Tutorial Categories

Last Updated: April 21, 2026 at 10:30

How Banks Create Money: The Hidden Process That Powers Modern Economies

A step-by-step guide to deposit creation, balance sheet mechanics, credit expansion, and the real-world constraints that limit money creation

This tutorial reveals one of the most misunderstood concepts in economics: how banks actually create money. You will learn that banks do not simply lend out existing deposits—instead, they create new money when they issue loans. We will walk through the deposit creation process step by step, using balance sheets to show how a single loan expands both sides of a bank's accounts. We will trace the life cycle of money—from creation through circulation to destruction—and examine why the traditional "money multiplier" story is a classroom simplification that does not reflect how modern banking works. We will also explore the real-world constraints on money creation, including capital requirements, demand for loans, and interest rates. Using real-world examples from China's credit boom and the UK mini-budget crisis, this tutorial clarifies the fundamental process that underpins economic growth and financial instability.

Introduction: The Great Misunderstanding

Imagine a bank. Most people think of it as a safe place where people deposit their money, and the bank then lends that money out to borrowers. In this common view, deposits come first, then loans. The bank is simply a middleman, passing money from savers to borrowers.

That is not how it works.

In reality, the process works in reverse. Loans create deposits. When a bank makes a loan, it does not hand out money that someone else deposited. Instead, it creates new money right there on the spot and adds it to the borrower's account. The borrower then spends that money, and it circulates through the economy, eventually becoming deposits in other banks. This is how most money in modern economies is created.

A quick note on terminology. Bank deposits are not a separate kind of money. They are promises to pay central bank money. When you have $1,000 in your checking account, the bank owes you $1,000 of central bank money. This hierarchy matters: central bank money sits at the base, and bank deposits are the second layer built on top of it.

Understanding this process matters. If money is created through lending, then the amount of money in the economy depends on banks' willingness to lend and borrowers' willingness to borrow. When banks lend freely, money expands. When they stop lending, money contracts. This is the hidden engine of the business cycle.

In this tutorial, we will walk through how banks create money, step by step. We will look at balance sheets to see how a single loan expands a bank's accounts. We will trace the life cycle of money from creation to destruction. We will explore why banks cannot create unlimited money, and we will look at real-world examples from China, the 2008 crisis, and the United Kingdom. By the end, you will understand a process that is central to modern economies but widely misunderstood.

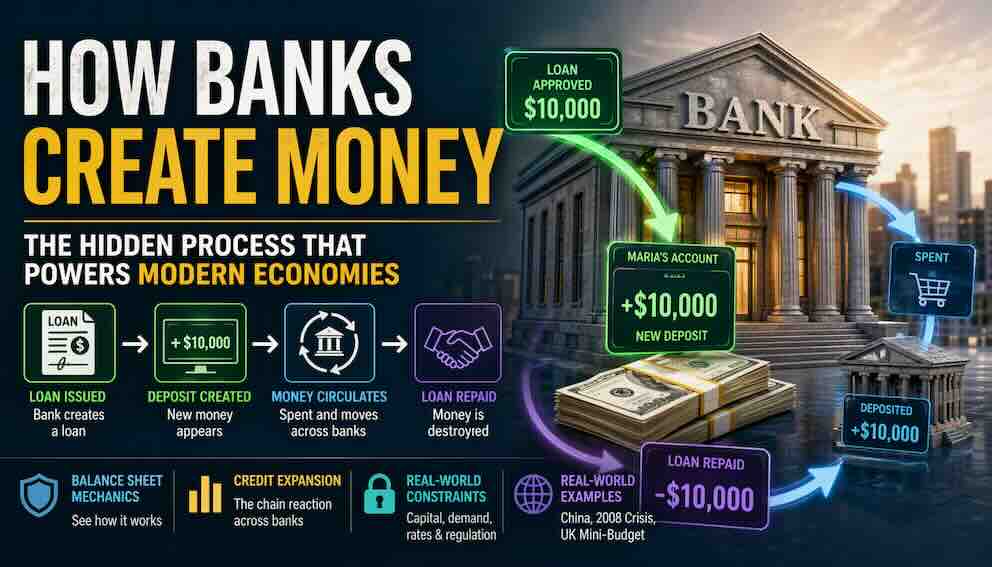

A Simple Example: Maria's Bakery

Let us start with a small business owner named Maria. She wants to expand her bakery. She needs a new oven that costs $10,000. She goes to her bank, First National Bank, and applies for a loan. The bank reviews her credit and her business plan and decides to approve the loan.

At the moment the loan is approved, the bank does not go to a vault and pull out $10,000 that someone else deposited. Instead, it adds $10,000 to Maria's checking account. In return, Maria promises to repay the loan with interest. That promise is an asset for the bank. The new deposit is a liability for the bank—it owes Maria the money.

