Tutorial Categories

Last Updated: May 7, 2026 at 18:30

Adaptive Expectations in Macroeconomics: How People Learn from the Past to Predict the Future

Understanding gradual belief formation, inflation persistence, and short-run policy effects

Why does inflation often stay high long after the original cause has disappeared? The answer lies in how people form expectations. Adaptive expectations describe how individuals and firms learn from past experiences, updating their beliefs gradually rather than instantly. This tutorial explains the mechanics of adaptive expectations, including the simple error-correction rule that drives expectation formation. It explores why inflation tends to persist, why policies can have temporary real effects, and how this framework connects to the expectations-augmented Phillips Curve and the accelerationist hypothesis. Using real-world examples from 1970s Britain, the tutorial shows how gradual learning shapes the economy in ways that are slower, more human, and more realistic than those implied by perfect foresight models.

Introduction: How Do People Form Expectations?

In macroeconomics, expectations about the future play a central role in shaping present decisions. When households decide how much to consume, when firms choose prices or investment levels, or when workers negotiate wages, they are all implicitly making assumptions about what lies ahead. These expectations influence inflation, unemployment, and economic growth.

But how do people actually form these expectations? It is unrealistic to assume that everyone perfectly understands the entire economy or can predict future events with complete accuracy. Instead, people rely on simpler methods based on experience.

One of the most influential frameworks capturing this idea is adaptive expectations. This approach dominated macroeconomic thinking before the rise of rational expectations. It remains important because it captures a realistic feature of human behavior: people learn from their mistakes, but they do so gradually.

This tutorial walks through the mechanics of adaptive expectations, shows how they create inflation persistence, explains the short-run trade-off between inflation and unemployment, and connects the framework to broader macroeconomic concepts such as the expectations-augmented Phillips Curve and the accelerationist hypothesis.

The Core Idea: Learning from Past Mistakes

At its heart, adaptive expectations rest on a straightforward principle: people use past data to form expectations about the future. Instead of analyzing all possible information or constructing complex models, individuals look at what has already happened and assume that the future will resemble the recent past, with an adjustment for what they got wrong.

A helpful way to think about this is through a simple rule of thumb:

"Tomorrow will be similar to yesterday, but with a correction for my last mistake."

Imagine a worker trying to predict inflation for the coming year. If inflation was 4 percent last year, the worker might expect something close to 4 percent again. However, if their previous expectation had been 2 percent, they now recognize that they underestimated inflation. As a result, they revise their expectation upward, but not all the way to 4 percent. They move part of the way.

This process reflects a realistic feature of human behavior. People rarely abandon their previous beliefs entirely. Instead, they update them incrementally, especially when uncertainty is high or when interpreting new information is difficult.

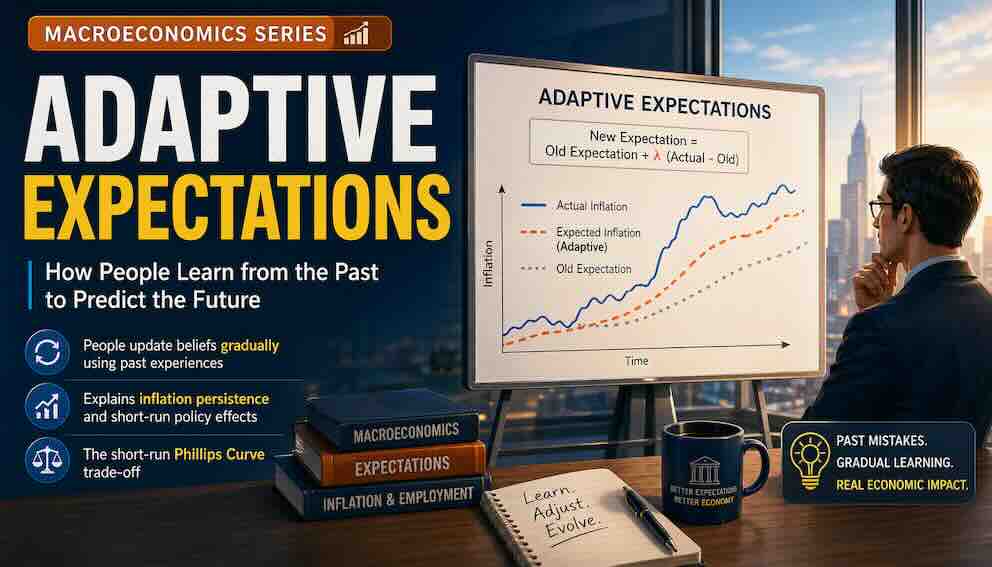

The Mechanism: A Simple Updating Rule

The defining feature of adaptive expectations can be expressed as a simple equation. It is not complicated, and it helps make the idea precise.

