Tutorial Categories

Last Updated: June 2, 2026 at 10:30

Minsky's Financial Instability Hypothesis Explained: Why Stability Creates Financial Crises

How long periods of calm can quietly build the conditions for economic collapse

Hyman Minsky argued that financial crises are not rare accidents but the natural outcome of how modern capitalist economies evolve over time. This tutorial explains his Financial Instability Hypothesis in clear, accessible language, using the 2006 housing market as a running example. You will learn how borrowers gradually move from safe to fragile financial positions, how banks actively lower their lending standards during booms, and how this shift builds systemic risk. The tutorial walks through the full boom-to-crisis cycle and examines real-world episodes from the 1997 Asian crisis to the 2008 financial crisis and the COVID-19 pandemic. By the end, readers will understand why periods of apparent safety can be the most dangerous of all, and how the shadow banking system and debt deflation dynamics amplify these cycles.

The Paradox of Tranquility

For most of his career, Hyman Minsky worked outside the mainstream of economics, developing ideas that many of his contemporaries viewed as too unconventional or insufficiently formal. His work did not fit easily into the dominant mathematical frameworks that shaped macroeconomic thinking in the late twentieth century, and as a result, his warnings about financial fragility received little attention. Yet when the 2008 financial crisis unfolded, his name suddenly appeared everywhere, from central bank speeches to major financial newspapers. The phrase "Minsky moment" became shorthand for the sudden collapse of asset prices after a long period of excessive borrowing and optimism.

There is a deep irony here that Minsky himself would have appreciated. The very stability that led policymakers and financiers to dismiss his warnings turned out to be the engine that produced the crisis. This irony has a name among those who study financial instability: the paradox of tranquility. The safer the system appears, the more risk-taking it encourages, and the less safe it actually becomes.

This paradox raises a fundamental question that will guide this tutorial. Was Minsky describing an unusual breakdown, or was he identifying something essential about how capitalist economies function? If financial instability is built into the system rather than imposed from outside, then crises are not anomalies to be eliminated but recurring outcomes that must be understood and managed. The evidence suggests that Minsky was right about the pattern, even if the timing of any particular crisis remains impossible to predict.

Section 1: The Basic Insight — Why Stability Destroys Stability

Minsky's central idea is deceptively simple, but its implications reach deep into how we think about markets, risk, and regulation. He argued that periods of economic stability do not make the financial system safer over time. Instead, they gradually make it more fragile. This is the opposite of what many people assume. The natural intuition is that if nothing has gone wrong for a long time, the system must be robust. Minsky argued that the opposite is true: if nothing has gone wrong for a long time, the system has likely accumulated hidden vulnerabilities.

Why does this happen? When households, firms, and financial institutions experience years of steady growth, low default rates, and rising asset prices, they begin to revise their expectations about risk. What once seemed cautious starts to feel unnecessarily restrictive. A family that saved for a 20 percent down payment in the 1990s might, by the mid-2000s, see a 10 percent down payment as perfectly reasonable because housing prices have only ever gone up. A bank that required full documentation of income in the 1990s might, by the mid-2000s, accept stated income loans because competition from other banks forces it to relax its standards.

Each individual decision appears reasonable when viewed in isolation. A bank that slightly lowers its lending standards is responding to competitive pressure and to recent data showing that defaults are rare. A household that takes on a larger mortgage is responding to low interest rates and a decade of rising property values. No single actor intends to make the system more fragile. Yet collectively, these decisions transform the structure of the financial system.

Over time, the system shifts from a position where most borrowers can comfortably meet their obligations even under mild stress to one where many borrowers depend on continued favourable conditions. This gradual shift is not driven by irrational exuberance in the sense of simple optimism. It is driven by adaptive behavior. Stability teaches borrowers and lenders that risk is low, and they act on that lesson. In doing so, they borrow and lend more aggressively, which actually increases risk. Stability destroys stability.

This view stands in direct contrast to the Efficient Market Hypothesis, which suggests that financial markets process information effectively and tend toward equilibrium. In that framework, instability is usually attributed to external shocks — an oil price spike, a sudden policy change, a war. In Minsky's framework, instability emerges from within the system. The seeds of the next crisis are planted during the long boom that precedes it.

