Tutorial Categories

Last Updated: June 7, 2026 at 11:30

Credit Cycles and Debt Dynamics: Why Financial Booms Turn Into Crises (and When They Don't)

How rising credit and asset prices reinforce each other over time, creating fragile systems that can unravel suddenly

Credit cycles are longer, quieter, and often more dangerous than ordinary business cycles, yet they remain poorly understood outside specialist circles. This tutorial explains how rising credit and asset prices reinforce each other over time, creating fragile financial systems that can unravel suddenly. Drawing on historical research and real-world crises—from the early 1990s Nordic banking collapses to the 2008 global financial crisis—it shows why private debt, especially mortgage borrowing, plays a central role in financial instability. It also explores how policymakers now try to detect and manage these risks using tools like the credit-to-GDP gap and stress testing, while acknowledging the political economy challenges that make these tools difficult to use in practice. The goal is to understand not just why credit cycles happen, but why some become catastrophic while others remain manageable, and whether the world today is storing up problems for tomorrow.

A Family, A Bank, and A Rising Market

Let us begin with a single family in a single city, because large economic forces often become clearer when we watch them play out in a small, concrete setting.

In the spring of 2004, a family in Phoenix, Arizona decides to buy a home. They have stable jobs, a modest down payment, and a good credit score. The local housing market has been rising for several years, but nothing too dramatic. They find a house they like, apply for a mortgage, and are approved. The bank is happy to lend because housing prices have only gone up and because they can sell the mortgage to another financial institution, freeing up capital to make more loans.

This single transaction seems unremarkable. It is one of millions happening across the country. But it is also a small thread in a much larger fabric. The family's decision to borrow, the bank's decision to lend, and the rising price of the house all contribute to a pattern that economists call a credit cycle.

Now imagine that same family five years later, in 2009. The housing market has collapsed. Their home is worth less than they paid for it. They still have their jobs, but they have watched neighbors lose theirs. They are not defaulting, but they are not spending either. Every extra dollar goes toward paying down the mortgage. They are not alone. Millions of families are doing the same thing. And this collective prudence, as Fisher and Minsky taught us, is precisely what makes the downturn deeper.

The credit cycle is like a slow-building tide. The business cycle is the waves on the surface. This tutorial will examine why credit expands and contracts in such long cycles, why these cycles are so difficult to recognize in real time, and what determines whether a credit boom ends gently or collapses into crisis. We will connect this family's experience to the research that has shaped modern understanding of financial instability, and we will see why the distinction between private and sovereign debt matters more than most people realize.

What Is a Credit Cycle? And How Is It Different from the Business Cycle?

To understand credit cycles, it helps to separate them from the more familiar concept of the business cycle. The business cycle refers to fluctuations in economic activity — periods of expansion followed by recessions. These cycles typically last between five and eight years and are often driven by changes in demand, investment, or policy. They are relatively easy to observe. When unemployment rises and GDP falls, people notice.

