Tutorial Categories

Last Updated: June 2, 2026 at 10:30

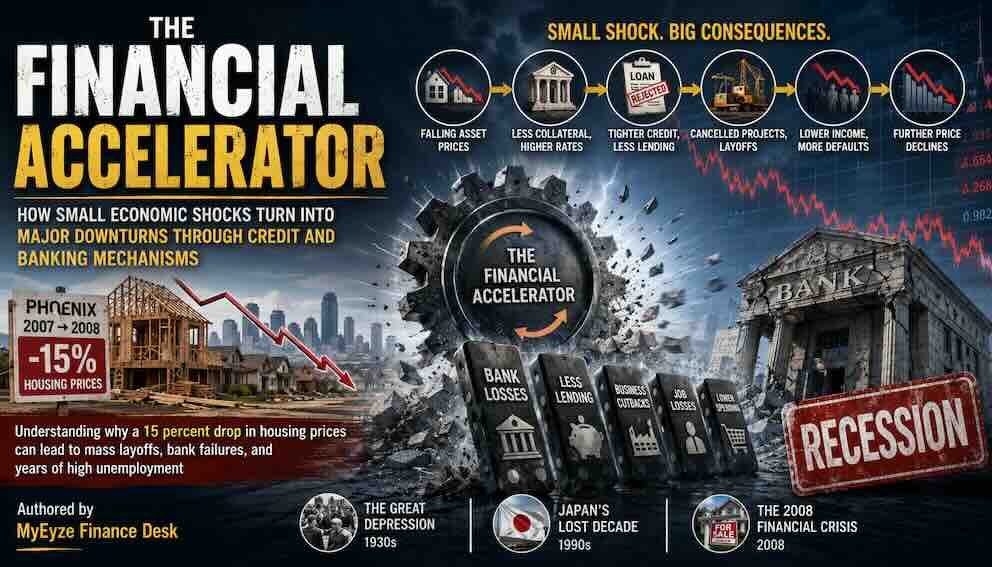

The Financial Accelerator: How Small Economic Shocks Turn Into Major Downturns Through Credit and Banking Mechanisms

Subtitle: Understanding why a 15 percent drop in housing prices can lead to mass layoffs, bank failures, and years of high unemployment

This tutorial explains the financial accelerator, a concept developed by Ben Bernanke, Mark Gertler, and Simon Gilchrist that shows how financial markets can turn small economic disturbances into large, prolonged recessions. The core insight is that falling asset prices reduce the value of collateral that businesses use to borrow, which raises the cost of credit and forces banks to cut lending, which then forces firms to cancel projects and lay off workers, which pushes asset prices down further. Using real-world examples including the 2008 financial crisis, the Great Depression, and Japan's Lost Decade, the tutorial walks through the main amplification channels: the collateral channel, the bank capital channel, and the uncertainty channel. By the end, readers will understand why central banks intervene during financial crises, what tradeoffs those interventions entail, and why financial stability matters for ordinary households.

A Construction Firm in Phoenix, 2007 to 2008

Let us begin with a single business in a single city, because big economic ideas often become clearer when we watch them play out in a small, concrete setting.

In the spring of 2007, a mid-sized construction firm in Phoenix, Arizona is doing reasonably well. The firm builds single-family homes in the sprawling suburbs that have been growing rapidly for years. Like most construction firms, this company does not pay for its projects entirely out of its own cash. Instead, it borrows money from a regional bank, using its existing assets as collateral. Those assets include the land it already owns, the heavy equipment it operates, and the partially completed homes it is building. The bank feels comfortable lending because if the firm cannot repay, the bank can seize the land and the equipment and sell them to recover its money.

Because the firm can borrow against this collateral, it plans three new housing developments for the coming year. It hires forty additional workers. It signs contracts with suppliers for lumber, concrete, and plumbing fixtures. The local economy hums along.

