Tutorial Categories

Last Updated: June 2, 2026 at 10:30

Debt Deflation Theory Explained: Irving Fisher, Japan's Lost Decades, and the 2008 Crisis

How excessive debt, falling prices, and balance sheet repair can trap entire economies in long downturns

This tutorial explains debt deflation theory through the life and work of Irving Fisher, one of the most influential economists of the early twentieth century, who lost his personal fortune in the 1929 crash and then devoted himself to understanding what had happened. It shows how excessive debt combined with falling prices can trigger a self-reinforcing spiral of asset sales, rising real debt burdens, and economic contraction. The discussion then moves to Japan's "lost decades," where Richard Koo's idea of a balance sheet recession illustrates the same mechanism unfolding slowly over time, and to the 2008 financial crisis, where policymakers applied lessons drawn from Fisher to prevent a deeper collapse. The tutorial also explains Fisher's own policy prescription of reflation, the role of the gold standard in worsening the Great Depression, the importance of household debt in slowing the post-2008 recovery, and whether debt deflation remains a risk given current global debt levels. By the end, readers will understand why Fisher's neglected diagnosis has become essential to modern macroeconomic policy.

Irving Fisher's Personal Story: The Beginning of the Theory

Irving Fisher's story is not just an introduction to debt deflation theory. It is the emotional and intellectual foundation of it. In 1929, Fisher was widely regarded as the most famous economist in the United States. He was not an outsider making speculative claims. He was deeply respected, academically accomplished, and influential in both public and policy circles. He had written extensively on money, prices, and capital, and his work on the quantity theory of money was standard reading for anyone studying economics.

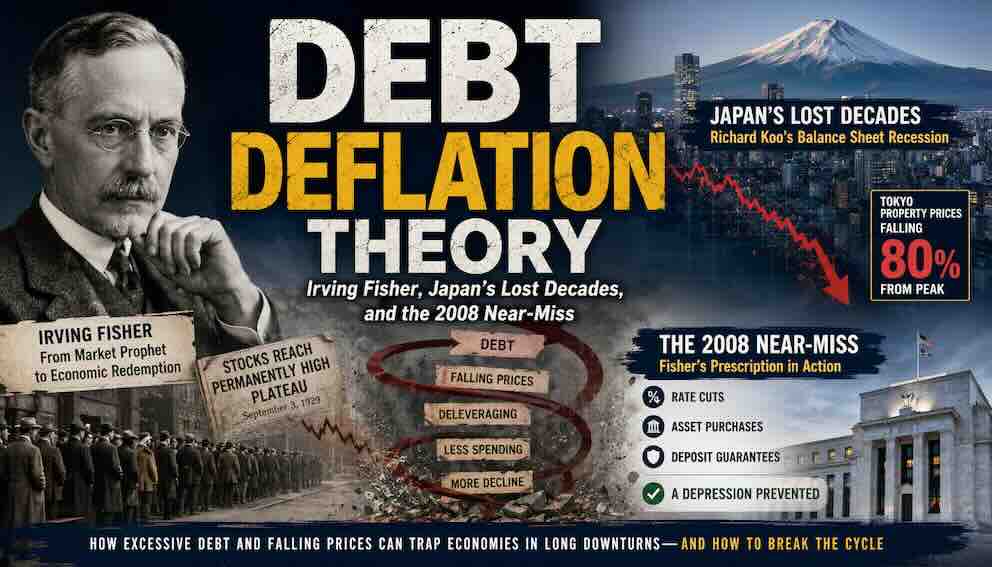

Just days before the stock market crash of October 1929, Fisher made a statement that would follow him for the rest of his life. He declared that stock prices had reached what he called a "permanently high plateau." The phrase was not offhand. He believed it. He had studied market fundamentals, looked at earnings, and concluded that the boom was justified.

