Tutorial Categories

Last Updated: May 7, 2026 at 18:30

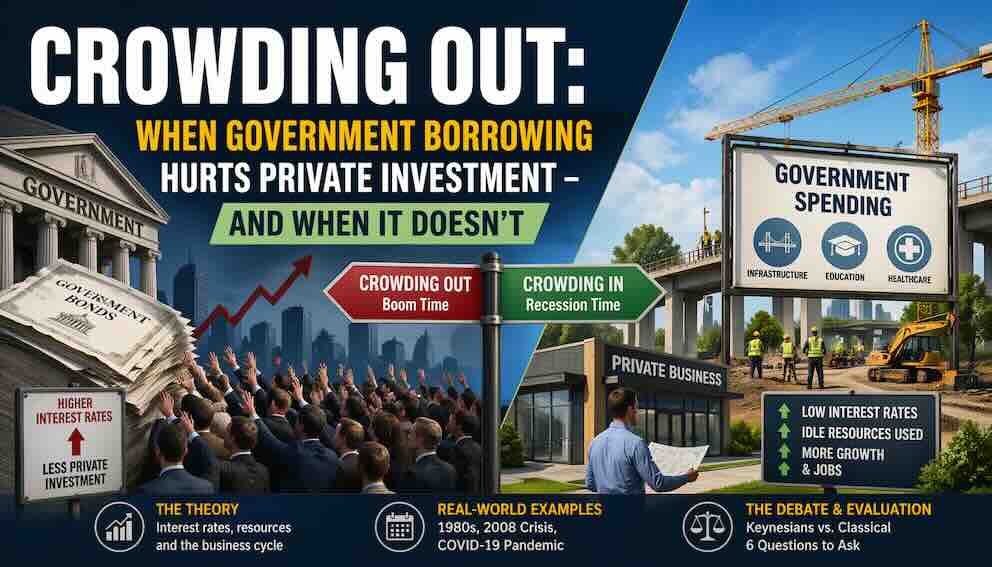

Crowding Out: When Government Borrowing Hurts Private Investment – And When It Doesn't

A Clear Guide to Understanding Why Government Spending Sometimes Fails to Stimulate the Economy

This tutorial explains crowding out, one of the most important criticisms of government borrowing and spending, which occurs when government demand for borrowed money pushes up interest rates, reduces private investment, or causes the currency to appreciate and hurt exports. You will learn the difference between financial crowding out (higher interest rates making loans more expensive for businesses), resource crowding out (the government competing for workers and materials), and exchange rate crowding out (a stronger currency reducing net exports). The tutorial walks you through why crowding out depends critically on what the central bank does – if the bank keeps interest rates low or buys bonds through quantitative easing, crowding out may not happen at all. Using real-world examples from the United States in the early 1980s, the global financial crisis of 2008, and the COVID-19 pandemic, you will understand that crowding out is not a law of nature but a condition that matters in booms and mostly disappears in recessions.

The Core Idea – Why Government Borrowing Might Backfire

Imagine you are the owner of a small manufacturing business that makes furniture. You have been planning to borrow fifty thousand pounds to buy a new computer-controlled cutting machine that would allow you to produce twice as many chairs and tables each week and hire two more workers. You go to your local bank, ready to apply for a loan. But when you sit down with the loan officer, she tells you that interest rates have gone up by two percentage points since you last checked. Your monthly payments would now be much higher than you expected. You do the maths and realise that the new cutting machine would no longer be profitable at these interest rates. You cancel your plans, keep your old equipment, and do not hire those two new workers. The expansion never happens.

What caused your interest rate to rise? The answer might be the government. If the government is running a large budget deficit – spending much more than it collects in taxes – it must borrow the difference by selling government bonds to investors. To attract enough buyers for all those bonds, the government may have to offer a higher interest rate than it would otherwise. As the government borrows more and more, it competes with you and every other business in the country for the limited pool of available savings. The price of borrowing – the interest rate – gets bid up. And when interest rates rise, private investment falls. Businesses postpone buying new machinery, families delay buying new homes, and the overall level of private spending in the economy drops. This is crowding out in a nutshell: government borrowing crowds out private borrowing by pushing up the cost of borrowing for everyone else. The single most important sentence in this entire tutorial is this: crowding out is not about whether government spending works, but about when it works – it matters during economic booms and mostly disappears during deep recessions.

