Tutorial Categories

Last Updated: April 19, 2026 at 10:30

Business Cycles & Economic Fluctuations: Understanding the Rhythm of Booms and Busts

A Step-by-Step Guide to the Phases of Expansion, Peak, Recession, and Trough—and What Causes Economies to Move Through Them

This tutorial explores the business cycle—the recurring pattern of expansion and contraction that characterizes every market economy. You will learn the four phases of the cycle: expansion, when the economy grows and jobs are plentiful; peak, the turning point when growth maxes out; recession, when output falls and unemployment rises; and trough, the bottom from which recovery begins. We will examine the forces that drive these fluctuations, from shifts in aggregate demand and supply to the role of financial markets, credit cycles, and animal spirits, and see how these forces often combine to amplify the cycle. Using real-world examples from the Great Depression and the 1970s oil shocks, this tutorial shows how business cycles are not random events but the result of identifiable forces—and why understanding them is essential for navigating the economy.

Introduction: The Economy's Natural Rhythm

The economy does not grow in a straight line. It expands, then slows, then contracts, then recovers. This rhythm is the business cycle.

The business cycle is one of the oldest and most persistent observations in economics. Since the dawn of industrial capitalism, economies have moved through recurring patterns of boom and bust. In the 19th century, these cycles were often tied to agricultural harvests and banking panics. In the 20th century, they became linked to industrial production, consumer confidence, and financial markets. In the 21st century, they are shaped by globalization, technology, and the extraordinary power of central banks.

Understanding the business cycle is essential for understanding why people lose jobs, why businesses fail, why stock markets crash, and why governments spend trillions of dollars trying to stabilize the economy. It is also essential for understanding why, despite these cycles, the long-run trend of economic growth has lifted billions out of poverty. The cycle is not the whole story, but it is an essential part of it.

In this tutorial, we will explore the phases of the business cycle: expansion, peak, recession, and trough. We will examine the forces that drive these fluctuations—from shifts in aggregate demand and supply to the role of financial markets, credit cycles, and the unpredictable swings of human confidence. We will see how these forces often combine and amplify each other, turning small shocks into major downturns. And we will trace the cycle through two powerful real-world examples: the Great Depression, which taught the world the cost of inaction, and the 1970s oil shocks, which revealed the unique challenge of stagflation. By the end, you will see that the business cycle is a pattern we can understand and, to some extent, manage.

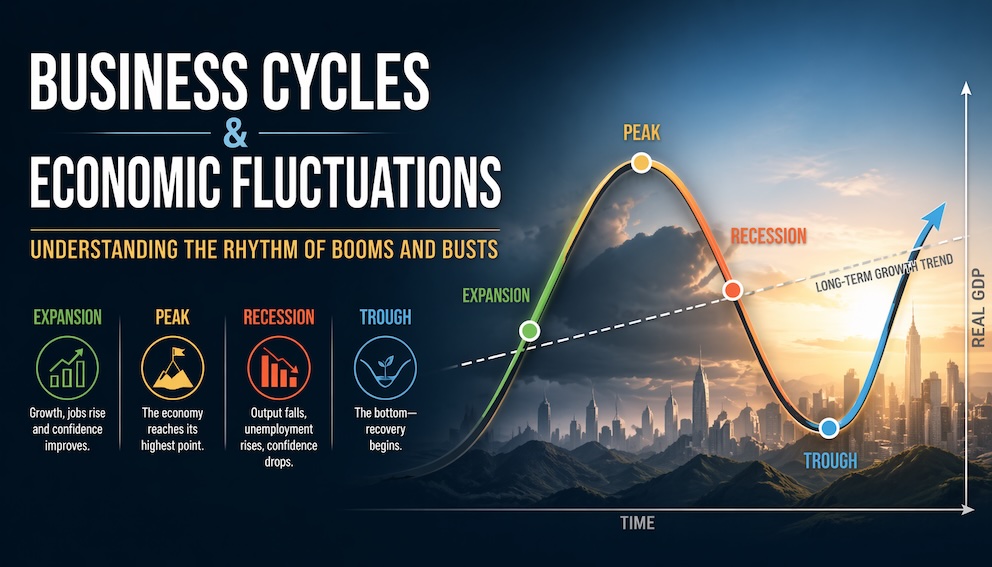

The Four Phases – From Boom to Bust and Back Again

The business cycle is typically divided into four phases. These phases are not of fixed duration; some expansions last for years, others for months. Some recessions are deep and long; others are shallow and short. But the sequence is remarkably consistent.