When the market collapsed shortly after, the consequences for Fisher were devastating. He had invested heavily using borrowed money, which was a common practice during the speculative boom of the 1920s. As asset prices fell sharply, his wealth evaporated. Estimates suggest that he lost a personal fortune of more than 10 million dollars, which in today's terms would be the equivalent of well over 100 million dollars. His financial losses were accompanied by a collapse in his reputation. A man who had once been celebrated as a leading voice in economics became a symbol of misplaced optimism. For years, colleagues and critics alike would refer to his prediction as an embarrassment.

But Fisher did not simply withdraw from public life after this. He did not retreat into bitterness or silence. Instead, he turned his attention to understanding what had gone wrong. He wanted to explain not only his own losses but the broader economic collapse that had unfolded across the United States and the world. The result of this effort was his theory of debt deflation, which he published in the early 1930s in a paper titled "The Debt-Deflation Theory of Great Depressions."

What makes this story compelling is that the theory did not emerge from abstract reasoning alone. It was shaped by direct experience with the forces it describes. Fisher had lived through the boom fueled by debt, the sudden collapse in asset prices, and the painful process of trying to repay obligations when income and prices were falling. His theory is rooted in both observation and personal consequence. He was not an outsider looking in. He was a participant who had been caught in the very machinery he then set out to explain.

The Core Idea: How Debt and Falling Prices Interact

Debt deflation theory begins with a simple but powerful observation. When an economy accumulates too much debt, it becomes fragile. This fragility is not immediately visible during periods of growth. In fact, rising asset prices and expanding credit often create a sense of stability and prosperity. People feel wealthier. Businesses invest more. Borrowing seems manageable because incomes are rising and assets are appreciating.

The problem emerges when something causes asset prices to fall. This could be a stock market crash, a decline in real estate values, a wave of business failures, or a broader economic slowdown. When prices begin to drop, the real burden of debt increases. This happens because debts are typically fixed in nominal terms. The amount owed — measured in dollars or yen or pounds — does not change when prices fall.

To understand this, imagine a business that has borrowed one million dollars and expects to repay the loan using revenue generated from selling its products. The business plans to sell 100,000 units at 10 dollars each. If the price per unit falls to 8 dollars, the business now needs to sell 125,000 units to generate the same revenue. But selling more units may not be possible if demand has also fallen. The debt has not changed in dollar terms, but in real terms — measured against the business's diminished revenue — it has become much heavier.

This is the core mechanism of debt deflation. Falling prices redistribute wealth from debtors to creditors without any legislation or policy change. The debtor owes the same amount but earns less. The creditor is owed the same amount but can buy more goods with the repayment because prices have fallen.

The problem is that this redistribution does not leave the economy neutral. Debtors who suddenly find themselves unable to meet their obligations are forced to take action. They begin to sell assets to raise cash and reduce their debt. These asset sales push prices down further. As prices fall, more borrowers find themselves under pressure, leading to more selling. The process becomes self-reinforcing.

Fisher described this as a spiral with nine interacting factors. The most important of these — the ones that do the heavy lifting in his theory — are:

- Distress selling — Borrowers forced to sell assets quickly, often at whatever price they can get, to meet margin calls or debt payments

- Falling profits — As prices fall, business revenues decline, squeezing profit margins and making it harder to service debt

- Falling output — With profits falling and debt heavy, businesses cut production and lay off workers

- Falling confidence — As the spiral continues, lenders and borrowers become increasingly pessimistic, which slows spending further

These factors do not operate in sequence. They operate simultaneously, each amplifying the others. The economy becomes trapped in a cycle where attempts to reduce debt collectively make the situation worse.

Why the Spiral Becomes So Persistent

One of the most important aspects of debt deflation theory is that individual actions that seem rational can produce harmful outcomes at the collective level. Economists have a name for this kind of situation: the paradox of thrift. What is prudent for a single household or firm can be disastrous when everyone does it at the same time.

When a household or a firm tries to reduce its debt, it is acting prudently. Paying down liabilities improves financial stability and reduces the risk of default. No one would criticize a family for paying off its credit cards or a business for reducing its loan balance. From the perspective of the individual actor, deleveraging is responsible behavior.

