Tutorial Categories

Last Updated: May 7, 2026 at 18:30

Rational Expectations & the Lucas Critique: Why Expectations Changed Macroeconomics Forever

Understanding how forward-looking behavior reshaped economic policy, forecasting, and theory

Why did economists in the 1970s fail to predict rising unemployment and rising inflation at the same time? Because their models ignored how people form expectations. This tutorial explains the concept of rational expectations and how it transformed macroeconomics. It explores why individuals use available information to form accurate forecasts and why this limits the effectiveness of predictable government policies. The discussion walks through the policy ineffectiveness proposition using a clear example. Finally, the Lucas Critique is explained in depth, with a real-world look at the breakdown of the Phillips Curve during the 1970s. By the end, you will understand why modern macroeconomics must explicitly account for expectations rather than rely on historical relationships.

Introduction: The Old Way of Thinking

Before the 1970s, many economists thought about expectations in a simple way. They assumed that people looked at the past and projected it into the future. If inflation had been 2 percent last year, people expected 2 percent this year. If it had been 5 percent, they expected 5 percent. This was called adaptive expectations. It was simple. It was easy to model. And for a while, it seemed to work.

But there was a problem. This way of thinking treated people as passive. It assumed that they never learned, never anticipated, and never adjusted their behavior until after the fact.

In the 1970s, a group of economists led by Robert Lucas argued that this was wrong. They proposed a different view. People are not passive. They actively gather information, understand how the economy works, and form expectations about the future. This view became known as rational expectations.

The shift from adaptive to rational expectations changed macroeconomics forever. It revealed that many old models were fundamentally flawed because they ignored how people respond to policy. It also produced a stunning conclusion: predictable government policies cannot consistently influence the real economy.

This tutorial walks through these ideas step by step, using clear examples and historical events.

A. Core Idea: Rational Expectations

What Does Rational Expectations Mean?

Rational expectations is the idea that individuals in the economy—workers, firms, investors—use all the information available to them, along with an understanding of how the economy operates, to make predictions about the future. These predictions are not random guesses. They are structured attempts to anticipate what will happen given current conditions and policies.

To understand this more concretely, imagine a worker negotiating wages. If the worker expects inflation to rise in the coming year, they will demand higher nominal wages to maintain their purchasing power. This expectation is not formed blindly. It is based on information such as central bank announcements, recent inflation data, and broader economic trends.

This approach assumes that people are not systematically wrong. While they may make mistakes, those mistakes are not biased in one direction over time.

How Expectations Are Formed: Understanding Policy Rules

In rational expectations models, individuals are not simply reacting to outcomes such as inflation or unemployment. They are also forming beliefs about the rules that policymakers follow.

For example, if a central bank tends to raise interest rates when inflation rises, individuals incorporate this behavior into their expectations. They do not just forecast inflation. They forecast how the central bank will respond to inflation, and then how the economy will respond to that response.

This is what economists mean when they say that expectations are model-consistent. People's beliefs about the future align with the structure of the economic system they are operating in. Expectations are formed within the model itself, not outside it.

Forecast Errors: What Makes Them Unpredictable

One of the most important implications of rational expectations is that forecast errors are unavoidable. New information arrives unexpectedly. A storm comes without warning. A supplier goes bankrupt. A competitor launches a surprise product. No amount of cleverness can eliminate these errors entirely.

But under rational expectations, forecast errors are also unpredictable given the information available at the time the forecast was made.

This is a precise idea. It does not mean that forecast errors are "random" in the everyday sense. It means that the error is not correlated with any information that was available when the forecast was made. If it were, the person would have used that information to improve their forecast.

Consider Alan, a taxi driver who has been working the same city for twenty years. Every morning, he decides whether to work the early shift. He checks the weather forecast. He looks up local events. He knows it is a holiday. He considers road closures. He uses everything he can reasonably know.

Most days, Alan is close to correct. But some days he is wrong. A sudden rainstorm might bring out more customers than he expected. A breakdown on the main road might reduce traffic past the station.

Could Alan have predicted these errors using the information he had in the morning? No. He did not know about the rainstorm because the forecast was clear. He did not know about the breakdown because there was no warning. The errors came from new information.

Under rational expectations, forecast errors are not systematically biased. They do not consistently overpredict or underpredict. Across many forecasters or over long periods, the average error is close to zero. This does not mean every person's errors average to zero in every short sample. It means there is no persistent systematic bias.

A Note on Learning

Notice that Alan already forms the best forecast he can. He already knows how rain affects demand. He already knows how holidays change patterns. He incorporates this knowledge from the beginning. This is the rational expectations assumption.

In the real world, people sometimes need time to figure out new relationships. Economists have developed models of adaptive learning to capture this. In those models, agents start with imperfect knowledge and update their beliefs over time. Both approaches are useful, but they are distinct. The rational expectations assumption is stronger: it assumes optimal use of available information from the start.

B. The Policy Ineffectiveness Proposition

The Basic Idea

The policy ineffectiveness proposition builds directly on rational expectations and leads to a striking conclusion. Systematic and predictable economic policies cannot consistently influence real variables such as output or employment.