To visualize the cycle, imagine a graph with time on the horizontal axis and real GDP on the vertical axis. The line moves upward over the long run—this is economic growth. But it does not move in a straight line. It rises, peaks, falls, bottoms out, and rises again. This wave-like pattern is the business cycle.

Expansion: The Climb Upward

An expansion is a period when the economy is growing. Output (GDP) is rising, employment is increasing, incomes are growing, and consumer and business confidence is generally positive. Expansions are the normal state of a healthy economy. In the United States, the average expansion since World War II has lasted about five to six years, but some have been much longer. The expansion from 2009 to 2020 was the longest on record, lasting over a decade.

During an expansion, businesses hire workers, invest in new equipment, and expand production. Households spend more, confident that their incomes will continue to rise. Banks lend freely, and credit is available. As the expansion continues, the economy approaches its potential output. Resources become tighter. Labor markets tighten, and wages begin to rise more quickly. Eventually, the expansion reaches its limit.

Peak: The Turning Point

The peak is the highest point of the business cycle. It is not a period of time but a turning point—the moment when expansion stops and contraction begins. At the peak, the economy is operating at or above its potential. Unemployment is low—often below what economists consider the natural rate. Factories are running at high capacity. Inflationary pressures often build as demand outruns supply.

Peaks are often marked by excesses. In the 1920s, the peak was marked by a speculative bubble in stocks. In the 1970s, the peak was followed by a sharp contraction triggered by oil price shocks. Peaks are not always easy to identify in real time. The National Bureau of Economic Research (NBER), which officially dates recessions in the United States, often declares the peak months after it has passed.

Recession: The Descent

A recession is a significant decline in economic activity that spreads across the economy and lasts more than a few months. The NBER looks at a range of indicators: real GDP, real income, employment, industrial production, and wholesale-retail sales. A common rule of thumb is two consecutive quarters of negative GDP growth, but the NBER uses a broader definition.

During a recession, businesses cut back on production, lay off workers, and postpone investment. Households reduce spending, worried about job security. Banks become cautious, tightening lending standards. Confidence evaporates. The decline can be self-reinforcing: falling incomes lead to falling spending, which leads to further job losses, which leads to further falls in income. This is the downward spiral of a recession.

Not all recessions are alike. Some are mild and short. Others are severe and prolonged. The Great Depression of the 1930s lasted over a decade, with GDP falling by nearly 30 percent and unemployment reaching 25 percent. The recessions of the 1970s, triggered by oil shocks, were shorter but brought the novel challenge of rising prices during economic contraction—a phenomenon known as stagflation.

Trough: The Bottom

The trough is the lowest point of the business cycle. Like the peak, it is a turning point—the moment when contraction stops and expansion begins. At the trough, output is at its lowest, unemployment is at its highest, and capacity utilization is at its minimum. Business and consumer confidence are often at rock bottom.

From the trough, recovery begins. The economy starts to grow again, slowly at first, then more rapidly as confidence returns. The trough is often hard to recognize in real time; the NBER typically declares it months after the fact. But it is the foundation of the next expansion.

Key takeaway: The business cycle has four phases: expansion (growth), peak (the top), recession (contraction), and trough (the bottom). Expansions are the normal state, but they inevitably give way to recessions, which eventually give way to recoveries. The cycle is not a law of nature, but it is a persistent feature of market economies.