Expected inflation today = Expected inflation last period + λ × (Actual inflation last period − Expected inflation last period)

The term in parentheses is the forecast error—the difference between what people expected and what actually happened. The Greek letter λ (lambda) represents the speed of adjustment. It is a number between 0 and 1.

If λ is close to 1, people adjust quickly. They learn from their mistakes almost immediately. If λ is close to 0, people adjust very slowly. They barely change their expectations even when they are wrong.

What determines λ in the real world? Several factors matter. The frequency with which people receive new data affects how quickly they update. Institutional rigidities, such as multi-year wage contracts, slow down adjustment. Access to information also plays a role. A financial trader with real-time data adjusts faster than a worker who reads about inflation once a year.

To see how this works, suppose a firm expected inflation to be 2 percent last year. Actual inflation turned out to be 5 percent. The forecast error is 3 percentage points.

If λ is 0.5, the firm revises its expectation upward by half of the error: 1.5 percentage points. Its new expectation is 3.5 percent, not 5 percent. Next year, if it is wrong again, it will adjust further.

If λ is 0.8, the firm adjusts more quickly. It revises upward by 2.4 percentage points, arriving at an expectation of 4.4 percent.

If λ is 0.2, the firm adjusts very slowly. It revises upward by only 0.6 percentage points, arriving at an expectation of 2.6 percent.

A Deeper Look: Expectations as Weighted Past Inflation

There is another way to think about adaptive expectations that reveals its structure more clearly. The updating rule can be rewritten to show that expected inflation is a weighted average of past inflation rates, with more weight given to recent observations.

Under adaptive expectations, people never fully forget the past. Older inflation data still matter, but they matter less than more recent data. The weights decline gradually as you go further back in time.

This means that if inflation has been high for several years, expectations will eventually rise to match it. But they will never jump instantly. The past lingers. A single year of high inflation moves expectations only part of the way. It takes several years of sustained high inflation for expectations to fully adjust.

This property explains why inflation persistence is so common. Once expectations have adjusted to a high level, they do not fall quickly even if inflation drops. The memory of past high inflation remains.

A Real-Life Example: Wage Negotiations in 1970s Britain

To see adaptive expectations in action, consider wage negotiations between workers and employers in 1970s Britain.

Throughout the 1960s, inflation in the United Kingdom had been relatively low and stable, averaging around 2 to 3 percent. Workers came to expect inflation to remain in that range. They negotiated wage increases accordingly.

Then came the 1970s. Oil prices quadrupled. Inflation soared, reaching over 10 percent by 1974. But workers did not immediately expect 10 percent inflation. Their expectations were anchored in past experience. In the first year of high inflation, they might have expected only 4 or 5 percent.

As a result, their wage demands were too low to keep up with rising prices. Real wages fell. Firms found labor cheaper. Employment remained higher than it would have been if wages had adjusted instantly.

But over time, workers learned. Each year, they revised their expectations upward. By the late 1970s, they were demanding wage increases that anticipated high inflation. The temporary boost to employment faded. Inflation became embedded in expectations.

This is the essence of adaptive expectations. People learn from experience, but they learn slowly. The delay creates room for temporary effects on employment and output.

Connecting to the Phillips Curve

The gradual adjustment of expectations does not just affect inflation itself. It also shapes how inflation interacts with real economic variables such as employment.

In modern macroeconomics, the relationship between inflation and unemployment is captured by the expectations-augmented Phillips Curve. The core idea is simple:

Inflation today depends on expected inflation plus demand pressures in the economy.

When demand is strong, inflation tends to rise above what people expected. When demand is weak, inflation tends to fall below expectations.

Adaptive expectations provide the other half of the story. They explain how expected inflation is formed and how it evolves over time. Expected inflation is not a fixed number. It is constantly being updated based on past forecast errors.

This combination—inflation depends on expectations, and expectations adapt to past inflation—creates the dynamics that economists observed in the 1970s.

The Accelerationist Hypothesis

One of the most important implications of adaptive expectations is the accelerationist hypothesis, associated with the economists Milton Friedman and Edmund Phelps.

The accelerationist idea addresses a simple question: can policymakers keep unemployment permanently below its natural rate by accepting higher inflation?

Under adaptive expectations, the answer is no. Here is why.

Suppose policymakers want to keep unemployment below the natural rate. They use expansionary policy to boost demand. Inflation rises. Initially, workers do not expect this inflation, so real wages fall and unemployment drops.

But workers learn. Over time, they revise their expectations upward. They demand higher wages. Real wages return to their original level. Unemployment returns to its natural rate.

If policymakers want to keep unemployment below the natural rate again, they must raise inflation even higher to create another surprise. Then workers learn again. Inflation must rise further. And further.

The result is accelerating inflation. To keep unemployment below its natural rate, inflation must keep increasing. A constant high inflation rate is not enough. This is why the hypothesis is called "accelerationist."

