to buy its ovens, the interest paid to the bank is income that contributes to GDP.

Adjustments for Market Prices vs Factor Cost: This is an important conceptual step. GDP is usually measured at market prices – what consumers actually pay. But the income components we have listed (wages, profits, rent, interest) are measured at factor cost – what producers receive. The difference between market price and factor cost is indirect taxes (like sales tax or VAT) and subsidies. When you buy a pizza for £10, the pizzeria might receive only £8 after paying VAT. The £2 VAT is income for the government, not for the pizzeria. To move from factor cost to market prices, we add indirect taxes and subtract subsidies. This makes the adjustment feel intuitive: indirect taxes increase the price paid by consumers without increasing producer income, so they must be added; subsidies reduce the price paid, so they must be subtracted.

Depreciation: Capital goods wear out over time – ovens break, buildings age, computers become obsolete. This wear and tear is a cost of production, just like wages or raw materials. Depreciation is the value of capital that wears out during the year. Even though it is not paid out as income to anyone, it is part of the value of output and must be included. This is also where we get the distinction between gross and net measures. GDP is a gross measure because it includes depreciation. If we subtract depreciation, we get Net Domestic Product (NDP) . NDP tells us how much new value was created after accounting for the capital used up in production. In our pizza economy, if ovens worth £10,000 wear out during the year, that depreciation is included in GDP but not in NDP.

Our Pizza Economy Example – Continued: In the same year, workers earn £300,000 in wages. Pizzeria owners earn £200,000 in profits. Landlords receive £40,000 in rent. Banks receive £10,000 in interest. Indirect taxes (like VAT on pizzas) are £50,000. There are no subsidies. Depreciation on ovens is £10,000. Adding these: £300,000 + £200,000 + £40,000 + £10,000 + £50,000 + £10,000 = £610,000. Wait – this does not match the expenditure method total of £600,000. This is where the statistical discrepancy comes in.

Why this matters – The Statistical Discrepancy: In the real world, the three methods are based on different data sources. The expenditure method uses retail surveys, trade data, and government accounts. The income method uses tax records and payroll data. The output method uses production statistics from factories and service providers. Because these data sources are collected independently, they never match perfectly. Statistical agencies publish a "statistical discrepancy" – the difference between the three estimates – and make adjustments to bring them into alignment. A small discrepancy suggests confidence in the data; a large discrepancy suggests measurement problems. In our example, the discrepancy is £10,000, which might be adjusted by revising inventory estimates or adding a balancing item. In practice, the Office for National Statistics in the UK and the Bureau of Economic Analysis in the US spend considerable effort minimising this discrepancy.

How to interpret this: The income method shows how the value of output is distributed among workers (wages), business owners (profits), landlords (rent), lenders (interest), and the government (taxes). It is particularly useful for understanding inequality and the functional distribution of income.

The Output Method: Measuring Value Added at Each Stage

The output method, also known as the production method or value-added method, calculates GDP by adding up the value created at each stage of production. This approach avoids double counting, which would happen if we simply added up total sales.

Understanding Value Added: Value added is the increase in value that a firm contributes to a product. It is calculated as the firm's sales revenue minus the cost of intermediate goods (materials and services purchased from other firms). Summing value added across all firms in the economy gives us GDP.

Our Pizza Economy Example – Value Added: Suppose a pizza goes through three stages:

- A farmer grows wheat and sells it to a miller for £1.

- The miller grinds the wheat into flour and sells it to a pizzeria for £2.

- The pizzeria bakes the flour into a pizza and sells it to a customer for £5.

If we added up total sales (£1 + £2 + £5 = £8), we would be counting the wheat three times. Instead, we calculate value added at each stage:

- Farmer's value added = £1 (no inputs purchased)

- Miller's value added = £2 − £1 = £1

- Pizzeria's value added = £5 − £2 = £3

Total value added = £1 + £1 + £3 = £5 – exactly the price of the final pizza. Sum this across all pizzas and all other goods, and you get GDP.

How this works in practice: The output method is the primary method used for quarterly GDP estimates in many countries, including the United Kingdom and the United States. Statistical agencies collect data on production from factories, farms, mines, and service providers. They then subtract the cost of intermediate inputs to calculate value added. This approach is particularly useful for understanding which sectors of the economy are growing or shrinking. For example, if the services sector shows significant growth while manufacturing declines, this provides insight into structural changes in the economy. In the United Kingdom, services account for about 80 per cent of GDP, manufacturing about 10 per cent, and agriculture less than 1 per cent.