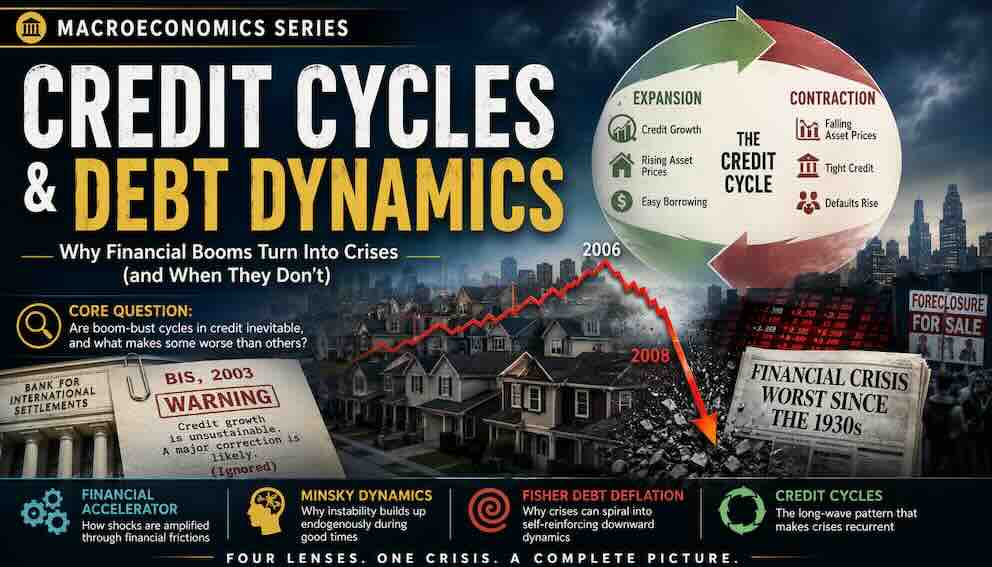

The credit cycle operates on a much longer horizon and moves more quietly. Research by Claudio Borio of the Bank for International Settlements shows that credit cycles often last 15 to 20 years. Because they unfold slowly, they are much harder to detect while they are happening. By the time the risks become obvious — when defaults rise and banks tighten lending — the system is often already fragile. The credit cycle is the tide. The business cycle is the waves.

At the heart of the credit cycle is a reinforcing mechanism that should be familiar from the previous tutorials in this series. During an expansion, banks are willing to lend, households and firms are willing to borrow, and asset prices — especially real estate — begin to rise. Rising asset prices increase the value of collateral. When a house is worth more, a bank is more comfortable lending against it. This additional lending pushes prices even higher.

This creates a feedback loop. Credit growth drives asset prices, and rising asset prices enable more credit. The system appears stable because defaults are low and balance sheets look strong. Everyone feels prosperous. However, this stability depends entirely on continued growth. The moment growth slows, the same feedback loop works in reverse.

The turning point does not require a dramatic shock. It can begin with something as simple as credit growth slowing down. When borrowing slows, asset prices stop rising. When prices stop rising, collateral values stabilize or fall. Banks become more cautious. Lending tightens. Prices begin to decline. This is the financial accelerator that Bernanke, Gertler, and Gilchrist described — and it is why credit cycles tend to be more extreme than ordinary economic fluctuations.

One of the most important mechanisms that makes credit busts so persistent is debt overhang. This term describes a situation where existing debt burdens are so large that they discourage new borrowing and investment even when interest rates are very low. A firm that is already highly leveraged will not take on new debt to expand, even if profitable opportunities exist, because it is focused on repairing its balance sheet. A household with a large mortgage will not take on new loans to buy a car or renovate a kitchen. Debt overhang is the mechanism that explains why recoveries from credit busts are often slow and weak. It is the reason that simply lowering interest rates is not enough to restart an economy that has been through a severe credit cycle. We will return to this concept later when examining the slow recoveries after 2008 and Japan's lost decades.

This tutorial builds directly on the three that came before it. Minsky explained how stability breeds instability and how borrowers slide from hedge to speculative to Ponzi finance. Fisher explained what happens when that debt begins to unwind — the spiral of falling prices and rising real debt burdens. The financial accelerator explained how small shocks are amplified through collateral and bank capital channels. This tutorial asks the preceding question: what generates the debt in the first place? How do credit cycles begin, why do they persist, and what determines whether they end in a gentle slowdown or a full-blown crisis?

Financial Liberalisation — The Recurring Trigger

If one looks across the history of credit booms, a clear pattern emerges. Major credit expansions are almost always preceded by financial liberalisation — the removal of credit controls, interest rate ceilings, lending restrictions, and other regulatory barriers that had previously constrained bank lending. This is one of the most consistent findings in the historical research of Carmen Reinhart and Kenneth Rogoff. Financial liberalisation does not guarantee a credit boom, but credit booms almost never happen without it.

The reason is straightforward. Before liberalisation, banks face binding constraints on how much they can lend and at what rates. They cannot compete aggressively for borrowers because regulations limit their ability to do so. When those constraints are removed, banks suddenly have both the ability and the incentive to expand lending. They compete for market share. They lower interest rates. They relax underwriting standards. The credit cycle begins.