Section 2: The Three Stages of Borrower Fragility

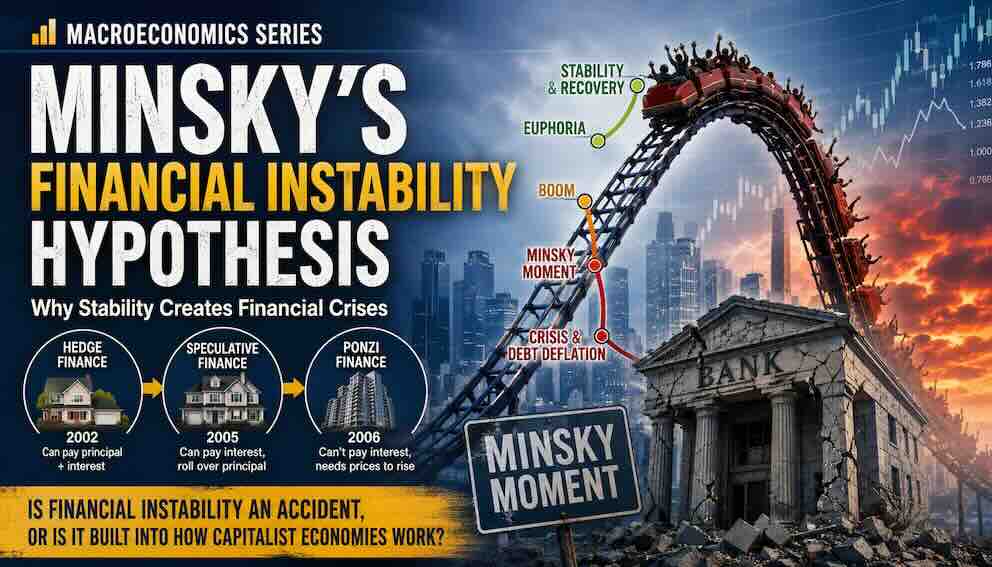

At the heart of Minsky's theory is a classification of how borrowers finance their activities. These categories describe not the intentions of borrowers but the structural position of their balance sheets. To make this concrete, it is useful to follow a single household through the United States housing market in the years leading up to 2006.

Hedge Finance — The Stable Beginning

Imagine a household in 2002 purchasing a home with a traditional 30-year fixed-rate mortgage. Their income is steady, and they put 20 percent down. The mortgage is structured so that monthly payments cover both interest and principal. This means that over time, the debt is gradually paid down, and the borrower does not depend on refinancing or on rising asset prices to remain solvent. Even if housing prices stagnate or fall moderately, the household continues to pay down the loan.

This is what Minsky called hedge finance. The borrower's expected cash flows from income are sufficient to meet all contractual obligations. The loan has a comfortable margin of safety — the cushion between what the borrower must pay and what the borrower is expected to earn. Hedge finance represents the stable baseline of the system. When most borrowing in an economy is hedge finance, the financial system is robust. It can absorb moderate shocks because borrowers have room to adjust.

Speculative Finance — Growing Dependence on Credit

Now consider the same household in 2005. Housing prices have been rising steadily for several years. The household has accumulated equity in its home and receives mailers from banks offering attractive refinancing options. Interest rates remain relatively low, but the household wants to reduce its monthly payments to free up cash for other spending.

The household refinances into an interest-only mortgage. Monthly payments now cover only the interest, not the principal. The principal will have to be repaid later when the loan matures, or it will have to be rolled over into a new loan. At this stage, the borrower can still meet interest payments from income, but the principal is no longer being reduced. The borrower depends on the ability to refinance when the loan matures.

This is speculative finance. The margin of safety has shrunk. The borrower is not insolvent — income still covers interest — but the borrower has lost the ability to reduce debt over time. As long as credit remains available and interest rates do not rise sharply, speculative finance is manageable. But it introduces a new vulnerability. If credit conditions tighten or if interest rates increase, refinancing may become difficult or expensive. A borrower who could afford interest payments at 6 percent might struggle at 8 percent.

Ponzi Finance — Reliance on Rising Prices

By 2006, the same household, encouraged by continued price increases and by stories of neighbors making large profits from real estate, decides to purchase a second property as an investment. This time, the mortgage is structured as a low-documentation loan with a very low introductory rate that will reset higher after two years. The household puts almost nothing down — perhaps 3 percent or even zero. The expectation is that the property's value will continue to rise, allowing the household to sell at a profit before the rate resets, or to refinance under similarly favorable terms.