Before the loan, the money supply did not include that $10,000. After the loan, it does. Maria can now spend that money. The bank has created new money.

This is the fundamental insight. Banks do not need to have existing deposits to make loans. They create the deposits when they make the loans. However, a quick clarification is worth making. Banks do not need prior deposits, but they still rely on deposits as a stable and low-cost source of funding. This influences how much they are willing to lend and how they manage their balance sheets over time.

Now Maria spends the $10,000 to buy the oven from an equipment supplier. She writes a check or makes an electronic transfer. The supplier deposits the $10,000 in their own bank, Second National Bank. The money has moved from First National Bank to Second National Bank.

First National Bank's deposits decrease by $10,000 because it no longer owes that money to Maria. Its reserves also decrease by $10,000 because it must transfer reserves to Second National Bank. Second National Bank's deposits increase by $10,000, and its reserves increase by $10,000.

Here is the crucial point. The money that was created when First National Bank made the loan does not disappear. It has simply moved. The total money supply remains larger by $10,000 than it was before the loan was made.

A Note on Types of Money

Before we go further, it helps to distinguish between different forms of money. In modern economies, there are three main types.

Cash is physical money issued by the central bank. This includes notes and coins. It is the only form of money that the public can hold directly.

Central bank reserves are money that commercial banks hold in their accounts at the central bank. Only banks can use reserves. The public never sees or touches them.

Commercial bank deposits are the money in your checking and savings accounts. This is the form of money that most people use every day. It is created by commercial banks when they make loans. Remember, these deposits are promises to pay central bank money.

In this tutorial, we are focusing on the creation of commercial bank deposits. That is the money that makes up most of the money supply. When a bank makes a loan, it creates a new deposit. That deposit is money.

Balance Sheet Mechanics: Seeing the Creation in Action

To understand this process fully, we need to look at a bank's balance sheet. A balance sheet is a snapshot of what a bank owns and what it owes. For a bank, the key relationship is that assets equal liabilities plus capital.

Assets are what the bank owns: loans, reserves, government bonds, buildings. Liabilities are what the bank owes: deposits, borrowing from other banks, borrowing from the central bank. Capital is the bank's own equity—the money put in by shareholders plus retained earnings.

Let us look at First National Bank's balance sheet before Maria's loan. For simplicity, suppose it has:

- Reserves: $1,000,000

- Loans: $10,000,000

- Deposits: $11,000,000

The balance sheet balances. Assets of $11,000,000 equal liabilities of $11,000,000.

Now the bank makes the $10,000 loan to Maria. Loans increase by $10,000. Deposits increase by $10,000. The new balance sheet shows:

- Reserves: $1,000,000

- Loans: $10,010,000

- Deposits: $11,010,000

Both sides have expanded. The bank has created $10,000 of new money. This is the moment of creation.

Now Maria spends the $10,000. She writes a check to the equipment supplier, who deposits it in Second National Bank. When the check clears, First National Bank's reserves decrease by $10,000, and its deposits decrease by $10,000. The balance sheet returns to its original size.

But something important has happened. The $10,000 of new money has moved to Second National Bank. Second National Bank's reserves have increased by $10,000, and its deposits have increased by $10,000. The money supply is still larger by $10,000 than before the loan was made. The money has simply moved from one bank to another.

The Life Cycle of Money: Creation, Circulation, and Destruction

There is a symmetry at the heart of money creation that is often overlooked. When a bank issues a loan, it creates new money. When that loan is repaid, the process works in reverse. Money is destroyed.

Creation: When a bank makes a loan, it creates a new deposit. In our example, Maria's $10,000 loan created $10,000 of new money.

Circulation: When Maria spends the money, it circulates through the economy. It becomes a deposit in another bank. That bank can then use it as the basis for new lending, creating even more money.

Destruction: When Maria repays the loan, her deposit decreases by $10,000. The bank's loan asset decreases by $10,000. The money that once existed disappears.

Consider a mortgage. When a bank issues a £300,000 loan to buy a house, it creates a £300,000 deposit. That money enters the economy when the seller receives it. But over the next 25 years, as the borrower makes payments, that money is gradually destroyed. By the time the mortgage is fully repaid, the money that was created at the start no longer exists.

This has a profound implication. Most of the money in the economy is temporary. It exists only as long as loans are outstanding. When new lending exceeds repayments, the money supply grows. When repayments exceed new lending, the money supply contracts.

This is why credit booms fuel economic expansion and why credit slowdowns lead to recessions.

Here is a simple way to see the full sequence:

Loan issued → Deposit created → Money spent → Reserves transferred → Loan repaid → Money destroyed

The Chain Reaction Across Banks

When a bank makes a loan, the money it creates circulates through the economy and becomes deposits in other banks. Those banks can then make new loans, creating even more money. This is a chain reaction.