This seems counterintuitive because governments often use tools like monetary policy to stabilize the economy. But the key insight is that once people anticipate these policies, they adjust their behavior in ways that neutralize their real effects.

Expected vs Unexpected Policy

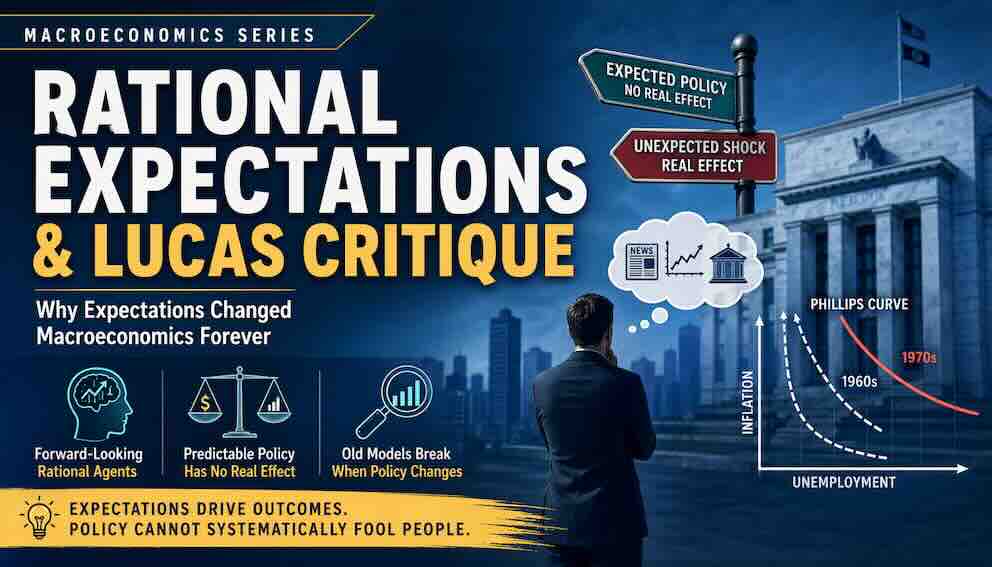

It is useful to think of any policy action as having two parts: the part that people expect and the part that surprises them.

Policy = Expected component + Unexpected component

Under rational expectations, the expected component is already built into wages, prices, and contracts. Workers have already demanded higher wages if they expect inflation. Firms have already adjusted their prices. The expected part of policy has no real effect.

Only the unexpected component can temporarily influence real decisions such as production or employment. This is why predictability reduces the real impact of policy.

A Detailed Example: A Tax Cut

Imagine the government announces a temporary tax cut designed to encourage spending. The policy is widely reported. Newspapers explain it. The central bank confirms it.

Under adaptive expectations, people might respond by spending more. They see the extra money in their paycheck and increase consumption.

Under rational expectations, people ask different questions. Is this tax cut permanent or temporary? Will taxes rise in the future to pay for it? If the government borrows to fund the cut, will interest rates rise?

If people conclude that the tax cut is temporary and that future taxes will increase, they may save the extra money rather than spend it. They anticipate the future. The policy has little effect on current consumption.

Now suppose the tax cut is a surprise. The government announces it the day before it takes effect. People did not see it coming. In this case, some may increase spending because they had not already adjusted their plans.

But here is the catch. A government cannot rely on surprise. Once it has used a surprise tax cut once, people will anticipate that it might happen again. Next time, the element of surprise is gone.

The Inflation Example

Consider monetary policy. Imagine the central bank increases the money supply, which leads to higher inflation.

If this inflation is unexpected, workers and firms may initially misinterpret the situation. Workers might see higher wages and assume that their real purchasing power has increased, even though prices are also rising. As a result, they may be willing to work more, leading to higher employment and output in the short run.

However, this effect depends entirely on surprise. If workers anticipate the inflation, they will demand higher nominal wages beforehand. Firms will adjust their prices accordingly. The increase in inflation does not lead to higher real wages or increased production. Everything adjusts simultaneously, leaving real variables unchanged.

This is the core insight: systematic policy cannot create systematic forecast errors. If the central bank consistently uses inflation to try to boost output, people will recognize this pattern. They will incorporate it into their expectations. The policy will have no systematic effect on real variables.

What Policy Can Still Do

The policy ineffectiveness proposition does not mean policy is powerless. It means systematic, predictable policy cannot systematically fool people. But policy can still have effects in several ways.

First, the unanticipated part of policy can still matter. A surprise interest rate cut can temporarily boost output because it was not expected. But relying on surprise is not a sustainable strategy.

Second, policy can change the structure of the economy. A new regulatory framework or a shift in the central bank's long-term targets can alter how people behave, even if it is announced in advance. For example, a credible commitment to keep inflation low changes expectations about future prices, which affects wage negotiations and investment decisions.

Third, if people are learning rather than already knowing the true model, policy can have effects during the transition period before expectations fully adjust.

This is why modern central banks place great emphasis on credibility and communication. By clearly signaling their future actions, they influence expectations directly. A central bank that is believed when it says it will keep inflation low does not need to surprise anyone. Its credibility does the work.