In this situation, the household's income from wages is no longer sufficient to cover the mortgage payments once the introductory rate expires. The entire financial position depends on continued increases in property prices. This is Ponzi finance — a term Minsky used not to imply fraud, but to describe a structural position where cash flows from operations are insufficient to cover either interest or principal. The borrower needs asset appreciation not just to make a profit, but to remain solvent. The margin of safety has not just shrunk; it has disappeared.

The progression from hedge to speculative to Ponzi finance does not require any change in the borrower's character or intentions. It reflects a changing environment in which rising prices and easy credit make increasingly risky positions appear reasonable. When many borrowers move along this spectrum at the same time — encouraged by banks that are also competing for market share — the entire financial system shifts from robust to fragile.

The Boom–Fragility–Crisis Cycle

Minsky's framework becomes most powerful when these individual behaviors are placed within a broader cycle that describes how economies evolve over time. This cycle has five recognizable phases.

Phase 1: Stability and Recovery

After a financial crisis, the system resets. Borrowers who took excessive risks exit the market, either through default or through restructuring. Lenders tighten their standards sharply. Regulators, chastened by the recent disaster, impose stricter oversight. The surviving participants become deeply cautious. Loans are extended conservatively, with large down payments, full documentation, and comfortable debt-to-income ratios. Leverage is low.

During this phase, the economy begins to recover slowly, supported by more robust financial structures. Growth may be modest, but it is built on a solid foundation. The memory of the crisis is fresh, and no one wants to repeat it.

Phase 2: Euphoria

As the recovery continues and stability persists year after year, confidence grows. Borrowers observe that incomes are stable and asset prices are rising. Lenders observe that defaults remain very low. Over time, both groups begin to question whether the caution of the post-crisis period was excessive. Perhaps the regulations are too strict. Perhaps the old standards were unnecessarily conservative.

Financial innovation often accelerates during this phase. New mortgage products are developed. New ways to package and sell debt are created. These innovations are not necessarily harmful by themselves, but they often allow credit to flow to borrowers who would not have qualified under the stricter standards of the recovery period.

Phase 3: The Boom

In the boom phase, rising asset prices validate the decisions made during the euphoric period. Borrowers who took on more risk appear to have been rewarded, which encourages others to follow. The household that bought a second property with no money down sees its value increase by 15 percent in a single year. Stories of such gains spread.

Here a critical element of Minsky's theory must be emphasized. Banks are not passive participants in this process. They actively lower their own lending standards over the course of the boom, competing for market share and responding to their own recent experience of low defaults. A bank that has not suffered a default in five years begins to accept smaller down payments. It begins to accept stated income rather than verified income. It begins to lend to borrowers with lower credit scores. This is not a mistake or a failure of judgment from the perspective of the individual bank. Given the information available and the competitive pressure from other banks, each bank's decision to relax standards is entirely rational. But collectively, these decisions transform the system. The boom is driven as much by lenders reaching for yield as by borrowers reaching for homes.

Ponzi finance becomes more widespread during the boom, although it is not always recognized as such because rising prices mask underlying vulnerabilities. A borrower who depends on continued appreciation to remain solvent does not appear troubled as long as appreciation continues. Financial instruments become more complex, and risk is often obscured rather than eliminated. Regulators may struggle to keep pace with these developments, or they may share the general optimism of the period.

Phase 4: The Minsky Moment

The turning point — the Minsky moment — occurs when some event causes lenders and investors to suddenly reassess risk. This trigger does not need to be large. It could be a modest increase in interest rates by the central bank. It could be a small rise in default rates in a particular sector, such as subprime mortgages. It could be a sudden change in market sentiment triggered by the failure of a single financial institution.

What matters is not the size of the trigger but the fragility of the system that receives it. In a robust system dominated by hedge finance, a small trigger produces a small response. In a fragile system dominated by speculative and Ponzi finance, a small trigger produces a large response. The Minsky moment is the moment when the system shifts from complacency to panic.