However, when many households and firms attempt to do this at the same time, the effect on the economy is contractionary. Consider a situation where many businesses decide to cut spending in order to repay loans. They stop investing in new equipment. They delay hiring. They may even lay off workers. This reduces demand for goods and services across the economy. As demand falls, revenues decline for other businesses. Those other businesses now find it harder to service their own debts, so they cut spending as well.

At the same time, falling prices increase the real value of existing debts. This means that even as borrowers try to reduce their obligations, the burden does not decline as quickly as they expected. They sell assets, but the prices they receive are falling. They cut spending, but the revenue they need to repay debt is also falling. The effort to deleverage becomes more difficult, not less, the more people attempt it.

The persistence of this process is what makes debt deflation particularly damaging. It is not just a short-term adjustment. It can lead to prolonged periods of weak growth, high unemployment, and financial instability. The economy does not naturally bounce back from a debt deflation spiral because the forces that drive it are self-reinforcing. Falling prices lead to more distress selling, which leads to more falling prices. Lower spending leads to lower incomes, which leads to lower spending.

This is where Fisher's work connects to the previous tutorial in this series. While Hyman Minsky described how debt accumulates during good times — how stability breeds instability and how borrowers slide from hedge to speculative to Ponzi finance — Fisher described what happens when that accumulated debt begins to unwind. Minsky explained the boom. Fisher explained the bust. Together, they provide a nearly complete account of why financial systems go through cycles of expansion and collapse. And as we will see in the next tutorial on credit cycles, understanding how these cycles generate the debt accumulation that makes deflation possible completes the intellectual chain.

Fisher's Policy Prescription: Reflation and the Gold Standard

Fisher did not merely diagnose the problem of debt deflation. He prescribed a specific solution, and his prescription was controversial in its time precisely because it ran counter to the orthodox thinking of the early 1930s. That orthodoxy held that governments should balance their budgets, central banks should not expand the money supply excessively, and the gold standard should be maintained at all costs. Fisher argued that all of these orthodoxies were wrong.

Fisher's solution was called reflation. He meant this term quite literally. Deflation was falling prices. Reflation was the deliberate reversal of that process — raising the price level back to where it had been before the deflation began. Fisher argued that if the government could increase the general price level to its pre-deflation level, the real burden of debt would be restored to its original size. Borrowers would no longer be crushed by debts that had grown heavier through falling prices.

This was not an abstract theoretical proposal. Fisher meant it as a practical policy. He advocated for monetary expansion — for central banks to create more money and credit — until prices had risen back to their pre-crash levels. He understood that this would benefit debtors at the expense of creditors, but he argued that this was necessary to prevent the complete collapse of the economic system. A general default that wiped out the entire corporate and household sector would harm creditors far more than a modest redistribution through reflation.

The obstacle to Fisher's prescription in the early 1930s was the gold standard. Under the gold standard, each country's currency was convertible into a fixed quantity of gold. The money supply was constrained by the amount of gold held in central bank vaults. A country could not simply print money to reflate its economy because doing so would risk depleting its gold reserves as people converted the expanded currency into gold.

Fisher understood that the gold standard made debt deflation worse by preventing the monetary expansion needed to stop the spiral. Countries that remained on the gold standard were forced into deflationary policies — cutting spending, raising interest rates, and allowing unemployment to rise — to protect their gold reserves. Countries that left the gold standard, by contrast, could expand their money supplies and begin the process of reflation.

The empirical evidence confirms Fisher's insight. The economist Barry Eichengreen documented that countries which left the gold standard earlier — such as Britain, which left in 1931, and the Scandinavian countries, which left around the same time — recovered from the Great Depression much faster than countries that stayed on gold longer, such as France and the United States (which finally left in 1933 after Roosevelt's election). The United States under President Franklin Roosevelt abandoned the gold standard in 1933, devalued the dollar against gold, and began a program of monetary expansion. The economy began to recover shortly thereafter. While many factors contributed to the recovery, Fisher's reflation prescription was a central part of the policy shift.