Let us return to our example. First National Bank made a $10,000 loan to Maria. When Maria spent the money, it became a deposit in Second National Bank. Second National Bank now has a new deposit of $10,000. It must decide what to do with it.

Second National Bank has several options. It could hold the deposit as reserves. It could lend it out. It could buy securities. The decision depends on its assessment of risk, its capital position, and the demand for loans.

If Second National Bank finds a creditworthy borrower, it can make a new loan. When it does, it will create a new deposit. That new money will circulate, become a deposit in Third National Bank, and the process continues.

Each round of lending creates new money. The amounts depend on banks' lending decisions, not on a mechanical formula.

Why Reserves Matter

When a borrower spends a newly created deposit and the payment goes to another bank, the original bank must transfer reserves to settle the transaction. This is where reserves matter. They are not needed to create loans, but they are needed to settle payments after the fact.

The full chain is:

Loan issued → Deposit created → Money spent → Reserves transferred

If a bank needs reserves to settle payments, it can borrow them from other banks or from the central bank. The central bank supplies reserves as needed at its policy rate. This means that in normal times, reserves are not the binding constraint on lending.

However, banks must manage liquidity carefully. If too many payments leave the bank at once, it may face funding pressure. This is why liquidity regulations exist, such as the Liquidity Coverage Ratio (LCR), which requires banks to hold enough high-quality liquid assets to survive a short-term funding shock. While banks can obtain reserves after lending, they cannot ignore the risk of sudden outflows.

Central Banks and Interest Rates

Central banks do not directly control how much banks lend. Instead, they influence lending by setting interest rates. This is the main channel of monetary policy.

When a central bank lowers interest rates, borrowing becomes cheaper. Businesses are more likely to take out loans for investment. Households are more likely to borrow for homes or cars. Banks are more willing to lend because the cost of funding is lower. The result is credit expansion and money creation.

When a central bank raises interest rates, the opposite happens. Borrowing becomes more expensive. Demand for loans falls. Banks become more cautious. Credit slows, and money creation slows with it.

Lower rates encourage credit expansion. Higher rates discourage borrowing and slow money creation. This is how central banks steer the economy without directly commanding banks to lend or not lend.

Capital vs Liquidity: A Crucial Distinction

Two constraints on banks are often confused. Understanding the difference is essential.

Capital is the bank's own equity. It comes from shareholders and retained earnings. Capital acts as a cushion. If loans go bad, the bank's capital absorbs the losses before depositors are affected. Capital limits how much risk a bank can take. This is a solvency constraint.

Liquidity is the bank's ability to meet short-term payment obligations. A bank can be solvent—it has more assets than liabilities—but still face a liquidity crisis if too many payments leave at once and it cannot borrow quickly enough. This is a payment constraint.

A bank can be solvent but illiquid. That was the case for many banks during the 2008 crisis. They had good assets on paper but could not access cash when they needed it. A bank can also be liquid but undercapitalized. It can pay its bills today but will fail when its bad loans eventually come due.

Both constraints matter, but they matter in different ways. Capital requirements are the binding constraint on lending in normal times. Liquidity matters more during sudden crises.

Why Banks Cannot Create Unlimited Money

If banks can create money simply by making loans, why do they not create unlimited money? The answer is that banks face several powerful constraints.

Capital Requirements

The most important constraint in modern banking is capital requirements. Banks are required to hold a certain amount of their own equity relative to the riskiness of their loans. Under the Basel III framework, banks must maintain a minimum capital ratio of around 10.5 percent.

If a bank makes too many loans, it must hold more capital. Raising capital is expensive. This constraint is binding even when reserves are abundant. After the 2008 financial crisis, capital requirements were significantly increased. Today, capital is the binding constraint on lending in normal times.

Demand for Loans

Banks cannot create money if no one wants to borrow. The demand for loans depends on economic conditions, interest rates, and confidence. In a recession, even if banks are willing to lend, businesses may not want to borrow because they do not see opportunities for investment. This is what happened during the 2008 crisis. Banks had plenty of reserves, but demand for loans collapsed.

Interest Rates and Profitability

The interest rate that banks charge on loans affects both their willingness to lend and borrowers' willingness to borrow. If rates are too low, banks may not earn enough profit to cover risks. If rates are too high, borrowers may not want loans. Banks are private businesses. They exist to make a profit. They will not lend if the expected return does not justify the risk.

Regulation and Supervision

Banks operate under extensive regulation. Regulators examine their loan portfolios, capital levels, and risk management practices. If a bank takes excessive risks, it may face fines, restrictions, or even closure. This oversight is a powerful constraint on banks' ability to create money.

Government Deficits as Money Creation

There is one other way money enters the economy that is different from bank lending. When governments spend more than they tax, they inject new deposits into the banking system. Unlike bank lending, which creates both money and private debt, government deficit spending adds deposits to the private sector without requiring households or businesses to borrow.