What Causes Business Cycles? The Forces Behind the Rhythm

If the business cycle is a recurring pattern, what drives it? Economists have debated this question for centuries. No single explanation accounts for all cycles, but several forces consistently appear. Importantly, these forces rarely act alone. They interact and amplify each other, turning small disturbances into major fluctuations.

Shifts in Aggregate Demand

The AD-AS model provides the most straightforward explanation. Business cycles are often driven by shifts in aggregate demand. A positive demand shock—a surge in consumer confidence, a tax cut, a wave of investment—shifts AD right, pushing the economy into an expansion. A negative demand shock—a collapse in confidence, a financial crisis, a cut in government spending—shifts AD left, pushing the economy into a recession.

The Great Depression was driven by a massive negative demand shock. The stock market crash of 1929 shattered confidence. Banks failed, wiping out savings. The money supply contracted sharply. Consumers and businesses stopped spending. The AD curve shifted far left, creating a deep and prolonged recessionary gap.

Shifts in Aggregate Supply

Supply shocks can also cause business cycles. A negative supply shock—a spike in oil prices, a disruption in supply chains, a natural disaster—shifts SRAS left, reducing output and raising prices. The 1970s oil shocks are the classic example. When OPEC embargoes quadrupled the price of oil, the SRAS curve shifted sharply left. The result was stagflation: output fell and inflation rose.

Positive supply shocks—a technological breakthrough, a fall in energy prices, a surge in productivity—shift SRAS right, boosting output and lowering prices. The 1990s technology boom was a positive supply shock that contributed to strong growth with low inflation.

Financial Cycles and Credit

One of the most important drivers of business cycles is the financial system. Credit expands and contracts in cycles that amplify the ups and downs of the economy. During good times, banks lend freely, asset prices rise, and borrowers take on more debt. This fuels further spending and investment, pushing the expansion forward. But as debt accumulates, the system becomes fragile. When a shock hits—a rise in interest rates, a fall in asset prices—the credit cycle reverses. Banks tighten lending, borrowers struggle to repay, and defaults rise. The contraction in credit amplifies the downturn.

The Great Depression was, in part, a credit cycle crisis. A decade of easy credit in the 1920s fueled a speculative bubble in stocks. When the bubble burst, banks failed, and the credit contraction turned a stock market correction into a decade-long catastrophe.

Animal Spirits and Confidence

The economist John Maynard Keynes used the term animal spirits to describe the spontaneous, often irrational swings in confidence that drive investment and consumption. When people are optimistic, they spend and invest. When they are pessimistic, they hoard cash and cut back. These swings in confidence can become self-fulfilling.

The Great Depression is the classic example. The stock market crash of 1929 shattered confidence. Businesses stopped investing. Consumers stopped spending. Banks failed as depositors rushed to withdraw their money. The collapse in confidence turned a stock market correction into a decade-long catastrophe.

External Shocks

Sometimes, business cycles are triggered by events outside the economy. Wars, pandemics, natural disasters, and geopolitical shocks can all cause sharp contractions. The oil shocks of the 1970s were external shocks—geopolitical events that disrupted global energy supplies and sent shockwaves through industrialized economies.

How Forces Combine: The Amplification Mechanism

These forces rarely act in isolation. They interact and amplify each other. The Great Depression saw a stock market crash (external shock) trigger a collapse in confidence (animal spirits), which caused a wave of bank failures (credit cycle contraction), which produced a massive negative demand shock (AD shift). The forces reinforced each other, turning a financial panic into the deepest economic contraction in modern history.

The 1970s saw external shocks (oil embargoes) combine with existing inflationary pressures to create stagflation—a combination of falling output and rising prices that challenged everything economists thought they knew about the cycle.

Leading and Lagging Indicators: How Economists Read the Cycle

Economists do not wait for history to tell them when the cycle has turned. They watch a set of leading indicators—measures that tend to change before the overall economy changes. These include stock market prices (which reflect expectations of future profits), building permits (which signal future construction), consumer confidence surveys (which predict future spending), and the yield curve (which has historically predicted recessions).

