Tutorial Categories

Last Updated: June 2, 2026 at 10:30

Labor vs Capital Share in Macroeconomics: Understanding Functional Income Distribution and Its Long-Term Trends

Subtitle: How income is divided between workers and owners of capital—and why it has changed over time

This tutorial explains how economists understand the division of national income between labor and capital, a concept known as functional income distribution. It walks through what labor share and capital share mean in practical terms, using real-world examples such as wages, profits, and business ownership. The discussion then explores how these shares have evolved over time, especially in advanced economies, and what factors have driven these changes. By the end, readers will have a clear understanding of why these trends matter for inequality, growth, and economic policy.

Introduction

Imagine for a moment that a country's entire economic output for a year — every car built, every meal served, every piece of software written, every hospital visit — is gathered into one enormous pile of value. That pile is the national income. Now imagine that this pile must be divided. Some of it will go to people who worked to produce those goods and services. The rest will go to people who own the machines, buildings, patents, and financial assets that made the work possible.

This simple division is what economists call functional income distribution. It is not about whether a particular person is rich or poor. It is about something more structural: how the rewards of production are split, as a whole, between labor and capital.

When we talk about the labor share, we mean the portion of national income that ends up in workers' paychecks — wages, salaries, bonuses, and benefits. When we talk about the capital share, we mean the portion that flows to owners of capital — profits, dividends, interest, and rents.

These two shares always add up to nearly 100 percent of national income (with a tiny remainder for taxes on production). That means if labor's share goes down, capital's share must go up, and vice versa. This tug-of-war matters enormously for how ordinary people live, how investors fare, and how economies grow over decades.

This tutorial will walk through these ideas slowly, with real examples and moments from recent history, so that by the end you will not only know the definitions but also feel why this topic stirs debate among economists and policymakers alike.

A Bakery, a Factory, and a Software Company

To make labor and capital concrete, let us leave abstract formulas aside and visit three small worlds.

First, a neighborhood bakery. The baker wakes up at 4 a.m. to knead dough. A cashier arrives at 6 a.m. to open the shop. These people are providing labor — human effort, skill, and time. The ovens, the mixers, the glass display cases, and the building itself are capital. They are produced goods used to make other goods. At the end of the month, after paying for flour and electricity, the bakery's owner divides the remaining income: wages go to the baker and cashier, and the residual profit goes to the owner as a return on capital.

Second, an auto factory in the 1970s. Thousands of workers on assembly lines install doors, mount engines, and inspect paint jobs. Labor's share of the factory's income is high because so many tasks require human hands and eyes. The owners' capital share is modest but steady.

Third, a modern software company that sells a project management tool. The company has only twenty employees — developers, salespeople, and support staff. But it also owns servers, code libraries, and algorithms that run without human intervention. When a customer pays a monthly subscription, most of that revenue flows to the company as profit after a small payroll cost. Here, capital's share is very high, even though the company does not own heavy machinery.

These three examples show that the labor-capital split is not fixed by nature. It depends on technology, ownership, and the kind of production happening in the economy.

What Functional Income Distribution Really Means

The word "functional" in functional income distribution can seem odd at first. It does not mean "useful" here. It comes from the idea that income is classified according to its function in the production process. Labor income compensates the human factor of production. Capital income rewards the ownership of produced assets.

This way of looking at the world is different from looking at income shares of the richest 10 percent versus the poorest 10 percent. That is personal income distribution. Both matter, but functional distribution asks a prior question: before we worry about exactly who gets what, how is the total pie sliced between the two great factors of production?

For most of the post-World War II period in rich countries, economists observed a surprising stability. The labor share hovered around two-thirds of national income, and the capital share around one-third. This stability was so consistent that the economist Nicholas Kaldor listed it as one of the "stylized facts" of economic growth. Many textbooks treated it almost like a law of gravity.

But gravity, it turned out, had weakened.