Financial Crowding Out – The Interest Rate Channel

The first and most familiar type of crowding out is financial crowding out, which happens through the interest rate mechanism we just described. When the government borrows money, it increases the total demand for loanable funds in the economy. In any market, when demand rises and supply does not change immediately, the price rises. The price of borrowed money is the interest rate. So government borrowing pushes up interest rates. Higher interest rates make it more expensive for businesses to borrow for investment, more expensive for families to borrow for housing, and more expensive for students to borrow for education. As a result, private investment falls.

Think of the economy as having a certain amount of savings each year – money that households and businesses do not spend on consumption. These savings flow into banks, pension funds, and other financial institutions. That pool of savings is what is available to be borrowed. When the government wants to borrow, it dips into this same pool. If the government borrows heavily, it absorbs a large share of the available savings, leaving less for private borrowers. In a closed economy with no foreign lending, the interest rate must rise until the demand for borrowing from both the government and the private sector matches the available supply of savings. In an open economy like the United Kingdom or the United States, some of the government's borrowing can come from foreign savers, which reduces the upward pressure on interest rates. But even in an open economy, a very large government deficit can still push up interest rates if foreign investors are not willing to lend unlimited amounts.

The classic real-world example of financial crowding out is the United States during the early 1980s, though we must be careful not to oversimplify. President Ronald Reagan enacted large tax cuts and increased military spending, creating very large budget deficits. At the same time, Federal Reserve Chair Paul Volcker was raising interest rates dramatically to break the back of high inflation that had plagued the 1970s. Most economists agree that the Volcker monetary policy was the primary cause of high interest rates in the early 1980s, but the large government deficits almost certainly contributed as well by adding to the demand for borrowed funds. The high interest rates that resulted – the prime rate reached twenty per cent in 1981, meaning that a family with a variable-rate mortgage would have seen their monthly payments double or triple – caused a deep recession and severely reduced private investment in housing, business equipment, and factories. The 1980s teach us that financial crowding out is real, but it is often mixed together with other factors, especially monetary policy.

Resource Crowding Out – Competition for Workers and Materials

The second type of crowding out is resource crowding out, and it works through a completely different channel. Instead of happening in financial markets, resource crowding out happens in the real economy – in labour markets and in markets for raw materials, machinery, and construction supplies. When the government increases its spending, it needs to hire workers and buy things. The government might need to hire construction workers to build a new road, or purchase steel to build a new bridge, or hire nurses to staff a new hospital. If the economy is already operating at or near full employment, those workers and materials are not just sitting around waiting to be used. They are already employed by private businesses. The government must compete for them, and when the government competes for scarce resources, it drives up wages and prices. Private businesses that cannot afford the higher wages or higher material costs cut back on their own spending.

Resource crowding out is easiest to understand with a concrete example. Imagine a small city where there are exactly one hundred construction workers, and they are all already employed building private housing developments. The government announces a new project to build a public library. To get the workers it needs, the government must offer higher wages than the private developers are paying. The construction workers leave the private housing projects to work on the library. The private developers, unable to find workers at their original wage, either raise their own wages (which makes their projects less profitable) or delay their projects. The library gets built, but several private houses do not. The government's spending has crowded out private spending by competing for the same limited pool of workers.

The crucial difference between financial crowding out and resource crowding out is that resource crowding out only happens when the economy is already at or near full employment. If there are unemployed construction workers sitting at home because the private sector is not hiring them, the government can hire them without competing with anyone. Those workers were not being used anyway, so there is no resource crowding out. This is why the state of the economy matters so much. In a deep recession with high unemployment, resource crowding out is not a problem. In a booming economy with full employment, it can be severe.