This pattern can be seen across every major crisis examined in this tutorial. In the Nordic countries during the 1980s, financial deregulation allowed banks to lend freely for the first time in decades, fueling a rapid expansion in commercial real estate lending. In the United States, the savings and loan crisis of the late 1980s was preceded by deregulation that allowed these institutions to take on riskier assets. The 2000s housing boom was preceded by a long process of liberalisation that included the repeal of the Glass-Steagall Act's separation of commercial and investment banking, the preemption of state anti-predatory lending laws, and the growth of the shadow banking system outside traditional regulatory oversight.

The implication is important but often overlooked. Financial liberalisation creates benefits — more access to credit, lower borrowing costs, increased economic activity. But it also creates risks. Those risks do not appear immediately. They accumulate over years as the credit cycle unfolds. By the time they become visible, the system is already fragile. The challenge for policymakers is not to prevent liberalisation, which would be economically costly, but to manage the credit cycles that liberalisation makes possible.

Private Versus Sovereign Debt — Why the Distinction Matters

For much of the twentieth century, economists focused heavily on government debt. The concern was that excessive public borrowing would crowd out private investment or lead to inflation and default. While these risks are real, historical evidence shows that they are not the main drivers of financial crises.

Instead, the most dangerous debt build-ups have occurred in the private sector. And here the concept of debt overhang, introduced earlier, becomes particularly relevant. Private debt overhang directly reduces spending and investment. Households with too much debt cut consumption. Firms with too much debt postpone investment. Government debt overhang operates differently — it can be refinanced or inflated away, and it does not directly constrain spending in the same way.

A large body of research by Òscar Jordà, Moritz Schularick, and Alan Taylor examined data from 17 countries over more than 140 years. Their findings are striking. Financial crises are strongly associated with rapid increases in private credit — the debts of households and non-financial corporations. Mortgage lending is particularly dangerous. Government debt, by contrast, is a much weaker predictor of crises.

This pattern can be seen across major historical episodes. Before the crash of 1929, household and corporate borrowing had surged across the United States. In Japan during the 1980s, firms borrowed heavily against rising land prices. In the Nordic countries in the late 1980s, rapid deregulation led to a surge in private borrowing. In the United States before 2008, mortgage debt expanded rapidly as house prices climbed. In each case, the crisis that followed was preceded by a private credit boom, not a government borrowing spree.

The mechanism is straightforward. Private borrowers depend on income and asset values to service their debts. When asset prices fall or incomes decline, their balance sheets deteriorate quickly. Defaults increase. Banks suffer losses. The financial system comes under strain. Debt overhang then amplifies the downturn as households and firms shift from maximizing spending to minimizing debt.

Government debt operates differently. Governments have taxation power and, in many cases, control over their own currency. This gives them more flexibility to manage their obligations. They can refinance debt over long periods. They can inflate away some of its real value. They cannot be forced into the kind of immediate distress that a household faces when it cannot make its mortgage payment.

The implication is important. A narrow focus on public debt can miss the build-up of risks in private balance sheets. Many crises that appear to be about government finances actually begin in the private sector.

What Makes Debt Dangerous? Four Key Factors

Not all debt is equally risky. Some forms of borrowing support economic growth and remain manageable even when conditions change. Others create vulnerabilities that can destabilize the entire system. Four factors help determine the difference. Understanding them is essential for recognizing the difference between a healthy credit expansion and a dangerous bubble.

First, the purpose of borrowing matters enormously. When debt finances productive investment — building a factory, expanding a business, purchasing equipment that increases output — it generates income that can be used to repay the loan. This is often called "good debt." In contrast, borrowing to purchase existing assets, such as real estate or financial securities, does not create new income. It simply transfers ownership. It pushes prices higher without increasing the economy's productive capacity. This makes the debt harder to sustain if prices stop rising. Much of the borrowing in the 2000s housing boom was of this second type — households borrowing against rising home values to fund consumption, and investors borrowing to buy more properties.