The 1970s illustrated this pattern. Policymakers tried to exploit the trade-off. Inflation rose. But unemployment did not stay low. Eventually, both inflation and unemployment were high. The accelerationist hypothesis predicted exactly this outcome.

Policy Credibility and Expectation Anchoring

Adaptive expectations have important implications for how policymakers should behave. One of the most important lessons is about credibility.

Under adaptive expectations, people do not instantly trust policy announcements. They wait to see what actually happens. If a central bank announces a lower inflation target, people may not believe it immediately. They have learned from past experience that inflation has been high. They will adjust their expectations only gradually as they observe lower inflation over time.

This creates a challenge for policymakers. It takes time to build credibility. During that transition, policy may have different effects than intended.

This is why modern central banks place great emphasis on inflation targeting and clear communication. By announcing a specific numerical target and demonstrating a commitment to it over time, they hope to anchor expectations. When expectations are well anchored, people believe that inflation will remain low and stable. This belief becomes self-fulfilling. Workers demand moderate wages. Firms set moderate prices. Inflation stays low without requiring constant intervention.

The contrast with adaptive expectations is clear. Under adaptive expectations, expectations are always looking backward. Under well-anchored expectations, they are looking forward at a credible policy target.

Why Adaptive Expectations Feel Realistic

Adaptive expectations are often considered appealing because they align closely with how people behave in everyday life. Individuals rarely have perfect information or the ability to process complex data instantly. Instead, they rely on experience and adjust gradually.

Consider how people form expectations about housing prices. If house prices have been rising steadily for several years, buyers may expect this trend to continue. Even if there are signs of a slowdown, they may not immediately revise their expectations downward. They wait for more evidence. They adjust slowly.

Or consider how drivers learn about a new speed camera. The first time they see it, they might not slow down. After receiving a fine, they adjust. But they might not slow down every time immediately. They learn gradually.

This behavior mirrors the adaptive expectations framework. It captures the idea that people learn over time, rather than making perfect predictions from the outset.

Limitations of Adaptive Expectations

While adaptive expectations provide valuable insights, they have important limitations that eventually led to their replacement by rational expectations in mainstream macroeconomics.

First, adaptive expectations allow systematic forecast errors to persist for long periods. People can be consistently wrong year after year, and the model does not explain why they would not learn to adjust their behavior more quickly. In reality, people eventually notice persistent patterns.

Second, adaptive expectations ignore forward-looking behavior. People do not only look at the past. They read central bank statements. They follow policy debates. They form beliefs about what will happen, not just what has happened. A worker who hears a credible announcement that inflation will fall might adjust expectations without waiting for inflation to actually fall.

Third, adaptive expectations cannot explain rapid shifts in expectations following credible policy changes. When a new central bank governor with a strong anti-inflation reputation takes office, expectations may change quickly. Adaptive expectations, with its slow gradual adjustment, cannot capture this.

Fourth, the framework assumes that the same λ applies regardless of circumstances. But people may adjust faster when the costs of being wrong are high. A financial trader adjusts faster than a worker with a three-year wage contract.

These limitations do not make adaptive expectations useless. They mean that the framework works best in certain contexts: when policy is stable, when information is limited, and when institutional rigidities slow down adjustment. For understanding the 1970s, adaptive expectations are highly relevant. For understanding modern inflation-targeting economies, rational expectations and forward-looking behavior are more appropriate.

Conclusion

Adaptive expectations offer a powerful and intuitive way to understand how people form beliefs about the future in an uncertain world. By focusing on gradual adjustment and learning from past errors, this framework captures an essential feature of real human behavior.

The simple updating rule—new expectation equals old expectation plus a fraction of the last forecast error—provides a clear mechanism for how expectations evolve. The speed of adjustment, represented by λ, determines how quickly people learn. Different parts of the economy can have different speeds, with wages adjusting slowly and financial markets adjusting quickly.

Adaptive expectations explain why inflation often persists long after its original causes have disappeared. They explain why policies can have temporary effects on employment and output. They connect naturally to the expectations-augmented Phillips Curve and lead to the accelerationist hypothesis, which showed that keeping unemployment below its natural rate requires ever-rising inflation.

The framework also highlights the importance of policy credibility. When people do not instantly trust announcements, building a reputation for low inflation takes time. This is why modern central banks emphasize clear inflation targets and transparent communication.

But adaptive expectations are not the final word. They allow systematic forecast errors, ignore forward-looking behavior, and cannot explain rapid shifts in expectations. These limitations led to the development of rational expectations, which assumes that people use all available information efficiently.

Understanding adaptive expectations helps us appreciate why economic adjustments are rarely immediate and why the past continues to influence the present. It reminds us that the economy is not just driven by current conditions, but also by the accumulated experiences and evolving beliefs of the people within it. People learn. But they learn slowly. And that slow learning makes all the difference.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.