This historical episode matters for understanding the 2008 crisis because the policy response in 2008 was, in many ways, a modern reflation. Central banks expanded their balance sheets dramatically through quantitative easing. They signaled that they would tolerate higher inflation if necessary. They explicitly aimed to stabilize asset prices and prevent deflation from taking hold. The language was different — no one spoke of "reflation" in 2008 — but the logic was Fisher's.

Why We Must Distinguish Deflation from Disinflation

Before moving to historical examples, a brief clarification is necessary. When economists talk about debt deflation, we often mean a sustained fall in the general price level — outright deflation. This is what happened in the United States during the Great Depression, with prices falling by roughly 25 percent between 1929 and 1933. It is also what happened in Japan during the 1990s and 2000s, with consumer prices occasionally falling on a year-over-year basis.

However, a prolonged period of very low inflation — sometimes called disinflation — can create similar pressures, albeit less severe. If a household or business borrowed money expecting 2 percent annual inflation, and inflation instead runs at 0 percent for a decade, the real burden of that debt is higher than planned. The debtor must devote a larger share of real income to debt service. This is not as extreme as outright deflation, but it is a milder version of the same mechanism.

This distinction matters for policy. During the 2008 crisis and its aftermath, many advanced economies experienced very low inflation but not outright deflation. The United States, the United Kingdom, and the euro area all saw inflation fall below target for years. The fear among central bankers was not just that prices would fall, but that they would stay too low for too long, gradually increasing real debt burdens and slowing the recovery. Understanding this distinction helps us see that debt deflation is not an on-off switch. It is a spectrum.

Japan's Experience: A Slow-Motion Debt Deflation

Japan provides one of the clearest real-world examples of debt deflation dynamics, particularly when viewed through the framework developed by economist Richard Koo. Unlike the United States in the 1930s, where the process was sharp and dramatic, Japan's experience was gradual and persistent. But the underlying mechanism was similar.

During the late 1980s, Japan experienced a massive asset price bubble. Real estate and stock prices rose to extremely high levels, driven by easy credit, speculation, and a belief that the boom would continue indefinitely. In Tokyo, property values became so elevated that, as a famous anecdote has it, the land under the Imperial Palace was said to be worth more than all the real estate in the state of California. The comparison is partly rhetorical, but it gives a sense of the scale. This was not a modest bubble. It was one of the largest asset price run-ups in modern economic history.

When the bubble burst in the early 1990s, asset prices fell dramatically. Tokyo property prices eventually declined by roughly 80 percent from their peak. This was not a temporary correction. It was a prolonged and deep decline that lasted more than a decade. Stock prices fell by similar magnitudes. Companies that had borrowed against their real estate holdings suddenly found that their collateral had evaporated.

Consider a concrete example. A Japanese real estate company that had borrowed heavily in the 1980s to buy land in Tokyo might have seen the value of that land fall from 10 billion yen to 2 billion yen. Meanwhile, the debt remained at 8 billion yen. The company was now technically insolvent — its liabilities exceeded its assets — even though it was still operating and generating some revenue. Its priority was no longer expansion or profit maximization. Its priority was survival. Every yen of cash flow went toward debt repayment rather than new investment.

Richard Koo's key insight was that Japanese firms entered what he called a balance sheet recession. Even though interest rates were reduced to very low levels — in some cases close to zero — businesses were not willing to borrow and invest. They were not maximizing profits in the usual sense. They were minimizing debt. The standard logic of monetary policy — that lower interest rates stimulate borrowing and spending — broke down because firms were not interested in borrowing at any interest rate. Their goal was to repair their balance sheets, not to expand.

This created a situation where monetary policy became unusually ineffective. The Bank of Japan could lower interest rates to zero, but it could not force firms to borrow. As economists sometimes put it, the central bank was pushing on a string — it could pull back (tighten policy) but could not effectively push (loosen policy) when the private sector was determined to deleverage.