Second, the currency of the debt is critical. Borrowing in a foreign currency exposes borrowers to exchange rate risk. If a country's currency depreciates, the real burden of foreign-denominated debt increases. The debtor owes the same number of dollars or yen, but their local currency income buys fewer of those dollars or yen. This dynamic played a central role in the Asian financial crisis of 1997, when firms in countries like Thailand and Indonesia had borrowed heavily in US dollars. When their currencies fell dramatically, their debts became much more expensive in local terms, leading to widespread insolvency and a deep regional recession.

Third, the maturity structure influences stability. Short-term debt must be rolled over frequently — sometimes every few days or weeks. If lenders become unwilling to extend new credit, borrowers face immediate repayment pressures. This is what happened to Northern Rock in 2007. The bank had funded long-term mortgages with short-term wholesale borrowing. When the wholesale markets froze, Northern Rock could not roll over its debt and collapsed. Long-term debt, by contrast, provides more time to adjust to changing conditions. It is less vulnerable to sudden shifts in market sentiment.

Fourth, the concentration of debt matters. When borrowing is spread across many households and small businesses, losses are distributed and often manageable. When debt is concentrated in large, interconnected institutions, the failure of a few entities can trigger systemic consequences. This is particularly important in banking systems, where the failure of one large bank can freeze the entire interbank lending market, as happened after Lehman Brothers collapsed in 2008.

These four factors — purpose, currency, maturity, and concentration — help explain why some credit booms end in a gentle slowdown and others end in catastrophe. The 2008 crisis was severe because the debt was tied to existing assets (housing), concentrated in large institutions, and in some cases of short maturity.

The US Housing Boom and Bust — A Full Credit Cycle

The US housing market in the 2000s provides the most vivid modern example of a full credit cycle, from quiet expansion to euphoric boom to catastrophic bust.

The upswing began in the 1990s and accelerated sharply after the 2001 recession. Interest rates were low. Financial liberalisation had allowed banks to expand lending in new ways. As house prices rose, both lenders and borrowers became more confident. A family that bought a home in 2000 and saw its value rise by 50 percent by 2005 felt wealthy. That wealth effect encouraged more spending and more borrowing.

New financial instruments played a central role in extending the boom. Mortgage-backed securities allowed banks to package thousands of individual mortgages together and sell them to investors around the world. Collateralised debt obligations (CDOs) took this a step further, creating complex tranches with different risk profiles. In theory, these instruments made the system safer by spreading risk widely. In practice, they often obscured risk and weakened lending standards. Banks no longer needed to hold loans on their balance sheets, so they had less incentive to assess borrowers carefully. The link between the original borrower and the ultimate lender was broken.

However, there is another important dimension to this story that moves beyond domestic credit creation. In the years before 2008, the United States experienced large inflows of foreign capital, particularly from China and other emerging Asian economies with high savings rates. These countries had accumulated substantial foreign exchange reserves and were looking for safe assets to invest in. US mortgage-backed securities, despite their hidden risks, were perceived as safe because they carried high credit ratings and because the US housing market had never experienced a national decline. This phenomenon, which Ben Bernanke called the global savings glut, meant that demand for mortgage-backed securities came not only from domestic investors but from around the world. This additional demand pushed down interest rates on mortgages and made credit even more abundant.

The global savings glut hypothesis is not universally accepted. Some economists argue that it overstates the role of foreign capital and understates the role of domestic financial deregulation. But it represents an important strand of thinking about what drives credit cycles from the supply side. It suggests that credit booms can be fueled not only by domestic bank lending but also by cross-border capital flows that respond to global rather than local conditions.

By the mid-2000s, the system appeared remarkably stable. House prices had risen for years without a national decline. Defaults were low. Financial innovation was celebrated. But the system was built on fragile foundations. Much of the borrowing was speculative, and some was Ponzi finance in Minsky's sense — borrowers who could only repay if prices continued to rise.