Exchange Rate Crowding Out – The Hidden Third Channel

Most introductory textbooks stop with financial and resource crowding out. But there is a third channel that matters enormously in the modern global economy, and it is called exchange rate crowding out (or sometimes external crowding out). This channel works through international trade rather than through domestic interest rates or labour markets. Here is how it happens. When a government runs a large deficit and borrows heavily, two things can occur. First, if the government's borrowing pushes up domestic interest rates (financial crowding out), those higher interest rates attract foreign investors who want to earn higher returns. Second, even if interest rates do not rise, large-scale government borrowing from foreign investors directly increases demand for the domestic currency because foreigners need to buy the currency to purchase government bonds. Both of these effects cause the domestic currency to appreciate – to become more expensive relative to foreign currencies.

When a country's currency appreciates, its exports become more expensive for foreign buyers, and imports become cheaper for domestic consumers. As a result, exports tend to fall and imports tend to rise. The net exports component of aggregate demand – which is exports minus imports – decreases. This reduction in net exports offsets some or all of the initial increase in government spending. In an open economy with flexible exchange rates, exchange rate crowding out can be just as important as financial crowding out, and sometimes more important.

The real-world example of exchange rate crowding out is again the United States in the early 1980s. The combination of high interest rates (driven mainly by the Federal Reserve) and large budget deficits (driven by Reagan's tax cuts and military spending) caused the US dollar to appreciate dramatically against other major currencies. Between 1980 and 1985, the dollar rose by about fifty per cent against the German mark and the Japanese yen. This made American manufactured goods very expensive for foreign buyers. US exports collapsed, and imports surged. The trade deficit widened sharply. Many economists believe that the strong dollar caused by the fiscal expansion offset much of the stimulative effect of the tax cuts and spending increases. The lesson is that in an open economy, crowding out can happen not only through higher interest rates but also through a stronger currency that chokes off exports.

The Most Important Factor – What the Central Bank Does

Everything we have discussed so far assumes that the central bank sits on its hands while the government borrows and spends. But in the real world, central banks are active players, and their decisions determine whether crowding out actually happens. This is the single most important insight for understanding crowding out in the modern era. Crowding out is not just a function of how much the government borrows. It is a function of how the central bank responds to that borrowing.

There are three main scenarios to consider. In the first scenario, the central bank accommodates the government's borrowing by keeping interest rates low or by buying government bonds through quantitative easing. When the central bank does this, it essentially provides the savings that the government needs. The government borrows, but the central bank creates new money to buy the bonds, so there is no competition for existing savings. Interest rates do not rise. The exchange rate does not appreciate (or may even depreciate). Financial crowding out is zero, and exchange rate crowding out is minimal. This is exactly what happened during the COVID-19 pandemic. The Federal Reserve, the Bank of England, the European Central Bank, and the Bank of Japan all engaged in massive bond-buying programmes. Governments borrowed trillions, but interest rates remained at historic lows. There was no crowding out because the central banks effectively printed the money to finance the deficits.

In the second scenario, the central bank tightens monetary policy by raising interest rates to fight inflation. This is the opposite of accommodation. When the central bank raises rates, it makes government borrowing even more expensive and directly crowds out private investment. In this scenario, financial crowding out is severe because the central bank is actively pushing up the cost of borrowing for everyone. This is closer to what happened in the early 1980s, although even then the crowding out was primarily driven by monetary policy rather than by the deficit itself.

In the third scenario, the economy is at the zero lower bound – interest rates are already as low as they can go (near zero), and the central bank cannot cut them further. In this situation, which describes most advanced economies after the 2008 financial crisis and during the COVID-19 pandemic, crowding out is approximately zero. The government can borrow without pushing up interest rates because rates are already at their floor, and private borrowing is weak because businesses and households are not confident enough to borrow regardless of the interest rate. This is why almost all economists supported large fiscal stimulus in 2008 and 2020: the conditions for crowding out simply did not exist.

Ricardian Equivalence – The Deeper Critique

Before we move to evaluation, we need to acknowledge one more theoretical critique of fiscal policy that is closely related to crowding out but operates through a completely different mechanism. Ricardian equivalence is the idea, named after the nineteenth-century economist David Ricardo, that government borrowing might not stimulate the economy even if interest rates do not rise and resources are not scarce. The logic is subtle but powerful. When the government borrows money today, it must eventually repay that borrowing with higher taxes in the future. Rational households, according to this theory, understand this. When they see a tax cut today that is financed by borrowing, they do not spend the extra money. Instead, they save it to prepare for the future tax increase. If every household behaves this way, then the tax cut has no effect on consumption, and the government borrowing has no effect on aggregate demand. Fiscal policy is completely ineffective, not because of crowding out in financial markets, but because households anticipate the future tax burden and adjust their saving accordingly.