The result was a prolonged period of economic stagnation, often referred to as Japan's "lost decades." Growth remained slow for years. Inflation was low or negative. The economy struggled to regain momentum. Fiscal policy — government spending — became the primary tool for supporting demand, because monetary policy had lost much of its traction.

Japan's experience is important because it shows that debt deflation does not always unfold rapidly. In the United States during the Great Depression, the process was sharp and dramatic. In Japan, it was gradual and persistent. The underlying mechanism — excessive debt, falling asset prices, rising real debt burdens, and balance sheet repair — was similar in both cases. Only the speed differed.

The 2008 Financial Crisis: A Near-Miss

The global financial crisis of 2008 provides a powerful example of how the lessons of debt deflation theory can be applied in practice. It also shows what happens when policymakers have learned from history. However, to understand the full picture, we must look at both the financial sector and the household sector.

In the years leading up to the crisis, there was a significant buildup of debt, particularly in the United States housing sector. Rising home prices encouraged borrowing. Households took out larger mortgages. Financial institutions created increasingly complex securities backed by those mortgages. Leverage accumulated throughout the system, much as it had during the 1920s and during Japan's bubble.

When housing prices began to fall in 2006 and 2007, the dynamics described by Fisher started to emerge. Households found themselves with mortgages that exceeded the value of their homes — a situation known as negative equity. As of early 2009, more than 10 million American households, or roughly 20 percent of all homeowners with mortgages, were in negative equity. These households could not refinance their mortgages because they owed more than their homes were worth. They could not sell their homes without bringing cash to the closing table. Many simply stopped making payments and entered foreclosure.

The household debt channel was central to the depth of the recession. The economists Atif Mian and Amir Sufi documented this relationship in careful empirical work. They showed that counties with higher household debt before the crisis experienced sharper declines in employment and consumption after the crisis. Households with high debt burdens cut spending dramatically as they tried to repair their balance sheets. This reduction in consumption — not just the banking crisis — drove the depth of the recession.

At the same time, financial institutions faced losses on assets that had previously been considered safe. The banking system came under severe stress. The risk of a full debt deflation spiral — falling prices, rising real debt burdens, more defaults, further price declines — became very real.

What distinguishes 2008 from the Great Depression is the response of policymakers. By this time, Fisher's work was well understood. Economists and central bankers had studied the Great Depression and had absorbed its lessons. They were aware of the dangers posed by falling prices and rising real debt burdens. They knew that doing nothing — or doing too little — could allow the debt deflation spiral to take hold.

The response was aggressive and multifaceted. Central banks, led by the Federal Reserve under Ben Bernanke (who had studied the Great Depression extensively), reduced interest rates rapidly, cutting them to near zero. They also implemented unconventional policies such as large-scale asset purchases, often referred to as quantitative easing, which were designed to push down long-term interest rates and support asset prices. Governments provided guarantees to the banking system and, in some cases, injected capital directly into financial institutions. The goal was to prevent a wave of bank failures like the one that had turned the 1929 crash into the Great Depression.

These actions were aimed at preventing the collapse of the financial system and stabilizing prices. The goal was to stop the debt deflation spiral before it could fully take hold. Policymakers understood that if they could prevent a sustained fall in the general price level, they could prevent the most damaging aspect of debt deflation — the increase in real debt burdens that comes from falling prices.

It is important to understand that these policies were not arbitrary. They were informed by decades of research and experience, including the insights developed by Fisher and later extended by economists like Hyman Minsky and Ben Bernanke himself. The idea that reflation — raising the general price level — could reduce the real burden of debt was central to the response. The Federal Reserve's asset purchases were explicitly designed to support asset prices and prevent deflation from taking hold.

While the crisis was severe and led to a deep recession, the outcome was very different from the 1930s. The global economy did not experience the same scale of collapse. Unemployment rose sharply but did not reach Great Depression levels. The banking system was stabilized rather than allowed to fail en masse. This does not mean that the response was perfect or without controversy, but it does suggest that the application of economic ideas can have significant real-world consequences.