Why this matters: The output method avoids double counting and provides a sector-by-sector breakdown of economic activity. It is the method most closely tied to actual production data.

Why the Three Methods Match – The Circular Flow

One of the most important concepts in GDP measurement is that all three methods should, in theory, produce the same result. This consistency exists because of the circular flow of income. When a product is sold, it represents expenditure by the buyer, income for the seller, and output produced – three perspectives on the same transaction. In our pizza economy, a £5 pizza purchase is simultaneously £5 of consumption spending (expenditure method), £5 of income to the pizzeria owner and workers (income method), and £5 of value added by the pizzeria (output method). The three methods are like three different cameras filming the same event from different angles.

In practice, the three methods rarely match perfectly because they rely on different data sources – retail surveys, tax records, production statistics. The difference is called the statistical discrepancy. A small discrepancy suggests confidence in the data; a large discrepancy suggests measurement problems. The circular flow of income and the relationship between the three methods is explored in more detail in a separate tutorial.

Nominal vs Real GDP – Adjusting for Inflation

So far, we have measured GDP at current prices – the prices that prevailed when the goods were sold. This is called nominal GDP. But nominal GDP can rise for two reasons: the economy produced more, or prices increased. To understand whether the economy is actually growing, we need to separate these two effects.

Real GDP adjusts for inflation by measuring output using constant prices from a base year. When economists report that GDP grew by a certain percentage, they are almost always referring to real GDP growth, because it reflects changes in actual production rather than price increases. The distinction between nominal and real GDP, along with the GDP deflator and methods like chained dollars, is covered in detail in a separate tutorial.

GDP per Capita – Adjusting for Population

GDP alone tells you the size of an economy. But it does not tell you how rich the average person is. If GDP grows but population grows faster, average living standards may not improve. GDP per capita divides total GDP by the population. It is a better approximation of average income and living standards.

For example, China has a larger GDP than Japan, but Japan has a much higher GDP per capita because its population is smaller. When comparing living standards across countries, economists almost always use GDP per capita rather than total GDP. When comparing growth over time, they often use real GDP per capita – adjusting for both inflation and population.

How to interpret this: GDP per capita is not a perfect measure of well-being (it says nothing about inequality, health, or happiness), but it is the best single number we have for comparing average living standards across countries.

What GDP Excludes – The Limitations

GDP is a powerful tool, but it is important to understand what it leaves out. GDP excludes non-market activities (household work, volunteering), the underground economy (cash-in-hand work, illegal activities), environmental degradation (pollution, resource depletion), quality improvements and new goods, and the distribution of income (inequality). These exclusions mean GDP is a measure of market economic activity, not a complete measure of well-being. A full discussion of the limitations of GDP, including alternative measures of well-being, is covered in a separate tutorial.

GDP per Capita – Adjusting for Population

GDP alone tells you the size of an economy. But it does not tell you how rich the average person is. If GDP grows but population grows faster, average living standards may not improve. GDP per capita divides total GDP by the population. It is a better approximation of average income and living standards.

For example, China has a larger GDP than Japan, but Japan has a much higher GDP per capita because its population is smaller. When comparing living standards across countries, economists almost always use GDP per capita rather than total GDP. When comparing growth over time, they often use real GDP per capita – adjusting for both inflation and population.

How to interpret this: GDP per capita is not a perfect measure of well-being (it says nothing about inequality, health, or happiness), but it is the best single number we have for comparing average living standards across countries.

What GDP Excludes – The Limitations

GDP is a powerful tool, but it is important to understand what it leaves out. These exclusions are not flaws in the concept of GDP; they are deliberate choices about what to measure. But they mean that GDP does not tell us everything about economic well-being.

Non-Market Activities: GDP counts only transactions that occur in markets. If you hire a cleaner, that contributes to GDP. If you clean your own house, it does not. If you pay for childcare, it contributes to GDP. If a parent stays home to care for children, it does not. This means GDP systematically understates total economic activity, especially in countries where much work is done within households or in informal arrangements.

The Underground Economy: GDP excludes illegal activities (drugs, unlicensed gambling) and legal activities that are not reported to tax authorities (cash-in-hand work). In some countries, the underground economy is very large – estimates range from 10 per cent of GDP in advanced economies to over 40 per cent in some developing countries. This means official GDP figures may miss a substantial portion of actual economic activity.