Once the shift begins, credit tightens rapidly. Borrowers who depend on refinancing — the speculative borrowers — find it difficult or impossible to roll over their debt. Borrowers who depend on rising prices — the Ponzi borrowers — become insolvent almost immediately. Asset prices begin to fall as distressed selling increases.

Phase 5: Crisis and Debt Deflation

As prices decline, the value of collateral falls, which further restricts access to credit. This creates a feedback loop. Falling prices lead to forced sales, which push prices down further. Banks that held collateral now find that collateral insufficient, so they call in loans or refuse to extend new credit. Credit markets may freeze entirely as lenders become uncertain about which counterparties are solvent.

The result is a broad economic contraction. This is not just a recession caused by a reduction in spending. It is a debt deflation — a process in which falling prices increase the real burden of debt, which forces more selling, which pushes prices down further. This process, which the economist Irving Fisher described in the 1930s, is examined in detail in the following tutorial of this series. For now, it is enough to note that the 2008 financial crisis followed this pattern closely, as did the Great Depression.

Section 4: Why Minsky Was Ignored — And Why That Matters

The cycle just described — stability, euphoria, boom, Minsky moment, debt deflation — was playing out in slow motion throughout the 1990s and 2000s, yet most mainstream economists did not see it coming. Understanding why Minsky's ideas were overlooked for so long requires looking at the intellectual environment of economics during his career.

Much of mainstream macroeconomics focused on models that emphasized equilibrium, rational expectations, and mathematical tractability. These models were well suited for analyzing certain types of policy questions, but they did not easily accommodate the kind of endogenous instability that Minsky described. Minsky's approach was more qualitative and institutional. He focused on how financial practices evolve over time and how these changes affect the stability of the system. This made his work harder to formalize within the dominant frameworks. As a result, his ideas were often seen as interesting but not central to the discipline. Economists might read a Minsky paper as an interesting case study, but they would not build their research agendas around his framework.

There is a broader lesson here about the relationship between theory and policy. Economic models shape what policymakers look for and what they consider possible. If the prevailing models assume that markets are generally self-correcting and that financial crises are rare events caused by external shocks, then there is little incentive to search for signs of systemic fragility that have built up during a long boom. In this sense, the absence of a widely accepted framework for understanding endogenous financial instability contributed to the lack of early warning before the 2008 crisis.

The Minsky Moment in Historical Perspective

Minsky's framework can be applied to several major financial episodes in recent history. Each episode follows the same arc: a long period of stability and rising asset prices, a gradual shift toward fragile financing structures, a small trigger, and a sudden collapse.

The Asian Financial Crisis (1997)

During the 1990s, several East Asian economies experienced rapid growth and large inflows of foreign capital. Borrowers in Thailand, South Korea, Indonesia, and Malaysia accumulated significant foreign-denominated debt, often under the assumption that exchange rates would remain stable and that growth would continue indefinitely. This was a classic boom phase with increasing speculative finance.

When investor sentiment shifted in 1997 — triggered in part by the devaluation of the Thai baht — capital flows reversed sharply. Currencies depreciated dramatically. Borrowers who had taken out loans in US dollars found that their local currency incomes could no longer service those debts. The Minsky moment arrived, and the crisis spread across the region.

The Dot-Com Bubble (2000)

The late 1990s saw enormous optimism about internet-based companies. Stock prices rose to levels that were not supported by underlying earnings, but the rising prices themselves attracted more investment. In the early years of the boom, some technology companies had genuine revenues and plausible business models. These were the hedge finance positions — modestly leveraged, with some margin of safety. As the boom continued, a second wave of companies entered public markets with no earnings and only the hope of future revenues. These were speculative finance positions, dependent on continued access to capital markets to survive. By the peak of the bubble in 1999 and early 2000, a third wave emerged: companies with no revenues at all, no clear path to profitability, and valuations based entirely on the expectation that someone else would pay more later. This was pure Ponzi finance, where the entire position depended on continued price appreciation.

When expectations changed in 2000, the trigger was modest — a slowing of earnings growth for some leading technology companies — but the fragility of the system was extreme. Companies in the Ponzi category collapsed immediately. Those in the speculative category could not roll over their debt. Even some hedge finance companies were pulled down by the broader panic. The NASDAQ index fell nearly 80 percent from its peak.