C. The Lucas Critique

The Problem with Traditional Models

Before rational expectations, many macroeconomic models relied heavily on historical relationships. Economists would observe patterns in the data and use these patterns to guide policy decisions.

This approach assumed that these relationships were stable over time. If higher inflation was associated with lower unemployment in the past, policymakers might attempt to replicate this outcome by increasing inflation.

However, this reasoning overlooked a crucial factor: human behavior changes when policy changes.

The Core Insight

The Lucas Critique argues that economic relationships are not fixed. They depend on how individuals respond to policy. When policy changes, expectations change, and behavior changes with them.

To see why this matters, consider the relationship between inflation and unemployment. If policymakers attempt to exploit this relationship by increasing inflation, individuals will eventually anticipate this strategy. Workers will demand higher wages. Firms will adjust prices. The original relationship disappears.

In other words, the historical pattern breaks down because it was based on a different set of expectations. Once expectations adjust, the economy behaves differently.

A Concrete Example: A Tax Credit for Home Insulation

Imagine a government introduces a temporary tax credit for home insulation. For one year, homeowners who install insulation receive £500 back from the government.

In the first year, many homeowners respond. They install insulation. The policy seems effective.

The next year, the government repeats the policy. But this time, fewer homeowners respond. Why? Because their expectations have changed. They now suspect that the government will keep extending the policy. Some decide to wait. Others realize that the £500 is not a one-time opportunity but a recurring offer. They are no longer rushed to act.

The historical relationship between the tax credit and insulation installation has broken down. Not because the policy changed, but because expectations about the policy changed.

This is the Lucas Critique. The old data from the first year cannot predict behavior in the second year, because people updated their beliefs about what the government would do.

The Phillips Curve: The Classic Example

The most famous application of the Lucas Critique is the Phillips Curve. In the 1960s, economists observed a stable negative relationship between inflation and unemployment in data from the United Kingdom and the United States. When inflation was high, unemployment was low. When inflation was low, unemployment was high.

Many policymakers concluded that they could choose their preferred combination. If they wanted lower unemployment, they could accept higher inflation.

Then the 1970s arrived. Governments tried to exploit the trade-off. They increased inflation. But unemployment did not fall. Instead, both inflation and unemployment rose together. The relationship had broken down.

Why? Because expectations adjusted. Workers and firms realized that higher inflation was not temporary. They built it into their wage demands and price setting. The old relationship, which had been based on a period of stable expectations, disappeared once expectations changed.

This was a devastating blow to the old way of doing economics. It showed that models based solely on historical data were unreliable when policy changed.

Why Expectations Must Be Modeled Explicitly

The Lucas Critique leads to a clear conclusion: macroeconomic models must explicitly incorporate expectations rather than treating them as fixed or secondary.

If expectations are ignored, models may produce misleading predictions because they fail to account for how individuals adapt to new policies. This is particularly important in modern economies, where information is widely available and people can respond quickly to changes.

By incorporating rational expectations, economists can build models that better reflect real-world behavior. These models recognize that individuals are forward-looking and that their decisions depend on what they expect to happen, not just on what has happened in the past.

Real-World Event: The 1970s Stagflation

The 1970s provide the clearest real-world illustration of these ideas. At the beginning of the decade, many economists believed in a stable Phillips Curve. They thought they understood the trade-off between inflation and unemployment.

Then came the oil shocks of 1973 and 1979. Energy prices quadrupled. Inflation soared. Unemployment rose alongside it. By 1975, unemployment in the United States had reached 9 percent, while inflation was above 10 percent. By 1980, inflation exceeded 14 percent, and unemployment was climbing again.

The old models could not explain this. They predicted that high inflation would bring low unemployment. The opposite happened.

Rational expectations offered an explanation. Workers and firms had learned to anticipate inflation. They adjusted their behavior accordingly. The old relationship, which had been based on a period when inflation was low and stable, no longer held.

This episode illustrated the Lucas Critique in practice. The historical relationship that policymakers relied on broke down precisely because their policies changed and people adjusted their expectations.

Conclusion

The development of rational expectations and the Lucas Critique marked a turning point in macroeconomics. They fundamentally changed how economists think about policy and human behavior.

The idea that individuals use available information to form forward-looking expectations means that the economy cannot be easily manipulated through predictable interventions. Systematic policy cannot create systematic forecast errors. Once a policy becomes expected, its real effects disappear.

The Lucas Critique showed that historical relationships are not reliable guides for policy. When policy changes, expectations change, and behavior changes with them. The Phillips Curve of the 1960s disappeared in the 1970s because policymakers tried to exploit it. The tax credit relationship shifted because homeowners updated their beliefs about whether the policy would continue.

These insights force economists to move beyond simple historical patterns and build models that capture how behavior evolves in response to policy changes. Expectations cannot be an afterthought. They must be at the center of the analysis.

Perhaps the deepest lesson is that people are not passive. They watch. They learn. They anticipate. And in doing so, they shape the very world that economists are trying to understand. This is why modern macroeconomics does not ask only what policy does, but what people believe policy will do.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.