Then, in late 2007 and early 2008, housing prices begin to fall. At first, the fall seems modest — just a few percentage points. But by the summer of 2008, home prices in Phoenix have dropped about 15 percent from their peak. The land that the construction firm owns is now worth 15 percent less. The bank revalues the firm's collateral and reaches a troubling conclusion: the firm no longer has enough assets to justify its existing credit line, let alone any new loans. The bank cuts the credit line sharply.

Now watch what happens next, because this is the heart of the financial accelerator.

The firm cannot borrow the money it needs to finish the projects it already started. It cancels the three new developments. It lays off most of the forty workers it recently hired. It stops buying lumber and concrete from its suppliers. Those suppliers, suddenly missing a major customer, lay off some of their own workers. The laid-off workers stop spending money at local restaurants and retail stores. Those businesses see their sales fall and consider their own layoffs. Meanwhile, because so many people have lost income or fear losing their jobs, even fewer families can afford to buy homes. Housing prices fall further.

Here is the crucial observation: nothing fundamental changed about this construction firm's ability to build houses. The same workers with the same skills, the same equipment, the same blueprints, and the same undeveloped land were perfectly capable of building the same homes. But a purely financial mechanism — the link between collateral values and borrowing capacity — turned a moderate 15 percent price decline into a cascade of cancelled projects, lost jobs, and falling incomes that spread far beyond the housing market.

This mechanism is what economists call the financial accelerator. Here is a roadmap of where we are going. First, we will define the financial accelerator formally, introducing the external finance premium and the information problem that makes collateral so important. Second, we will walk through the three main amplification channels. Third, we will examine historical evidence from the Great Depression, Japan's Lost Decade, and the 2008 crisis. Fourth, we will discuss policy implications and tradeoffs. Finally, we will close with a conclusion that ties everything together.

What Is the Financial Accelerator?

In the 1990s, three economists — Ben Bernanke (who later became the chair of the US Federal Reserve), Mark Gertler, and Simon Gilchrist — developed a formal model to explain something that standard economic models had trouble capturing. Standard models tended to treat financial markets as a kind of neutral veil that simply channeled savings into investment without changing the fundamental behavior of the economy. Bernanke, Gertler, and Gilchrist argued instead that financial markets contain their own internal dynamics that can take a small initial shock and turn it into something much larger and longer lasting. They called this phenomenon the financial accelerator.

The External Finance Premium

The core insight of the financial accelerator is that borrowing capacity and borrowing costs depend on the value of collateral, and collateral values depend on economic conditions. When times are good, asset prices rise. Firms see their collateral increase in value. Banks are willing to lend more, and at lower interest rates. Firms use that cheap credit to expand, pushing asset prices even higher.

When times turn bad, the opposite happens. Asset prices fall. Collateral shrinks. Banks respond in two ways: they cut the quantity of credit, and they raise the price of the credit they do extend. Even if a firm can still borrow, it now faces higher interest rates.

Economists call this increase in borrowing costs the external finance premium — the extra cost a firm pays to borrow from outside lenders compared to using its own internal funds. When a firm has high net worth and plenty of collateral, the external finance premium is low. When net worth falls and collateral shrinks, the premium rises. This rising premium makes many otherwise profitable projects no longer worth undertaking. A construction firm that would have borrowed at 6 percent to build a project with an expected return of 8 percent might find that the same loan now costs 9 percent. The project is cancelled not because credit disappeared entirely, but because it became too expensive.

Why Collateral Matters: Information and Enforcement

Why does collateral matter so much in the first place? The answer has to do with two features of real-world lending that are absent from idealized economic models: asymmetric information and limited enforcement.

Lenders do not know everything about the borrowers they lend to. A bank cannot perfectly observe whether a construction firm is working hard, taking prudent risks, or quietly shifting money to risky ventures. This is asymmetric information — the borrower knows more about its own behavior than the lender does. In addition, lenders cannot always force borrowers to repay. If a borrower simply refuses to pay, the lender must go to court, seize assets, and sell them, which is costly and time-consuming.