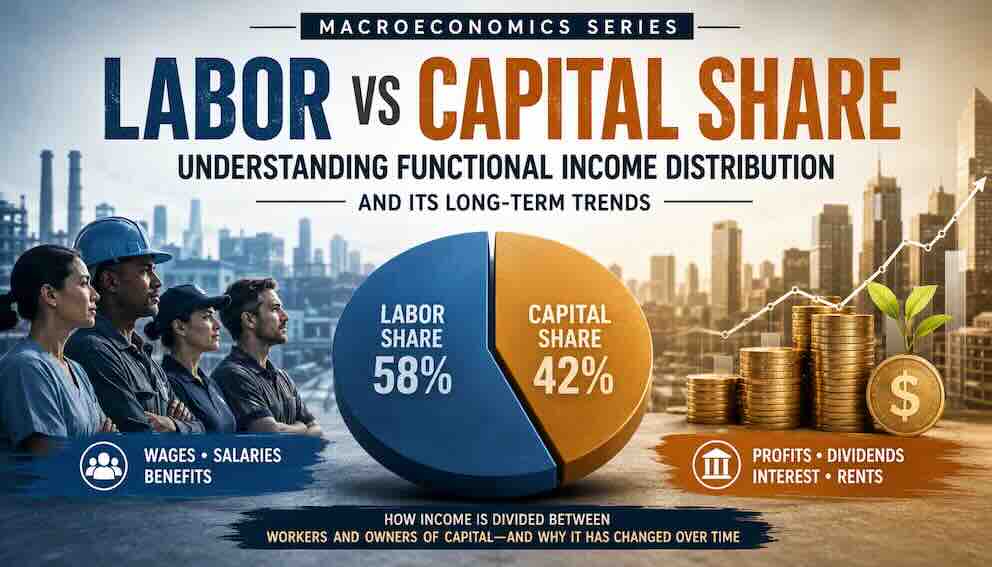

The Great Shift: What Happened After 1980

Beginning around the early 1980s in the United States, the United Kingdom, Germany, Japan, and later many other advanced economies, the labor share began a long, slow decline. By the 2010s, labor's share had fallen from roughly 67 percent to 58 percent or even lower in some countries. Capital's share rose correspondingly — from about 33 percent to 42 percent. That is a substantial reallocation of national income: billions of dollars shifted from paychecks to profits each year.

To feel what this means, consider the life of a typical manufacturing worker in the American Midwest. In 1975, a worker at a General Motors plant could earn a wage that supported a house, a car, and an annual family vacation. The company's profits were healthy, but a large portion of each vehicle's price went to hourly wages. Fast-forward to 2015. That same plant, if it still exists, has far fewer workers. Robots weld and paint. Computerized systems move parts. The remaining workers are more productive than ever, but the share of revenue going to wages is smaller. A larger slice goes to shareholders and executives — capital income.

Perhaps the starkest single piece of evidence for this shift comes from comparing productivity and pay. Between 1979 and 2020 in the United States, output per hour worked — the amount a worker produces in an hour — rose by roughly 60 percent. Over that same period, median hourly wages grew by only about 15 percent in real terms. Workers are producing far more than they did a generation ago, but they are capturing much less of the value they create. The gap between productivity and pay is the clearest possible illustration of a falling labor share.

One real-life event that crystallized this shift was the 2008 financial crisis. In the years after the crisis, corporate profits rebounded quickly in many countries, while wages stagnated for years. From 2009 to 2019 in the United States, real median household income grew slowly, but corporate profits after tax more than doubled. The recovery from the crisis was, in functional distribution terms, a recovery for capital more than for labor.

Another striking example comes from retail. In 2000, Walmart employed over one million workers in the United States, many of them in full-time, in-store roles. By 2020, Walmart still employed many people, but it had also introduced self-checkout kiosks, automated warehouse robots, and an online ordering system that uses far less labor per dollar of sales. Meanwhile, Amazon — a company with a famously high capital intensity — became one of the largest employers in the world, but its profit per employee soared. Consider the contrast within Amazon itself: warehouse workers, who pick and pack orders under intense productivity monitoring, earn wages that have barely kept up with inflation over the last decade, while Amazon's shareholder returns over the same period increased by more than 1,000 percent. That single comparison captures the essence of a rising capital share.

Why Did This Happen? Five Deep Forces

Economists debate the exact causes, but five factors consistently appear in the research. The first three are widely accepted; the fourth and fifth add important nuance.

1. Technology that replaces routine work — and the falling price of capital

Automation does not necessarily destroy all jobs, but it changes which jobs survive. When a robot can weld a car frame more cheaply than a human, the demand for that specific type of labor falls. The owners of the robot — capital — capture the savings.

There is a deeper mechanism here that economists call the elasticity of substitution. In plain English, this means: how easily can a firm replace a worker with a machine? When capital equipment such as robots, computers, and software becomes cheaper — as it has dramatically done over the past four decades — firms will tend to use more capital and less labor. This is exactly what the economists Loukas Karabarbounis and Brent Neiman found in a landmark study: the falling price of investment goods (like machinery and information technology) explains roughly half of the global decline in the labor share. The cheaper capital becomes, the more firms substitute it for workers, and the more income flows to capital owners.

2. Globalization and the movement of production

When a company can produce goods in Vietnam or Mexico and sell them in Germany or Canada, workers in high-wage countries face new competition. This competition does not always lower wages across the board, but it tends to reduce labor's bargaining power. A vivid real-life moment was the 1994 North American Free Trade Agreement (NAFTA). In the years after NAFTA, many US and Canadian manufacturing firms threatened to move production to Mexico unless workers accepted slower wage growth. Whether or not they actually moved, the threat alone shifted the balance toward capital.