Coincident indicators—like GDP, employment, and industrial production—tell economists where the economy is right now. Lagging indicators—like the unemployment rate and the duration of unemployment—confirm what has already happened. By tracking these indicators, economists can gauge the phase of the cycle and anticipate turning points, even if official dates are only determined later.

Key takeaway: Business cycles are driven by shifts in aggregate demand, shifts in aggregate supply, the expansion and contraction of credit, swings in confidence (animal spirits), and external shocks. These forces rarely act alone; they interact and amplify each other, turning small disturbances into major fluctuations. Leading, coincident, and lagging indicators help economists read the cycle in real time.

Real-World Examples – The Cycle in Action

Let us walk through two powerful business cycles that shaped modern macroeconomics. One is foundational—the Great Depression—and one reveals a unique challenge—the 1970s oil shocks and stagflation. Together, they illustrate the diversity of cycles and the lessons they taught economists and policymakers.

The Great Depression (1929–1939): When Forces Combined

The Great Depression was the most severe business cycle in modern history. It began with a stock market crash in October 1929, but the crash was only the trigger. The deeper forces were already in place: a decade of easy credit had fueled a speculative bubble; banks were overextended; inequality was high; and the global economy was fragile.

When the bubble burst, confidence evaporated. Businesses stopped investing. Consumers stopped spending. Banks failed as depositors rushed to withdraw their money. Between 1929 and 1933, the money supply fell by one-third. The Federal Reserve, still in its infancy, did not act to stem the contraction; in fact, it raised interest rates in 1931, making the downturn worse. The government, operating under the belief that budgets should be balanced even in recessions, did not increase spending.

The forces—confidence collapse, credit contraction, demand collapse—combined and amplified each other. The result was catastrophic. GDP fell by nearly 30 percent from its peak. Unemployment rose from 3 percent to 25 percent. Thousands of banks failed. Industrial production was cut in half. The downturn was so deep and so long that it earned the name "Depression" rather than "recession."

It was not until World War II, with massive government spending and the mobilization of the entire economy, that the United States finally emerged from the Depression. The Great Depression taught economists that business cycles are not self-correcting in the short run. It gave birth to Keynesian economics and the idea that government must act to stabilize aggregate demand during downturns. It also created the institutions—the Federal Deposit Insurance Corporation (FDIC), Social Security, and later the Employment Act of 1946—that would make future recessions less severe.

What the Great Depression Teaches Us: The Great Depression shows how multiple forces—a speculative bubble, a credit contraction, a collapse in confidence, and policy inaction—can combine to turn a financial panic into a decade-long catastrophe. It also shows that policy matters: where the government acted, the recovery began; where it did not, the suffering continued.

The 1970s Oil Shocks and Stagflation (1973–1975, 1979–1980): The Supply-Side Challenge

The 1970s brought a different kind of business cycle—one that challenged the prevailing wisdom of the time. In October 1973, Arab members of OPEC (the Organization of Petroleum Exporting Countries) imposed an oil embargo on nations that had supported Israel in the Yom Kippur War. The price of crude oil quadrupled almost overnight. A second oil shock followed in 1979, after the Iranian Revolution disrupted oil supplies.

These were pure negative supply shocks. Oil is a foundational input for almost every industry—transportation, manufacturing, heating, electricity generation, agriculture. When the price of oil quadruples, costs rise across the entire economy. The SRAS curve shifted sharply to the left.

The result was a combination that economists had not seen before: output fell (recession) and prices rose (inflation). They called it stagflation—stagnation plus inflation. Unemployment rose from 4 percent in 1973 to 9 percent in 1975, while inflation rose from 6 percent to over 12 percent. When the second oil shock hit in 1979, inflation soared above 14 percent, and the economy again fell into recession.