Collateral solves both problems at once. By pledging an asset as collateral, the borrower gives the lender a way to recover losses if things go wrong. This reduces the lender's need to monitor the borrower perfectly, and it gives the borrower a strong incentive to avoid default because default means losing the asset. When collateral values fall, this solution breaks down. The lender can no longer rely on the collateral to cover potential losses, so the information problems become severe again. Lenders respond by raising rates, tightening terms, or refusing to lend entirely.

Pro-cyclical Credit

The financial accelerator produces what economists call pro-cyclical credit — credit moves in the same direction as the overall economy, amplifying booms and deepening busts. What would actually stabilize the economy would be countercyclical credit: banks lending more during downturns to offset the weakness, and lending less during booms to prevent overheating. But the financial accelerator pushes credit in exactly the opposite direction.

Section summary: The financial accelerator describes how falling asset prices raise the external finance premium — the extra cost of external borrowing — through the collateral channel. This happens because collateral reduces information problems between lenders and borrowers, and when collateral falls, those information problems get worse, driving up borrowing costs and reducing credit availability.

Credit Amplification Mechanisms

The financial accelerator operates through several specific channels that reinforce one another. This section covers the three classic channels and then adds a fourth involving household balance sheets.

The Collateral Channel

The collateral channel is the simplest and most direct mechanism, and it is exactly what we saw with the Phoenix construction firm. When a business borrows money, it pledges assets as collateral. When asset prices fall, the bank recalculates the borrower's net worth. If net worth falls too low, the bank raises interest rates, shortens loan maturities, or cuts off credit entirely. The borrower cancels projects, lays off workers, and cuts spending. Those actions lower asset prices further, reducing collateral values for other borrowers, and the cycle continues.

The Bank Capital Channel

The collateral channel affects individual borrowers directly. But the financial accelerator also spreads through the banking system itself, infecting healthy borrowers far from the original shock.

Banks have capital — money put in by owners or retained from past profits — that acts as a cushion against losses. When a bank suffers losses, its capital shrinks, and it must reduce lending. In a downturn, many banks suffer losses at the same time. As bank capital falls across the system, every bank curtails lending to every borrower, not just the troubled ones. A healthy manufacturing firm in Ohio that never made a single housing loan suddenly finds its credit line reduced, not because the firm did anything wrong, but because its bank lost capital on real estate loans in Florida.

The Uncertainty Channel

When the economy enters a downturn, lenders face a difficult problem. They cannot easily tell which borrowers will remain healthy and which will fail. In normal times, lenders gather information and make reasonably accurate judgments. But in a severe downturn, the usual signals become unreliable.

Faced with this uncertainty, lenders often respond by restricting credit to almost everyone. They raise lending standards, demand more collateral, and reject loan applications from firms that would have been approved in normal times. This behavior is rational for each individual lender, but collectively it starves good firms of credit alongside failing ones. A well-managed firm gets starved of credit not because it is poorly managed, but because the lender cannot distinguish it from a failing firm.

The Household Balance Sheet Channel

The three channels above focus on firms and banks. But modern economies are also highly sensitive to the balance sheets of households, and this channel was central to the 2008 recession.

When housing prices fall, homeowners lose equity in their homes. A family that bought a house for $300,000 with a $30,000 down payment and a $270,000 mortgage might see the house's value fall to $250,000, leaving them with negative equity. Even if not in negative equity, their wealth has fallen substantially. Families that feel poorer spend less on consumption. In addition, many families borrow against home equity to finance spending. When home equity falls, this borrowing capacity disappears. Reduced consumption by households then reduces business revenues, leading to layoffs, which further reduces household income and leads to more defaults.

Section summary: The financial accelerator operates through four main channels. The collateral channel reduces borrowing capacity for firms. The bank capital channel spreads losses through the banking system. The uncertainty channel makes lenders cautious across the board. The household balance sheet channel reduces consumption and borrowing by families. These channels work together, each reinforcing the others.