The 2008 Financial Crisis

The 2008 crisis provides the most comprehensive illustration of Minsky's hypothesis. The United States experienced a long housing boom following the recession of 2001. Low interest rates, relaxed lending standards, and rising prices encouraged a massive shift from hedge to speculative to Ponzi finance in the housing market. By 2006, millions of households had mortgages that they could not sustain without continued price appreciation or refinancing.

But the fragility was not confined to traditional banks and their borrowers. By the mid-2000s, much of the most dangerous lending had migrated into the shadow banking system — a collection of financial institutions that performed bank-like functions but operated outside the regulatory framework designed for commercial banks. Money market funds, investment banks, structured investment vehicles, and the repo market all played roles that resembled traditional banking: they took short-term deposits (broadly defined) and made longer-term loans. But they did not have access to deposit insurance or to central bank emergency lending. This made them acutely vulnerable to runs. When confidence evaporated in 2007 and 2008, the shadow banking system experienced a run that was as sudden and as devastating as the bank runs of the 1930s, but it happened in wholesale funding markets rather than on retail deposit lines.

The trigger was modest: a small increase in interest rates and a small rise in defaults among subprime borrowers. But the system was so fragile that this modest trigger produced a global financial meltdown. The Minsky moment arrived in August 2007 with the freeze in the commercial paper market — a key part of the shadow banking system — and it culminated in September 2008 with the collapse of Lehman Brothers. The debt deflation that followed saw housing prices fall by more than 30 percent nationally, and by much more in the hardest-hit regions.

The Counterexample — COVID-19 (2020)

The economic shock associated with the COVID-19 pandemic might have been expected to trigger a similar dynamic. Economic activity contracted sharply and suddenly. Financial markets experienced their fastest decline in history. Millions of workers lost their jobs within weeks.

Yet a full Minsky-style crisis did not materialize. Why? The answer lies in the speed and scale of policy intervention. Central banks cut interest rates to near zero within days. Governments provided direct payments to households, expanded unemployment benefits, and offered loans and grants to businesses. These measures interrupted the feedback loop that typically drives a Minsky cycle. Borrowers who might have become distressed were supported. Asset prices were stabilized before widespread forced selling could begin.

The COVID-19 episode does not disprove Minsky's theory. Instead, it demonstrates that policy can influence how the cycle unfolds. The underlying tendencies toward fragility remain, but their consequences can be mitigated or delayed by aggressive intervention. What the episode does not tell us is whether such interventions will always be possible or politically feasible in the future.

Conclusion

Minsky's Financial Instability Hypothesis offers a way of understanding financial crises that shifts the focus from external shocks to internal dynamics. It suggests that the very processes that generate stability and growth can, over time, create the conditions for instability. This is the paradox of tranquility, and it is the central insight that separates Minsky from economists who view crises as rare accidents.

The progression from hedge to speculative to Ponzi finance is not a theory of irrational behavior. It is a theory of how rational behavior, repeated over time and shaped by experience, gradually transforms the structure of the financial system. Borrowers and lenders do not need to be greedy or foolish to produce a crisis. They only need to learn from the recent past. And when the recent past has been benign, what they learn is that risk is low. Acting on that belief, they take on more risk, and the system becomes less stable. Banks actively participate in this process, lowering their own standards in response to competition and experience, accelerating the shift toward fragility. And as the shadow banking system grows, the fragility can migrate to parts of the financial system that are less visible and less regulated.

This perspective does not imply that crises are inevitable in a deterministic sense. Policy matters. Regulation matters. The lender of last resort matters. The COVID-19 response showed that aggressive intervention can prevent a Minsky moment from unfolding into a full depression. But the COVID-19 response also showed something else: the underlying fragilities did not disappear. They were held in abeyance by extraordinary policy measures that cannot be sustained forever. The debt deflation dynamics that Fisher described remain a threat whenever leverage is high and asset prices begin to fall.

The renewed interest in Minsky's ideas after 2008 reflects not just the relevance of his insights, but also the limitations of the models that once dominated economic thinking. As policymakers continue to grapple with financial stability, his emphasis on endogenous fragility — on the way stability breeds instability — remains an essential part of the conversation. The paradox of tranquility is not a curiosity. It is a warning. And it suggests that the most dangerous moment for a financial system may be the one when everyone believes it is finally safe.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.