3. The weakening of labor institutions and bargaining power

In the mid-1950s, about one in three American workers belonged to a union. By 2020, that number had fallen to one in ten. Unions bargain for higher wages and a larger labor share. Their decline, partly driven by political changes and partly by shifts in industry structure, removed a counterweight to capital's rising influence. A telling event was the 1981 firing of striking air traffic controllers by President Reagan. Many labor historians mark that moment as a turning point in employer militancy and union decline.

4. The rise of superstar firms

The economists David Autor, David Dorn, Lawrence Katz, Christina Patterson, and John Van Reenen have documented a powerful mechanism: in many industries, a small number of highly profitable, capital-intensive firms have come to dominate the market. Think of Google in search, Amazon in e-commerce, or Deere in farm equipment. These superstar firms have very high profits relative to their sales, meaning a larger share of their revenue flows to capital. As they capture more market share, the aggregate labor share falls — even if nothing changes within the other, smaller firms.

This insight is important because it shows that the labor share can decline without every firm changing its behavior. It is a structural shift toward an economy dominated by a few extraordinarily profitable giants.

5. The rise of intangible capital

Traditional capital was physical: factories, machines, trucks. Modern capital increasingly includes intangible assets: patents, software, algorithms, brand value, and data. These intangibles have two features that boost capital's share. First, they often have very low marginal costs — once a software program is written, the cost of producing another copy is near zero, meaning most of each additional sale becomes profit. Second, intangible assets tend to be concentrated in the hands of a few firms, reinforcing the superstar effect.

A Necessary Measurement Caveat: The Self-Employment Problem

Before continuing, it is worth acknowledging a subtlety that economists debate. National income accounts include income from self-employed people — farmers, shopkeepers, freelance designers, gig workers. For these individuals, income is a mix of labor and capital returns. A self‑employed electrician earns a return on their tools (capital) and on their skill and time (labor). But standard accounting lumps this together as "mixed income." This makes it harder to measure the pure labor share precisely.

The growth of the gig economy — Uber drivers, DoorDash couriers, TaskRabbit handypeople — has made this measurement problem more relevant, not less. Many gig workers are technically self-employed, so their income is recorded as mixed. Yet in practical terms, much of it functions like wages. Economists have developed methods to impute the labor component, but the existence of the problem is worth remembering. The broad trends described in this tutorial — the long decline in labor's share — hold up even after adjusting for self-employment, but the exact numbers vary depending on the method used.

Not Every Country or Sector Follows the Same Path

It would be wrong to say that labor share is falling everywhere, all the time. Cross-country variation tells a more interesting story.

Consider Germany. Between the 1980s and early 2000s, Germany's labor share fell, much like in other advanced economies. But starting in the mid-2000s, it partially recovered. Why? Germany has a distinctive system of labor relations called co-determination: workers elect representatives to corporate supervisory boards, and works councils have legally protected rights over issues like working hours and pay scales. These institutions gave workers a voice even as unions declined nationally. The German recovery of labor share suggests that institutional design matters — the decline is not inevitable.

In developing countries like China, labor share fell sharply from the 1990s to the 2010s as millions moved from farming to factories, but capital's share rose because of high profits and low wages. More recently, China's labor share has begun to inch upward as wages catch up and the government emphasizes domestic consumption.

Within a single country, different industries tell different stories. In technology and finance, capital's share is very high. In hospitality and health care, labor's share remains high because those activities still rely heavily on human interaction. A nurse, a hotel housekeeper, or a restaurant server cannot easily be replaced by a machine or a line of code — at least not yet.

This unevenness means that when you hear "the labor share is falling," it is worth asking: whose labor? A skilled software engineer has seen their labor share hold up or even rise. A worker with a high school diploma in a routine manufacturing job has seen their share fall. Functional income distribution hides these differences, which is why it must be complemented by personal distribution analysis.

Who Within Labor Has Been Most Affected?

The decline in labor's share has not been distributed evenly among workers. Women and Black, Hispanic, and other minority workers have disproportionately borne the wage stagnation. This is not an accident of the data — it reflects the fact that routine, less-automated service jobs, where bargaining power is weakest, are also jobs held disproportionately by women and people of color.

For example, in the United States between 1980 and 2020, real hourly wages for white men with a high school degree fell modestly but remained relatively stable at the median. For Black women with the same education, real wages fell significantly in percentage terms, and they started from a lower base. The gap between the productivity-pay divergence and actual living standards is widest for these groups. This connects directly to the wealth inequality tutorial in this series: a falling labor share is one mechanism that generates racial and gender wealth gaps over time.

Why Should You Care? Three Real-World Consequences

1. Inequality and the r > g dynamic

Capital ownership is far more concentrated than labor income. In most countries, the richest 10 percent own the vast majority of stocks, bonds, and real estate. When capital's share rises, most of those extra profits flow to people who are already wealthy. This widens the gap between the top and the middle. The Occupy Wall Street movement's slogan — "We are the 99 percent" — was, in economic terms, a cry about the rising capital share.