Historical Evidence

The financial accelerator has played a central role in several major economic episodes. Before examining them, it is worth noting that the accelerator operates differently depending on how an economy is financed. In bank-based economies like Germany and Japan, the bank capital channel dominates. In market-based economies like the United States and the United Kingdom, the collateral channel operating through securities markets is equally important. This distinction explains why the 2008 crisis hit the US and UK harder through securities markets while Japan's crisis operated primarily through bank balance sheets.

The Great Depression

Ben Bernanke, before he became Federal Reserve chair, was a leading scholar of the Great Depression. In a famous paper published in 1983, he argued that the wave of bank failures between 1930 and 1933 transformed what might have been a severe but ordinary downturn into the deepest economic catastrophe in modern history.

More than 9,000 American banks failed in those years. Each bank failure destroyed credit relationships built over many years. A small business that had borrowed from a local bank for a decade suddenly found itself without access to credit. Even if another bank survived in the same town, that new bank did not know the business and was not willing to extend credit without a lengthy evaluation. Viable businesses could not borrow, laid off workers, and often failed themselves. The process of rebuilding credit relationships took years, which explains why the Depression lasted so long.

Japan's Lost Decade

Japan in the 1990s provides a different illustration. Japanese banks had made enormous loans during the bubble years of the 1980s. When the bubble burst, asset prices collapsed, and borrowers could not repay. Losses reduced Japanese bank capital substantially. Rather than write off the bad loans and recognize the losses, Japanese regulators and banks chose a different path. They continued lending to the same troubled borrowers, allowing them to make interest payments using new loans — a practice called evergreening.

These borrowers became zombie firms — economically unviable but kept alive by bank credit. Every yen lent to a zombie firm could not be lent to a healthy, growing firm. Credit was systematically misallocated toward failing companies and away from successful ones. The result was a decade of slow growth and falling asset prices. The financial accelerator operated not through a sudden crash in lending, but through a persistent misallocation of credit.

The 2008 Financial Crisis

The most vivid modern example is the 2008 crisis. The initial shock was a decline in US housing prices. This reduced the value of mortgage-backed securities. Banks and financial institutions had borrowed heavily to buy these securities, using the securities as collateral. When the securities lost value, collateral evaporated.

The failure of Lehman Brothers in September 2008 triggered the bank capital channel globally. Every major bank had lent to or traded with Lehman. The interbank lending market froze completely because no bank trusted that any other bank would survive — a pure example of the uncertainty channel. With the interbank market frozen, banks slashed lending to all borrowers: homebuyers, construction firms, manufacturers, and families. The household balance sheet channel amplified the downturn as families could not borrow against home equity, could not get auto loans, and could not refinance mortgages. Consumption fell sharply. The financial accelerator had turned a housing downturn into the deepest global recession since the 1930s.

Section summary: The Great Depression shows how destroyed credit relationships prolong downturns. Japan's Lost Decade shows how undercapitalized banks misallocate credit to zombies for years. The 2008 crisis shows how all four channels working together can transform a housing downturn into a global recession.

Why This Matters for Policy

The Case for Intervention

Standard economic models that ignore financial frictions often conclude that policymakers should not intervene in financial markets. Falling asset prices simply reflect new information. Banks that made bad loans should suffer the consequences. Intervening creates moral hazard — the incentive to take excessive risks because losses will be socialized.

But if the financial accelerator is correct, this view is incomplete. Falling asset prices cause further economic damage through the channels described above. A bank that loses money is a node in a credit network, and its failure can choke off credit to healthy firms and families. Breaking the feedback loop can prevent enormous economic damage.

The Federal Reserve, then chaired by Bernanke, took unprecedented steps in 2008. It cut interest rates to near zero. It created emergency lending facilities to provide credit directly to financial institutions that could not borrow in the frozen interbank market. It purchased massive quantities of mortgage-backed securities and government bonds — quantitative easing — to support asset prices and push down long-term interest rates. The goal was to short-circuit the financial accelerator by replacing frozen private markets, supporting collateral values, and reducing uncertainty.