Stagflation presented a cruel trade-off for policymakers. The traditional tools of demand management—monetary and fiscal policy—could not solve the problem. If they tried to fight the recession by increasing demand, they would worsen inflation. If they tried to fight inflation by reducing demand, they would deepen the recession. The economy was trapped.

It was not until the early 1980s, when the Federal Reserve under Paul Volcker raised interest rates dramatically (to over 20 percent), that inflation was finally broken. But the cost was a deep recession—the deepest since the Great Depression—with unemployment reaching nearly 11 percent.

What the 1970s Oil Shocks Teach Us: The oil shocks revealed that not all recessions are demand-driven. Supply shocks can cause output to fall and prices to rise simultaneously—a condition that standard demand-side policies cannot easily address. They also showed the importance of energy independence, the vulnerability of industrialized economies to external shocks, and the critical role of inflation expectations. The 1970s gave birth to the concept of "inflation expectations" and taught central banks that they must be credible in their commitment to price stability.

The Contrast: Demand Shocks vs Supply Shocks

These two examples illustrate the two great types of business cycles. The Great Depression was a demand-side cycle—a collapse in spending, confidence, and credit that caused output to plummet and prices to fall (deflation). The 1970s oil shocks were supply-side cycles—external shocks that raised costs, causing output to fall and prices to rise (stagflation).

Understanding the difference is essential for understanding policy. In a demand-driven downturn, the prescription is to boost demand—lower interest rates, increase government spending, cut taxes. In a supply-driven downturn, the prescription is more complex: policymakers must address the root cause of the supply disruption while managing the trade-off between output and inflation.

Key takeaway: The Great Depression shows the devastation of a demand-driven cycle compounded by policy inaction. The 1970s oil shocks show the unique challenge of supply-driven cycles and stagflation. Together, they illustrate the two great types of business cycles and the lessons they taught economists about the forces that drive economic fluctuations.

The Human Impact – Why the Cycle Matters

Business cycles are not abstract lines on a graph. They affect real people in real ways.

During a recession, unemployment rises. Families lose their primary source of income. Home foreclosures increase. Young people graduate into a labor market that has no jobs for them, and studies show that graduating during a recession can depress lifetime earnings for decades. Small businesses—the engine of job creation—close at higher rates. The stress of job loss and financial insecurity affects mental health, family stability, and community well-being.

During the Great Depression, one in four workers was unemployed. Families lost their homes. Bread lines stretched for blocks. The human toll was immeasurable. During the 1970s recessions, unemployment rose to 9 percent, and the combination of job loss and rising prices meant that families faced both lost income and higher costs for essentials like heating and gasoline.

During an expansion, the opposite happens. Jobs are plentiful. Incomes rise. Families can buy homes, send children to college, and save for retirement. Businesses expand, investing in new equipment and hiring more workers. Communities thrive.

The human impact of the cycle is why policymakers work so hard to smooth it. It is why central banks cut interest rates when the economy slows. It is why governments created unemployment insurance, the FDIC, and Social Security. The goal is not to eliminate the cycle—that is impossible—but to make the downturns shallower and shorter, and to prevent the kind of catastrophic collapse that occurred in the 1930s.

Key takeaway: Business cycles have real human consequences. Recessions bring job loss, financial insecurity, and long-term damage to careers and communities. Expansions bring opportunity, rising living standards, and security. This is why stabilizing the cycle is a central goal of economic policy.

The Role of Policy – Can We Tame the Cycle?

If business cycles are inevitable, can we do anything about them? The answer is yes—up to a point.

Monetary Policy: Managing Demand

Central banks use monetary policy to smooth the business cycle. When the economy is in recession, they lower interest rates to encourage borrowing and spending, shifting AD right. When the economy is overheating, they raise interest rates to cool demand, shifting AD left. The Federal Reserve's actions in response to the 1970s stagflation—raising rates dramatically to break inflation—illustrate the power and the pain of monetary policy.