This is an important nuance. Bank lending creates money, but it also creates a matching liability for the borrower. Government spending creates money without that matching private debt.

Shadow Banking

Not all money-like credit is created by traditional banks. A large shadow banking system has grown alongside traditional banking. Shadow banks include money market funds, hedge funds, and other non-bank financial institutions that create credit outside the traditional deposit system. They played a central role in the 2008 crisis. When Lehman Brothers failed, the panic spread through shadow banking channels that had little regulation and no access to central bank lending.

Understanding shadow banking is essential for understanding modern financial crises, but a full explanation is beyond the scope of this tutorial.

The Thought Experiment: If All Loans Were Repaid

Let us end with a thought experiment. Imagine that, overnight, every bank loan in the economy was repaid. What would happen?

When a loan is repaid, money is destroyed. If every loan were repaid, most of the money in the economy would disappear. The deposits that make up most of the money supply would vanish. However, central bank money—cash and reserves—would remain. Government-issued money and any deposits created through government deficits would also remain. So the money supply would not fall to zero. But it would shrink dramatically.

This is not a hypothetical scenario. It is what happens during severe financial crises, when banks stop lending and borrowers are forced to repay. The money supply contracts. This is why credit slowdowns can lead to deep recessions.

The economy's money supply is not fixed. It is created and destroyed through lending and repayment.

Reference: How Money Is Measured

For readers who want to understand how economists measure the money supply, here is a short guide.

Economists use several measures of money, from the narrowest to the broadest.

M0 is the narrowest measure of money, also called the monetary base. M0 includes physical currency (notes and coins) in circulation plus the reserves that banks hold at the central bank. This is the money that the central bank directly controls. It is sometimes called "high-powered money" because it forms the base upon which the rest of the money supply is built.

A crucial point to understand is that reserves are money that only banks can use—they are not part of everyday spending. When you hear about the central bank "printing money," it often refers to increasing reserves, not printing physical currency. These reserves sit in accounts at the central bank and are used by commercial banks to settle payments with each other and to meet regulatory requirements.

The central bank changes the level of reserves through open market operations—buying or selling government bonds. When the central bank buys bonds, it pays by creating new reserves, which flow into the banking system. When it sells bonds, it removes reserves from the system. This is the primary tool central banks use to influence the money supply.

M1 is the narrow measure of money that is directly usable for transactions. It includes:

- Physical currency (notes and coins) in circulation (the same as in M0)

- Demand deposits—checking accounts from which you can withdraw money immediately

- Other checkable deposits (like NOW accounts) and traveler's checks

M1 is the money that can be spent right now. If you have cash in your wallet or money in your checking account, it is part of M1. In modern economies, M1 is mostly digital—bank deposits, not physical cash.

M2 is a broader measure of money. It includes everything in M1, plus:

- Savings accounts (which are not directly spendable but can be easily converted)

- Money market deposit accounts

- Small-denomination time deposits (certificates of deposit under $100,000)

- Retail money market mutual funds

M2 includes assets that are "near money"—they cannot be spent directly, but they can be quickly converted to cash without significant loss of value. M2 is the measure that most economists watch when thinking about the overall money supply available to households and businesses.

Different measures exist because different forms of money serve different purposes. If you want to know how much people can spend today, you look at M1. If you want to know how much money households have available for spending and saving, you look at M2.

Conclusion

We began with a common misconception: that banks lend out existing deposits. We have seen that the opposite is true. Banks create money when they make loans. They do not need to have deposits first. They create the deposits at the moment of lending. This is how most money in modern economies comes into existence.

We have traced this process step by step, using balance sheets to show how a single loan expands both sides of a bank's accounts. We have followed the life cycle of money from creation to circulation to destruction. We have seen that money is temporary, existing only as long as loans are outstanding. We have explored the real-world constraints that limit money creation: capital requirements, demand for loans, interest rates, and regulation. We have distinguished between capital and liquidity. We have looked at examples from China, the 2008 crisis, and the United Kingdom. And we have acknowledged the role of shadow banking and government deficits.

The creation of money is not a mechanical process. It depends on the confidence of borrowers, the judgment of bankers, the oversight of regulators, and the stability of the financial system. When these elements align, credit expands and the economy grows. When they break down, credit contracts and the economy suffers.

The next time you hear about a bank making a loan, remember that loan created new money. The money did not exist before. It was created in that moment. It is not a transfer of existing wealth. It is the creation of new purchasing power. That power can fuel growth. It can also fuel bubbles. And when lending stops, the money supply can contract rapidly, turning a slowdown into a crisis.

Understanding how banks create money is not just an academic exercise. It is essential for understanding how economies grow, how financial crises happen, and how we might prevent them. The money that powers our economies is not found in vaults. It is created in the moment of lending. It is built on trust, constrained by capital, and managed by central banks.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.