House prices peaked in 2006. The initial decline seemed manageable — just a few percentage points. But the interconnected nature of global finance meant that losses spread quickly. Financial institutions around the world held assets linked to US mortgages. When those assets lost value, banks suffered losses. When banks suffered losses, they reduced lending. When lending declined, housing demand fell further. The feedback loop reversed.

The result was the most severe global recession since the 1930s. Millions of households lost their homes. Unemployment doubled and tripled in many countries. The credit cycle had turned, and the turning was brutal.

The "This Time Is Different" Fallacy

The US housing boom and bust illustrates one of the most persistent patterns in the history of credit cycles: the belief that the current boom is different — that new financial instruments, better regulation, or structural changes have permanently reduced risk. This belief is so common that the economists Carmen Reinhart and Kenneth Rogoff gave it a name: the "this time is different" syndrome.

In the 1920s, many believed that the Federal Reserve, then only a decade old, had mastered the business cycle and that severe downturns were a thing of the past. In Japan in the 1980s, the belief was that the new financial system and the strength of the Japanese economy made a crash impossible. In the United States in the 2000s, the belief was that mortgage-backed securities and credit default swaps had distributed risk so widely that no single failure could threaten the system.

Each time, the belief proved wrong. The reason is not that policymakers or investors are foolish. It is that credit cycles are driven by forces that do not go away. Optimism, competition among lenders, and the reinforcing feedback between credit and asset prices are features of market economies, not bugs.

The warning that was ignored in 2003 came from the Bank for International Settlements. Its economists noted that credit was growing unusually fast in several advanced economies and that this pattern had historically ended badly. The report was not obscure. It was discussed in policy circles. But growth was strong, inflation was low, and financial innovation was widely seen as a stabilising force. The warning was set aside.

Five years later, the global financial system experienced its most severe crisis since the Great Depression. The "this time is different" syndrome had struck again.

The Nordic Crisis and Sweden's Response — A Model of Intervention

A similar pattern occurred in the Nordic countries — Finland, Sweden, and Norway — in the early 1990s. The details differ, but the underlying dynamics are remarkably similar to the 2008 crisis.

During the 1980s, these countries deregulated their financial systems. Banks were suddenly free to lend in ways that had previously been restricted. Credit grew rapidly. Asset prices, particularly commercial real estate, rose dramatically. Borrowers and lenders alike became increasingly optimistic. The feedback loop between credit and asset prices was fully engaged.

When the cycle turned, the results were severe. Banking systems came under extreme stress. Finland and Norway experienced deep recessions. Sweden, however, responded in a way that has become a model for crisis management.

The Swedish government intervened decisively. It guaranteed all bank deposits and creditors of the nation's 114 banks. It created a special agency to take over troubled institutions. It nationalized failing banks, cleaned up their balance sheets by separating bad loans from good assets, and later returned them to private ownership. The entire operation was conducted transparently, with clear communication to markets and the public.

The cost was substantial — roughly 4 percent of GDP — but far less than the cost of allowing the banking system to collapse. Sweden recovered relatively quickly. Its approach influenced policy debates during the 2008 crisis, although it was not applied uniformly. In the United States, for example, the government injected capital into banks but did not nationalize them, a decision that remains controversial.

The Nordic experience offers two lessons. First, credit cycles can be severe even in well-governed countries with strong institutions. Second, decisive intervention can limit the damage, but it requires political will and fiscal capacity.

The Eurozone Crisis — Private Debt Becomes Sovereign Debt

The eurozone crisis between 2010 and 2015 illustrates a crucial mechanism that is often misunderstood. Countries such as Greece, Ireland, Portugal, and Spain all faced severe sovereign debt pressures, but the underlying causes differed sharply. Understanding this difference is essential for seeing how private debt problems can become public debt problems.

Greece had persistent fiscal deficits and rising public debt for years before the crisis. Its problem was primarily a sovereign debt problem — the government had borrowed more than it could repay given the constraints of eurozone membership.