Does Debt Deflation Remain a Risk Today?

The events of 2008 showed that debt deflation can be managed — even prevented — when policymakers understand the mechanism and act aggressively. But this raises a troubling question. If the only thing standing between a financial crisis and a full debt deflation spiral is aggressive policy intervention, what happens when that intervention is not available?

To answer this question, we need to look at the current debt landscape. Global private debt — the debt of households and non-financial corporations — has continued to rise since 2008. According to data from the Institute of International Finance, global debt reached a record high of more than 300 percent of global GDP by 2021. In advanced economies, private debt levels are now higher than they were before the 2008 crisis. In China, corporate debt has grown particularly rapidly, raising concerns about a potential debt deflation spiral in the world's second-largest economy. These high debt levels mean that the same vulnerabilities that Fisher identified are still present. They have not been eliminated. They have simply been managed.

The COVID-19 pandemic provided a partial test. As the economy shut down in early 2020, many households and businesses faced sudden income losses. Debt levels were high going into the crisis. The risk of a wave of defaults and falling prices was real. Once again, policymakers responded aggressively — with direct payments to households, expanded unemployment benefits, loans and grants to businesses, and continued central bank support. These measures prevented a debt deflation spiral, just as they had in 2008.

But this pattern suggests that modern economies have not eliminated the risk of debt deflation. They have learned to manage it through massive and rapid intervention. The underlying fragility — high levels of debt, the potential for falling prices, the self-reinforcing spiral — remains. If policymakers hesitate, or if political constraints prevent a sufficiently large response, the spiral could still take hold.

Conclusion

Debt deflation theory provides a way of understanding how financial systems can become unstable when debt levels are high and prices begin to fall. It shows that economic downturns are not always driven by a single external shock. Instead, they can emerge from the interaction of balance sheets, prices, and behavior over time. The spiral that Fisher described — distress selling, falling profits, falling output, falling confidence — is not a theoretical curiosity. It is a pattern that has appeared repeatedly in modern economic history.

The story of Irving Fisher gives the theory a human dimension. It reminds us that economic ideas are often shaped by lived experience and that even the most respected experts can be caught off guard by the systems they study. Fisher transformed personal loss into a framework that continues to influence economic thinking nearly a century later. He did not simply observe the Great Depression from a distance. He lived through it, lost his fortune in it, and then devoted himself to understanding it. His prescription of reflation — deliberately raising the price level to reduce real debt burdens — anticipated the policy responses of 2008 and 2020.

Japan's long period of stagnation demonstrates how the same mechanism can operate in a slower, more persistent way, reshaping an economy over decades rather than years. It highlights the importance of balance sheets and the limits of traditional policy tools when the entire private sector is focused on debt repayment rather than investment. Richard Koo's concept of a balance sheet recession captures this dynamic perfectly: a recession caused not by a lack of credit, but by a lack of borrowers willing to take on new debt.

The events of 2008 show that these ideas are not confined to history. They remain relevant in modern financial systems, where debt continues to play a central role. The fact that policymakers were able to draw on Fisher's insights to mitigate the crisis illustrates the practical value of economic theory. The household debt channel, documented by Mian and Sufi, reminds us that the path from debt to deflation runs through ordinary families, not just financial institutions.

Yet the COVID-19 pandemic and its aftermath remind us that the risk has not disappeared. Every economic expansion contains the seeds of the next debt deflation scare, because every expansion involves the buildup of new debt. Global debt levels are higher than ever. The question is not whether debt will accumulate, but whether policymakers will recognize the spiral when it begins and act decisively to stop it.

Fisher's theory does not offer easy answers, but it offers something almost as valuable: a clear description of the mechanism, a vocabulary for discussing it, and a warning about what happens when it is ignored. It is not a historical curiosity. It is a permanent feature of economies that rely on private credit.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.