Tradeoffs and Risks

Intervening to stabilize credit markets carries significant risks. The most frequently cited is moral hazard. If financial institutions believe the government will rescue them whenever they get into trouble, they have an incentive to take excessive risks.

A second risk is zombie lending, which we saw in Japan. If policymakers prop up insolvent banks rather than forcing them to recognize losses, those banks may continue lending to failing firms, crowding out productive lending.

A third risk is asset price distortion. When central banks purchase large quantities of assets, they push up prices. This supports collateral values, which is precisely the goal. But it also means that asset prices may no longer reflect fundamental values. Investors may come to rely on central bank support as a permanent feature of markets — the expectation, known as the central bank put, that the central bank will always step in when asset prices fall.

A Balanced View

The evidence from 2008 suggests that aggressive intervention prevented a second Great Depression. But the interventions also created moral hazard, distorted asset prices, and generated political backlash. The lesson is not that intervention is always right or always wrong. The lesson is that financial systems require careful regulation in normal times so that extreme interventions are needed less often. Higher capital requirements, stress tests, and countercyclical lending rules are all designed to limit the financial accelerator before it can gain momentum.

Section summary: The financial accelerator justifies central bank intervention during crises, but intervention carries tradeoffs: moral hazard, zombie lending, and asset price distortion. The best policy combines crisis intervention with long-term regulation that reduces the financial accelerator's power in the first place.

The Run on Northern Rock

The run on Northern Rock in September 2007 shows how quickly the financial accelerator moves from theory to reality. Northern Rock was a British bank that funded mortgages with short-term wholesale borrowing rather than customer deposits. On September 13, 2007, it announced it had received emergency funding from the Bank of England because it could not roll over its short-term debt. The next morning, depositors lined up outside branches to withdraw their savings — the first bank run in Britain in nearly 150 years.

What caused the run? Not a fundamental change in Northern Rock's mortgage portfolio, which was performing reasonably well. The problem was that Northern Rock's lenders had become uncertain about the value of its collateral and about its ability to repay. This is the uncertainty channel. Lenders could not distinguish between a solvent bank with a temporary liquidity problem and an insolvent bank that would never repay, so they refused to lend. The freezing of Northern Rock's credit caused its collapse, foreshadowing the global crisis to come.

Conclusion

Let us return one final time to the construction firm in Phoenix. A 15 percent drop in housing prices reduced the firm's collateral, which raised the external finance premium on its borrowing, which caused its bank to cut its credit line, which forced the firm to cancel projects and lay off workers, which reduced incomes and spending, which pushed housing prices down further. The initial shock was modest, but the financial mechanism turned it into something much larger.

The financial accelerator teaches us that credit markets are not neutral conduits for savings. They have their own internal dynamics that amplify and propagate economic disturbances. The collateral channel, the bank capital channel, the uncertainty channel, and the household balance sheet channel work together to transform small shocks into large, prolonged downturns. The Great Depression, Japan's Lost Decade, and the 2008 financial crisis each illustrate this mechanism in different ways, with the relative importance of each channel depending on whether an economy is bank-based or market-based.

This understanding has changed how economists think about financial crises and how policymakers respond to them. Breaking the feedback loop — supporting collateral values, providing emergency credit, reducing uncertainty — can prevent enormous economic damage. But intervention is not free. Moral hazard, zombie lending, and asset price distortion are real risks. The lesson of the financial accelerator is not that central banks should always intervene or never intervene. It is that financial systems have powerful internal amplifiers, and those amplifiers must be understood, measured, and managed. The construction firm in Phoenix did not stop building houses because the houses would have been bad. It stopped building because the financial system that should have funded the building stopped functioning. Understanding the financial accelerator helps us see that distinction clearly, and that clarity is the first step toward building a more stable financial system for households, workers, and firms alike.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.