Ireland and Spain, however, entered the crisis with relatively sound public finances. Their governments were not spending excessively. Their debt-to-GDP ratios were low. The problem was in the private sector. Both countries had experienced massive credit booms in real estate, with banks lending heavily against rising property prices. When the property bubbles burst, these banks faced enormous losses.

Here is the mechanism that transformed private debt into sovereign debt. In September 2008, in the immediate aftermath of the Lehman Brothers collapse, the Irish government issued a blanket guarantee for all deposits and most debts of its six largest banks. The guarantee was intended to prevent a run on the Irish banking system. But it meant that when the banks later suffered massive losses on their real estate loans, the Irish government was legally obligated to cover those losses. Private debts became public debts. By 2010, Ireland's banking losses were so large — estimated at roughly 40 percent of GDP — that the government itself became insolvent and required a bailout from the European Union and the International Monetary Fund.

Spain followed a similar path, though with different timing. The Spanish government did not issue an explicit blanket guarantee, but the implicit guarantee that the state would not allow its largest banks to fail had the same effect. When the real estate bubble burst, the Spanish government was forced to recapitalize its banks, adding substantially to its public debt.

The distinction matters because it suggests different policy responses. A country with a sovereign debt problem caused by fiscal profligacy needs fiscal consolidation and structural reform. A country with a sovereign debt problem caused by private banking losses needs bank recapitalization and, potentially, debt restructuring. Applying the wrong prescription — austerity for a country whose only problem was a banking crisis — can deepen the downturn unnecessarily. Many economists argue that this is precisely what happened in Ireland and Spain, where austerity policies prolonged the recession.

Measuring and Monitoring Credit Cycles

Recognizing the importance of credit cycles, policymakers have developed tools to monitor and manage them. These tools are not perfect, but they represent a significant advance over the laissez-faire approach that prevailed before 2008.

One of the most widely used indicators is the credit-to-GDP gap. This measures how far the ratio of credit to economic output deviates from its long-term trend. Research by the Bank for International Settlements shows that large and sustained deviations — when credit grows much faster than GDP for several years — are strong predictors of financial crises. The gap was flashing red in the United States, Spain, Ireland, and several other countries in the mid-2000s. The warning was there, though it was not heeded.

Another key tool is the countercyclical capital buffer. Introduced under the Basel III international banking regulations, this requires banks to build up additional capital during periods of rapid credit growth. The idea is simple: build resilience during the boom so that losses can be absorbed during the downturn. When the cycle turns, banks can draw down these buffers, continuing to lend even as the economy contracts. This is the opposite of the procyclical behavior that amplified the 2008 crisis.

However, these tools face a fundamental limitation that is not technical but political. Regulators face enormous pressure not to tighten during booms precisely because everything appears fine. The financial industry lobbies against restrictions, arguing that the economy is strong and that additional capital requirements would slow growth. Politicians who benefit from a booming economy are reluctant to impose constraints that might cool it down. The credit-to-GDP gap may be flashing red, but the warning is often ignored. This is not a problem of measurement. It is a problem of institutional design and political will. It explains why the tools described here have been underused even where they exist. Even today, after the lessons of 2008, countercyclical buffers in most advanced economies are set at or near zero.

Stress testing is also widely used. Regulators require banks to demonstrate that they can withstand severe scenarios — a sharp decline in asset prices, a spike in unemployment, a sudden freeze in credit markets. These exercises are designed to identify vulnerabilities before they lead to systemic problems. The United States has conducted regular stress tests since 2009, and they have become a model for other countries.

The Global Debt Landscape Today — And Why It Matters

The credit cycle does not end with the 2008 crisis. It continues, and the world today is storing up problems for tomorrow.

According to data from the Institute of International Finance, global debt reached a record high of more than 300 percent of global GDP by 2021. In advanced economies, private debt levels are now higher than they were before the 2008 crisis. Household debt in countries like Canada, Australia, and South Korea has reached levels that would have seemed alarming a generation ago. The debt overhang that slowed the recovery after 2008 persists, and in some countries it has grown larger.