Most economists do not believe that Ricardian equivalence holds perfectly in the real world. Households are not that far-sighted. Many households are credit-constrained and cannot save even if they want to. And households do not live forever, so they may not care about taxes that will be paid after their death. However, the theory is important because it warns against assuming that all fiscal policy works. If a tax cut is clearly temporary – for example, a one-year reduction in income tax that will expire automatically – households might indeed save most of it because they know taxes will go back up next year. This is why permanent tax changes are usually more effective than temporary ones.

Crowding In – The Opposite Effect

We have spent this entire tutorial talking about how government spending can reduce private spending. But it is only fair to point out that the opposite can also happen. Crowding in occurs when government spending actually increases private investment rather than reducing it. How can this happen? In a deep recession, when the government spends money, it creates demand for goods and services. That demand encourages businesses to invest in new capacity. The government builds a road, and a trucking company buys new trucks to use that road. The government hires unemployed workers, and those workers spend their wages at local shops, encouraging those shop owners to invest in new equipment. Government spending can also improve business confidence. When businesses see that the government is taking action to support the economy, they may become more optimistic about the future and more willing to invest.

The post-2008 recovery in the United States provides some evidence of crowding in. The American Recovery and Reinvestment Act of 2009 included spending on infrastructure, clean energy, and education. While the recovery was slow by historical standards, private investment did eventually return, and many economists argue that the stimulus prevented an even deeper collapse that would have made the subsequent recovery much harder. During the COVID-19 pandemic, the furlough schemes and stimulus payments in countries like the United Kingdom and the United States kept businesses afloat and preserved the connections between workers and firms. When the pandemic eased, private investment recovered quickly because the underlying productive capacity of the economy had been preserved. That is crowding in in action.

A Simple Evaluation Framework

When you read a news story about government borrowing and spending, or when you write an exam essay on fiscal policy, here are the key questions to ask that will help you evaluate whether crowding out is likely to be a problem. First, what is the state of the economy? In a deep recession with high unemployment, crowding out is unlikely. In a booming economy at full employment, crowding out is a serious concern. Second, what is the central bank doing? If the central bank is keeping interest rates low or buying bonds, crowding out is minimal. If the central bank is raising rates to fight inflation, crowding out will be severe. Third, is the economy open to trade and capital flows? If yes, exchange rate crowding out is possible. Fourth, what is the government spending the money on? Spending on infrastructure and education can increase productive capacity and even crowd in private investment. Spending on consumption or inefficient subsidies is more likely to be crowded out. Fifth, what is the time horizon? In the short run, during a recession, crowding out is unlikely. In the long run, if deficits persist through booms, crowding out can accumulate and reduce the economy's capital stock.

Conclusion: Crowding Out Is a Condition, Not a Law

The most important thing to understand about crowding out is that it is not a physical law like gravity. It does not happen automatically every time the government borrows money. It is a conditional phenomenon that depends on the state of the economy, the response of the central bank, the openness of the economy to trade, and the nature of the spending itself. In a deep recession with low interest rates, high unemployment, and an accommodating central bank, crowding out is unlikely to occur, and expansionary fiscal policy can work powerfully to boost aggregate demand. In a booming economy with high interest rates, full employment, and a central bank worried about inflation, crowding out is likely to be severe, and expansionary fiscal policy will mostly just replace private spending with government spending. The evidence tells us that the Keynesians are right about recessions and the classical economists are right about booms. A wise student of economics will carry both perspectives in their toolkit and apply the right one to the situation at hand. Crowding out is not an excuse to never use fiscal policy. It is a reason to use fiscal policy when it is most needed – during recessions – and to rely on other tools, or to run surpluses, during booms. That is the responsible path, and it is the path that the evidence supports.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.