This connects directly to Thomas Piketty's famous argument, explored in the wealth inequality tutorial of this series. Piketty's central formula — r > g, meaning the rate of return on capital exceeds the economic growth rate — depends on a rising capital share. If capital's share had remained stable at one‑third, r > g would be less consequential. But a rising capital share means that more of the economy's income flows to capital, and if r > g, that capital accumulates faster than the rest of the economy grows. The two ideas reinforce each other.

2. Spending power and secular stagnation

Workers tend to spend nearly all of what they earn on consumption — rent, groceries, school supplies. Capital owners save a larger fraction. If the capital share rises too much, total consumption demand may weaken, leading to slower growth and even recessions.

The economist Larry Summers and others have revived the concept of secular stagnation — a persistent shortfall in aggregate demand that keeps economies operating below potential. Summers argues that the rising capital share is a key driver: as income shifts from high-spending workers to high-saving capital owners, the economy needs ever-lower interest rates or ever-higher government spending to maintain full employment. This explains why many advanced economies have struggled with low inflation and low growth since 2008 despite very loose monetary policy.

Some economists argue that the 2008 crisis itself was preceded by a long rise in inequality and capital share, which forced middle- and low-income families to borrow heavily to maintain their living standards. When the borrowing stopped, the economy collapsed. This is not a fringe view; it was central to the research of economists like Raghuram Rajan and Atif Mian.

3. Politics and policy

Governments notice when wages stagnate. In recent years, many US states have raised minimum wages. France and Germany have experimented with kurzarbeit (short-time work subsidies) to protect wages during downturns. Some economists have proposed a "robot tax" or broadening capital ownership through worker stock ownership plans.

What does the evidence say on these policies? Minimum wage increases, in careful studies (such as by David Card and Alan Krueger), do not lead to the job losses that critics once predicted; they genuinely raise wages at the bottom and modestly increase labor's share. Kurzarbeit in Germany appears to have saved jobs during the 2008 recession without permanently reducing labor's share. Robot taxes are more speculative — no large country has implemented one — and critics worry they would slow innovation. Worker stock ownership plans, like those common in Germany or in US employee-owned firms (e.g., Publix supermarkets), do shift some capital income to workers, but they have not been large enough to reverse aggregate trends. The policy toolkit exists, but its use has been limited.

These policy ideas only make sense if you first understand functional income distribution. Without that lens, you might think the only issue is whether specific people are poor. With it, you see that the very structure of production shapes who gets what.

Conclusion

Let us return to that pile of national income we imagined at the beginning. For most of the twentieth century, in most rich countries, the division was surprisingly steady: about two shares for labor, one share for capital. That stability made it easy to forget that the split could ever change. But starting in the 1980s, it did change. Labor's share fell from roughly 67 percent to 58 percent; capital's share rose from 33 percent to 42 percent. In a large economy, that nine-percentage-point shift represents hundreds of billions of dollars moving from paychecks to profits every single year.

This is not a tale of good versus evil. Robots can make cars safer and cheaper. Global trade has lifted billions out of poverty. Shareholders include pension funds that pay for retirees' groceries. But the shift matters — for the factory worker who now competes with a machine, for the nurse whose wage grows more slowly than hospital profits, for the young person wondering if hard work still offers the same rewards it did for their parents' generation.

Now return to the bakery from the opening example. Imagine that over the next twenty years, the bakery's owners install automated dough-mixers, self-checkout kiosks, and algorithmic scheduling software. The baker and cashier work just as hard, but the share of each loaf's price that goes into their paychecks shrinks. The machines' owners get more. The baker does not work less hard; the bakery does not produce worse bread. But the division of the income changes. That is the labor share in miniature — a quiet, powerful shift that accumulates over decades into a different kind of economy altogether.

This tutorial sits at the intersection of several ideas explored elsewhere in this series. The Solow model showed how capital accumulation drives aggregate growth — this tutorial shows how that capital captures a growing share of what it produces. The wealth inequality tutorial explained why wealth concentrates at the top — a rising capital share is a core mechanism behind that concentration. In upcoming tutorials on secular stagnation and financialisation, we will see how a persistently high capital share suppresses demand and reshapes the entire macroeconomic landscape.

Understanding labor share and capital share will not tell you everything about the economy. But it will tell you something essential: how the fruits of production are divided before any government taxes or spends, before any charity gives or receives. That division is not determined by nature or by anonymous forces. It is shaped by technology, by laws, by bargaining power, and by politics. And because it is shaped by human choices, it can be reshaped. The baker, the auto worker, and the software developer all have a stake in how that reshaping goes.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.