Monetary policy is not perfect. It works with lags—it can take months or even years for interest rate changes to fully affect the economy. Its effects can be unpredictable. In a deep recession, when interest rates are already near zero, central banks must turn to unconventional tools. But despite these limitations, monetary policy has been remarkably successful at reducing the severity of recessions since World War II.

Fiscal Policy: Direct Spending and Taxes

Governments also use fiscal policy to stabilize the cycle. During recessions, they can increase spending or cut taxes to boost demand. The New Deal programs of the 1930s were an early experiment in fiscal policy, though they were not large enough to end the Depression. The massive government spending of World War II finally did.

Fiscal policy can be more targeted than monetary policy—it can put money directly into the hands of those most likely to spend it. But fiscal policy is subject to political delays and debates. By the time a stimulus bill is passed, the economy may already be recovering.

Automatic Stabilizers

Not all stabilization requires deliberate action. Automatic stabilizers—unemployment insurance, progressive taxes, welfare programs—automatically cushion the cycle. When the economy falls into recession, unemployment benefits rise and tax revenues fall, putting money back into the economy without any new legislation. These stabilizers were created in response to the Great Depression and are one reason recessions have become less severe in the postwar era.

The Limits of Policy

Despite these tools, we cannot eliminate the business cycle entirely. Shocks will always occur. Confidence will always swing. Credit cycles will always amplify. The goal of policy is not to end the cycle but to smooth it—to make recessions shallower and shorter, and to prevent the kind of catastrophic collapse that occurred in the 1930s.

Moreover, policy works with lags and under uncertainty. Policymakers rarely know the exact state of the economy in real time. By the time they act, the cycle may already have turned. And policies can have unintended consequences—stimulus that is too large can cause inflation; tightening that is too aggressive can trigger a recession. The 1970s showed that even well-intentioned policies can struggle in the face of supply shocks.

Key takeaway: Monetary policy, fiscal policy, and automatic stabilizers can reduce the severity of business cycles, but they cannot eliminate them. The goal is to smooth the cycle, not to end it. Policy works with lags and under uncertainty, and there are limits to what it can achieve—especially in the face of supply shocks.

Conclusion: The Cycle That Never Ends

The business cycle is the economy's natural rhythm. It is the pattern of expansion and contraction that has accompanied market economies since the dawn of industrial capitalism. We have traced the four phases—expansion, peak, recession, trough—and seen how they flow into one another. We have examined the forces that drive the cycle: shifts in demand, shifts in supply, the ebb and flow of credit, the unpredictable swings of confidence, and the external shocks that can upend everything. We have seen how these forces interact and amplify each other, turning small disturbances into major fluctuations. And we have walked through two cycles that shaped modern macroeconomics: the Great Depression, which taught the world the cost of inaction and the power of combined forces, and the 1970s oil shocks, which revealed the unique challenge of supply-driven cycles and stagflation.

Understanding the business cycle is not about predicting the next turning point. No one can do that reliably. It is about understanding the forces that shape economic fluctuations, the tools that can moderate them, and the limits of what policy can achieve. It is about recognizing that expansions do not last forever and that recessions are not permanent. It is about seeing the economy not as a straight line but as a rhythm—a rhythm that we can sometimes influence but never fully control.

The cycle matters because it affects real people. Recessions bring job loss, financial insecurity, and long-term damage to careers and communities. Expansions bring opportunity, rising living standards, and security. This is why stabilizing the cycle is a central goal of economic policy. It is why central bankers watch the data so closely. It is why governments created unemployment insurance, deposit insurance, and the other stabilizers that make modern recessions less devastating than the Great Depression.

The cycle will continue. There will be more booms and more busts. New shocks will arise—new technologies, new financial innovations, new geopolitical tensions, perhaps new energy crises. The shape of the cycle will change. But the underlying pattern will remain. The economy will expand, peak, contract, and trough. And then it will expand again. Understanding that rhythm doesn’t give us perfect foresight, but it does help us prepare—for the downturns to hurt less and the recoveries to start sooner. That is why studying the business cycle still matters.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.