Environmental Degradation: GDP counts the value of goods produced, but it does not subtract the cost of environmental damage. If a country cuts down its forests to produce timber, GDP rises. The loss of the forest – carbon storage, biodiversity, flood protection – is not subtracted. If a factory pollutes a river, the pollution is not deducted from GDP, though the cost of cleaning it up might be added later. This is one of the most serious criticisms of GDP as a measure of well-being.

Quality Changes and New Goods: GDP struggles to account for improvements in quality. A smartphone today is vastly better than a smartphone from ten years ago, but if the price is the same, GDP records no increase. Similarly, new goods (like streaming services) take time to be properly incorporated into GDP statistics. This means GDP may understate improvements in living standards.

Distribution: GDP tells us the size of the economy, but nothing about who gets the benefits. A country could have rising GDP while most citizens see stagnant incomes, if growth is concentrated among the wealthiest. This is why economists also look at measures of inequality, such as the Gini coefficient.

Why this matters: Understanding what GDP excludes helps you interpret economic data more critically. A country with high GDP growth but rising inequality and environmental degradation may not be improving well-being as much as the headline number suggests.

Seasonal Adjustment – Making Quarterly Comparisons Meaningful

Many economic activities follow predictable seasonal patterns. Retail sales surge in December due to Christmas shopping. Construction slows in winter. Agricultural output peaks at harvest time. These seasonal patterns mean that comparing GDP in one quarter to the previous quarter can be misleading – a drop from Q4 to Q1 might just reflect normal seasonal patterns, not a real economic slowdown.

Seasonal adjustment is a statistical technique that removes these predictable seasonal patterns. Statistical agencies estimate how much each quarter typically differs from the annual average, then adjust the data to remove that difference. The result is "seasonally adjusted" GDP, which can be compared from quarter to quarter without seasonal effects distorting the picture.

For example, the UK Office for National Statistics publishes both raw and seasonally adjusted GDP. The raw data show large spikes in Q4 (Christmas) and troughs in Q1 (post-Christmas). The seasonally adjusted data smooth these out, allowing economists to see the underlying trend.

How to interpret this: Most reported GDP figures are seasonally adjusted. When you hear that GDP fell by 0.1 per cent in the first quarter, that is already adjusted for seasonal patterns. The raw data would show a much larger drop, but that drop would be mostly due to post-Christmas slowdown, not a real economic contraction.

Gross vs Net – GDP and NDP

We mentioned depreciation earlier. Let us make the distinction explicit. Gross Domestic Product (GDP) is a gross measure because it includes depreciation – the value of capital that wears out during the year. Net Domestic Product (NDP) is GDP minus depreciation. NDP tells us how much new value was created after accounting for the capital used up in production.

Why does this matter? If an economy invests just enough to replace worn-out capital, GDP will be positive but NDP will be zero. The economy is not adding to its productive capacity; it is merely maintaining what it has. If an economy does not invest enough to replace worn-out capital, NDP will be negative, meaning the capital stock is shrinking. This is an important warning sign that is hidden by GDP alone.

In our pizza economy, if depreciation is £10,000 and GDP is £600,000, then NDP is £590,000. The economy added £590,000 of new value after accounting for the ovens that wore out.

How to interpret this: GDP is the more commonly reported figure, but NDP provides a cleaner measure of sustainable growth. A country that has high GDP growth but very high depreciation (perhaps because its capital stock is old and inefficient) may not be adding as much new productive capacity as the headline suggests.

Conclusion: Three Perspectives, One Reality

The three methods of calculating GDP are not competing approaches but complementary perspectives that together provide a complete picture of economic activity. The expenditure method shows how demand drives production – who is buying what. The income method reveals how the value of that production is distributed – who earns what. The output method highlights the structure of production across different sectors – where value is added. Every purchase is someone else's income, and every act of production contributes to both spending and earnings. This interconnectedness is why all three methods, when measured accurately, arrive at the same number. But GDP is not a perfect measure. It excludes non-market activities, the underground economy, and environmental degradation. It does not account for quality improvements or the distribution of income. And it requires adjustments – for inflation (real GDP), for population (GDP per capita), for depreciation (NDP), and for seasonal patterns – to be comparable over time. Understanding these nuances is essential for interpreting economic news. When you hear that GDP grew by 2 per cent last quarter, you can now ask: was that nominal or real? Seasonally adjusted or raw? Does that growth account for population growth? Does it reflect actual increases in production or just price increases? And what does that growth number leave out – the value of unpaid work, the cost of pollution, the distribution of the gains? By understanding how GDP is calculated – and what it does and does not measure – you become a more informed reader of economic data, better equipped to see through headlines and understand the actual health of the economy.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.