Most concerning, perhaps, is China. China's corporate debt-to-GDP ratio has risen from roughly 100 percent in 2008 to more than 160 percent today. However, a brief caveat is necessary here. Chinese debt statistics are subject to measurement uncertainty given the role of shadow banking — lending that occurs outside the traditional banking system — and local government financing vehicles, which are technically corporate entities but effectively act as extensions of government. These complexities mean that the true level of debt, and the true distribution of risk, is harder to assess in China than in most advanced economies. Nevertheless, even conservative estimates suggest that China's corporate debt is among the highest in the world.

Much of this debt was accumulated during a long credit boom driven by infrastructure investment and real estate development. The real estate sector, in particular, has seen rapid price increases and high levels of borrowing. Several large Chinese property developers have defaulted or come close to default in recent years, including Evergrande, which had liabilities exceeding 300 billion dollars. The risk is not just to China. A sharp slowdown in China's economy would affect commodity producers, trading partners, and global financial markets.

The question for policymakers today is whether the current debt levels constitute a dangerous credit cycle or a manageable expansion. The credit-to-GDP gap in most advanced economies is not flashing red as it did in 2006, but private debt remains near historical highs. The "this time is different" syndrome is always tempting. The challenge is to recognize the build-up of risks early and to act when the system still appears stable. And the political economy problem — the difficulty of tightening during booms — remains as acute as ever.

Conclusion

Credit cycles are not random events. They follow recognizable patterns driven by the interaction between borrowing, asset prices, and financial institutions. The reason they recur is not simply that policymakers fail to learn from history, although that is part of the story. It is also because the forces that drive credit expansion — optimism, innovation, competition among lenders, and the reinforcing feedback between credit and asset prices — are deeply embedded in market economies.

The pattern almost always begins with financial liberalisation, which removes the constraints that had previously limited credit growth. What follows is a slow-building tide. Credit expands. Asset prices rise. Collateral appreciates. More credit is extended. The system appears stable, even prosperous. Then the tide turns. A modest slowdown in credit growth, a small rise in defaults, a subtle shift in sentiment — any of these can trigger the financial accelerator. Asset prices fall. Collateral shrinks. Credit contracts. Debt overhang sets in, as households and firms shift from maximizing spending to minimizing debt. The recovery, when it comes, is slow.

What determines whether a credit boom ends gently or in crisis is not the existence of debt itself, but its structure, purpose, and distribution. When borrowing supports productive investment, is denominated in domestic currency, has a long maturity, and is spread broadly across the system, it can be managed. When borrowing is concentrated, tied to existing asset prices, short-term, and denominated in foreign currency, it becomes fragile. The worst crises combine multiple vulnerabilities.

The family in Phoenix in 2004 was not making a foolish decision. The bank that lent to them was not acting irrationally. The financial engineers who created mortgage-backed securities were responding to the incentive structures that financial liberalisation had created. Yet collectively, these individually reasonable decisions produced a system that collapsed. That is the paradox of credit cycles. What is rational for one actor can be destabilizing for all.

This tutorial has built on the three that came before it. Minsky explained how debt accumulates during good times. Fisher explained what happens when that debt unwinds. The financial accelerator explained how small shocks are amplified. This tutorial has asked the prior question: what generates the debt in the first place, and why do credit cycles last so long? The answer lies in the slow-building, self-reinforcing relationship between credit and asset prices — a relationship that is unlikely to disappear, but that can be understood, monitored, and sometimes restrained.

The challenge for policymakers is not to eliminate credit cycles, which is likely impossible, but to recognize their build-up early and limit their excesses. This requires not just technical tools like the credit-to-GDP gap and countercyclical capital buffers, but also the political will to use them when the economy appears strong. The warnings issued in 2003 show that the signals are often visible. The difficulty lies in acting on them when everyone believes that this time is different. Whether the world has learned this lesson remains an open question. The tide is always rising somewhere.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.